Health insurance in the USA is a complex and multifaceted topic, covering various aspects of medical care and financial protection for individuals and families. The system comprises both public and private insurance programs, each with its own set of benefits, limitations, and eligibility criteria. Understanding what health insurance covers is crucial for navigating the healthcare system effectively and ensuring access to necessary medical services. This paragraph will delve into the key components of health insurance coverage in the USA, including the types of plans available, the benefits they offer, and the factors that influence the cost and accessibility of health insurance for different populations.

Explore related products

What You'll Learn

- Types of Health Insurance Plans: Overview of HMO, PPO, EPO, and POS plans, their benefits and limitations

- Coverage for Pre-existing Conditions: Explanation of how pre-existing conditions are handled under different insurance plans

- Preventive Care Services: Details on coverage for routine check-ups, vaccinations, and other preventive health measures

- Prescription Drug Coverage: Information on how prescription medications are covered, including formularies and copay structures

- Mental Health and Substance Abuse Services: Coverage specifics for mental health treatments and substance abuse rehabilitation programs

![]()

Types of Health Insurance Plans: Overview of HMO, PPO, EPO, and POS plans, their benefits and limitations

Health insurance in the USA offers various plans, each with its own set of benefits and limitations. Understanding these plans is crucial for making informed decisions about your healthcare coverage. Here's an overview of four major types of health insurance plans: HMO, PPO, EPO, and POS.

Health Maintenance Organization (HMO) plans require you to choose a primary care physician (PCP) who will coordinate your care. HMOs typically cover preventive care and offer lower premiums and out-of-pocket costs. However, they may limit your choice of healthcare providers and require referrals to see specialists.

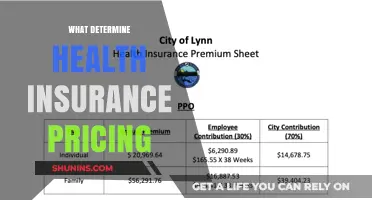

Preferred Provider Organization (PPO) plans offer more flexibility in choosing healthcare providers. They have a network of preferred providers, but you can also see out-of-network providers at a higher cost. PPOs often cover preventive care and provide a balance between lower premiums and the freedom to choose your doctors.

Exclusive Provider Organization (EPO) plans are similar to HMOs in that they require you to use a network of approved providers. However, they do not require referrals to see specialists. EPOs typically offer lower premiums and out-of-pocket costs but may have higher deductibles.

Point of Service (POS) plans combine features of HMOs and PPOs. They require you to choose a PCP and get referrals for specialists, but they also allow you to see out-of-network providers at a higher cost. POS plans often cover preventive care and offer a balance between lower premiums and flexibility in choosing providers.

When selecting a health insurance plan, consider your healthcare needs, budget, and preferences. Each plan type has its advantages and disadvantages, so it's essential to compare them carefully to find the best fit for you and your family.

When Can Employers Offer Medical Insurance to Employees?

You may want to see also

Explore related products

![]()

Coverage for Pre-existing Conditions: Explanation of how pre-existing conditions are handled under different insurance plans

Under the Affordable Care Act (ACA), also known as Obamacare, health insurance plans are required to cover pre-existing conditions without charging higher premiums. This means that individuals with chronic illnesses, such as diabetes or heart disease, cannot be denied coverage or charged more due to their condition. However, the specifics of how pre-existing conditions are handled can vary depending on the type of insurance plan.

For example, some plans may have a waiting period before covering pre-existing conditions, while others may require individuals to undergo a medical review before approving coverage. Additionally, some plans may have exclusions for certain pre-existing conditions, or may only cover them up to a certain limit. It's important for individuals to carefully review the details of their insurance plan to understand how pre-existing conditions are covered.

One unique aspect of coverage for pre-existing conditions is the concept of "grandfathered" plans. These are plans that were in existence before the ACA was passed and are exempt from some of the law's requirements, including the mandate to cover pre-existing conditions. However, these plans are becoming increasingly rare as more insurers opt to comply with the ACA's regulations.

Another important consideration is the impact of pre-existing conditions on insurance premiums. While the ACA prohibits insurers from charging higher premiums based on pre-existing conditions, individuals with chronic illnesses may still face higher out-of-pocket costs due to deductibles, copays, and coinsurance. Additionally, some plans may have higher premiums for individuals who use tobacco or have other lifestyle factors that are associated with higher health risks.

In conclusion, coverage for pre-existing conditions is a complex and important aspect of health insurance in the United States. While the ACA has made significant strides in ensuring that individuals with chronic illnesses have access to affordable coverage, it's still important for individuals to carefully review their insurance options and understand the specifics of how pre-existing conditions are handled under their plan.

