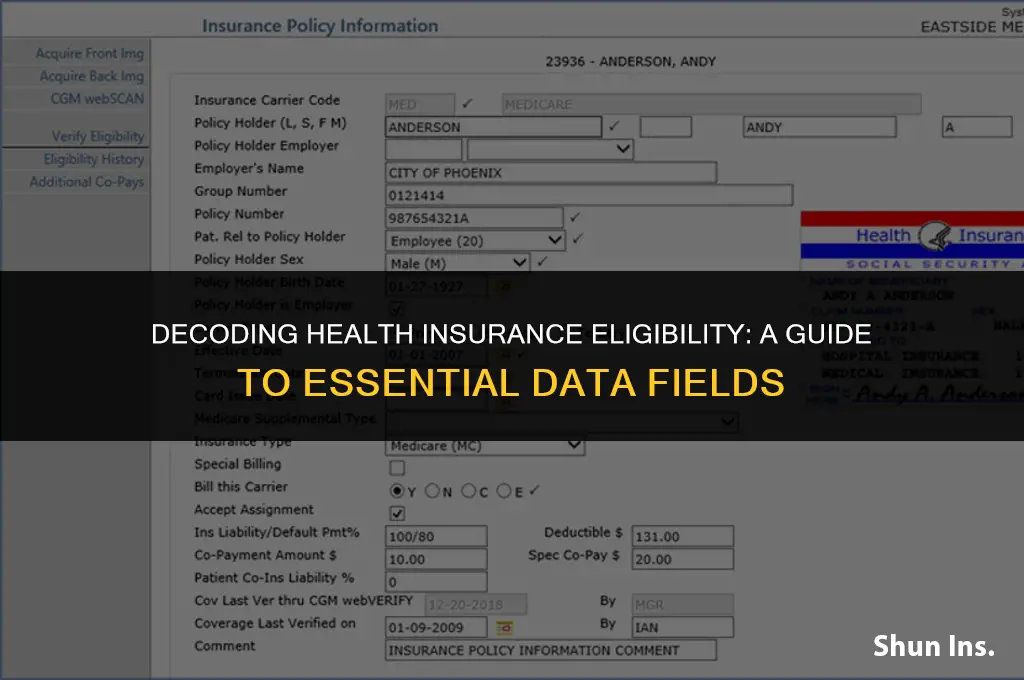

Health insurance eligibility involves several critical data fields that determine whether an individual qualifies for coverage. These fields typically include personal information such as name, date of birth, and social security number, as well as details about employment status, income level, and family size. Additionally, health insurance providers may require information about pre-existing medical conditions, previous health insurance coverage, and any government assistance programs the individual might be enrolled in. Understanding these data fields is essential for navigating the complex landscape of health insurance and ensuring that individuals receive the appropriate coverage based on their unique circumstances.

Explore related products

What You'll Learn

- Personal Information: Includes name, date of birth, social security number, and contact details

- Income Information: Contains details about income sources, amounts, and frequency for eligibility determination

- Family Composition: Lists family members, relationships, and their inclusion in the insurance plan

- Medical History: Records pre-existing conditions, disabilities, and any ongoing medical treatments

- Insurance Details: Specifies current insurance coverage, policy numbers, and expiration dates

![]()

Personal Information: Includes name, date of birth, social security number, and contact details

Personal information is a critical component of health insurance eligibility, serving as the foundation for identifying and verifying individuals. This category typically includes an individual's full legal name, date of birth, social security number (or equivalent national identifier), and contact details such as address, phone number, and email. These details are essential for insurance providers to accurately assess eligibility, process claims, and communicate with policyholders.

The collection and use of personal information in health insurance are governed by strict privacy laws and regulations, such as the Health Insurance Portability and Accountability Act (HIPAA) in the United States. These laws mandate that insurance companies protect the confidentiality and security of personal health information, ensuring that it is only used for legitimate purposes related to healthcare and insurance administration.

When applying for health insurance, individuals must provide accurate and up-to-date personal information to avoid delays or denials in coverage. Insurance providers may also require additional documentation, such as proof of identity or residency, to verify the information submitted. It is crucial for applicants to understand the importance of maintaining accurate records and notifying their insurance provider of any changes to their personal information to ensure continuous coverage.

In the context of health insurance eligibility, personal information also plays a role in determining premium rates and coverage options. Factors such as age, location, and health status can influence the cost and scope of insurance plans available to an individual. By providing accurate personal information, applicants can receive tailored quotes and select a plan that best meets their needs and budget.

Overall, personal information is a key element in the health insurance eligibility process, enabling providers to identify, verify, and serve their customers effectively while adhering to legal and regulatory requirements.

Choosing the Right Health Insurance: A Comprehensive Guide for You

You may want to see also

Explore related products

![]()

Income Information: Contains details about income sources, amounts, and frequency for eligibility determination

Income information is a critical component in determining eligibility for health insurance. This data field includes details about an individual's income sources, the amounts earned, and the frequency of these earnings. Insurance providers use this information to assess whether an individual qualifies for certain health insurance plans, subsidies, or assistance programs. For instance, Medicaid eligibility often depends on income levels, and the Affordable Care Act (ACA) uses income to calculate premium tax credits.

The specific details required in the income information section can vary. Generally, it includes gross income from all sources such as wages, salaries, tips, bonuses, and overtime pay. It may also encompass income from self-employment, rental properties, investments, and other financial activities. Additionally, the frequency of income, such as hourly, weekly, bi-weekly, monthly, or annually, is essential for accurate eligibility determination.

When applying for health insurance, individuals must provide documentation to verify their income. This can include pay stubs, tax returns, or letters from employers. For self-employed individuals, business income statements or tax returns may be necessary. Ensuring the accuracy of this information is crucial, as discrepancies can lead to incorrect eligibility determinations, potentially resulting in denied coverage or financial penalties.

Moreover, changes in income must be reported promptly to the insurance provider. This is because fluctuations in earnings can impact eligibility status. For example, a significant decrease in income might qualify an individual for Medicaid or other assistance programs, while an increase could affect subsidy amounts or even result in the loss of certain benefits.

In conclusion, the income information section is a vital part of the health insurance eligibility process. It requires careful attention to detail and accurate reporting to ensure that individuals receive the appropriate coverage and benefits based on their financial circumstances.

McCain's Health Insurance Plan: Coverage Details and Benefits Explained

You may want to see also

Explore related products

![Prime Screen 7 Panel Oral Saliva Drug Test Kit [5 Pack], Employment and Insurance Testing (AMP, COC, MET, OPI, OXY, PCP, THC) - ODOA-376](https://m.media-amazon.com/images/I/71HZu04wGYL._AC_UL320_.jpg)

![]()

Family Composition: Lists family members, relationships, and their inclusion in the insurance plan

Family composition plays a critical role in determining health insurance eligibility and