Does Your Health Insurance Cover Freestyle Libre? A Comprehensive Guide

You may want to see also

Explore related products

![]()

Preventive Care Services: Details on coverage for routine check-ups, vaccinations, and other preventive health measures

Preventive care services are a crucial aspect of health insurance coverage in the USA, focusing on measures to maintain health and prevent diseases. Routine check-ups, vaccinations, and screenings are typically covered under preventive care, aiming to detect health issues early and promote overall wellness. For instance, annual physical exams, mammograms for women, and colonoscopies for individuals over 50 are common preventive services.

Vaccinations are another key component, with coverage for a range of vaccines from childhood immunizations like MMR and polio to adult vaccines such as the flu shot and shingles vaccine. These services are often provided at no cost to the insured, emphasizing their importance in public health.

Moreover, preventive care includes counseling and education on healthy lifestyles, such as smoking cessation programs, weight management, and nutritional advice. Some plans may also cover alternative preventive therapies like acupuncture or chiropractic care, recognizing their role in holistic health.

It's important to note that while many preventive services are fully covered, some may require a copay or deductible, depending on the specific insurance plan. Insured individuals should review their plan details to understand the extent of their preventive care coverage and any associated costs.

In summary, preventive care services are a vital part of US health insurance, offering a range of benefits designed to maintain health and prevent disease. Understanding these services and their coverage can help individuals make informed decisions about their healthcare.

Adding Dependents to United Health Insurance: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Prescription Drug Coverage: Information on how prescription medications are covered, including formularies and copay structures

Prescription drug coverage is a critical component of health insurance in the USA, as it helps to manage the costs of necessary medications. Each insurance plan typically has a formulary, which is a list of covered drugs. Drugs on this list are usually categorized into tiers, with each tier corresponding to a different copay amount. For instance, generic drugs might be on the lowest tier with the smallest copay, while brand-name drugs could be on higher tiers with larger copays.

Understanding your plan's formulary is essential because it can significantly impact your out-of-pocket expenses. If a drug you need is not on the formulary, you may have to pay the full price or seek a prior authorization to get it covered. Prior authorization is a process where your doctor must justify the medical necessity of the drug to the insurance company before it will be covered.

Copay structures can vary widely among different insurance plans. Some plans may have a flat copay for all drugs, while others may have a percentage-based copay that increases with the cost of the drug. Additionally, some plans may offer a deductible option, where you pay a certain amount out-of-pocket before the insurance coverage kicks in.

It's also important to note that prescription drug coverage can change from year to year, so it's crucial to review your plan's formulary and copay structures annually during the open enrollment period. This is the time when you can make changes to your insurance plan to better suit your needs.

In summary, prescription drug coverage is a complex but vital part of health insurance in the USA. By understanding your plan's formulary and copay structures, you can better manage your medication costs and ensure that you have access to the drugs you need.

Understanding Health Insurance Profits: Strategies, Models, and Industry Insights

You may want to see also

Explore related products

![]()

Mental Health and Substance Abuse Services: Coverage specifics for mental health treatments and substance abuse rehabilitation programs

In the United States, health insurance coverage for mental health and substance abuse services varies significantly depending on the type of insurance plan and the specific treatments required. While the Affordable Care Act (ACA) has mandated that mental health and substance abuse services be covered as essential health benefits, the extent of this coverage can differ widely among insurance providers.

For individuals seeking mental health treatment, it is crucial to understand the specifics of their insurance plan's coverage. Some plans may cover only a limited number of therapy sessions per year, while others may have more comprehensive coverage that includes both inpatient and outpatient services. Additionally, the cost-sharing requirements, such as copays and deductibles, can vary, potentially impacting the affordability of care.

Substance abuse rehabilitation programs also face unique coverage challenges. Insurance plans may impose restrictions on the types of treatments covered, such as limiting coverage for residential treatment programs or requiring prior authorization for certain medications used in addiction treatment. Furthermore, the duration of coverage for substance abuse treatment may be shorter than that for mental health services, potentially leaving individuals without adequate support during their recovery process.

Navigating the complexities of mental health and substance abuse coverage can be overwhelming for individuals and families. It is essential to carefully review the terms of one's insurance plan and, if necessary, seek assistance from a healthcare advocate or insurance navigator to ensure that all available benefits are utilized. Understanding the nuances of coverage can help individuals access the care they need and avoid unexpected financial burdens.

Understanding the 1095: Proof of Your Medical Insurance

You may want to see also

Frequently asked questions

The USA offers several types of health insurance plans, including employer-sponsored insurance, individual health insurance, health maintenance organizations (HMOs), preferred provider organizations (PPOs), and government-funded programs like Medicare and Medicaid.

Health insurance in the USA generally covers medical expenses such as doctor visits, hospital stays, prescription medications, and preventive care services. Some plans may also include coverage for dental, vision, and mental health services.

The Affordable Care Act (ACA), also known as Obamacare, has significantly impacted health insurance in the USA by expanding coverage to millions of Americans, prohibiting insurance companies from denying coverage based on pre-existing conditions, and establishing health insurance exchanges where individuals can compare and purchase plans.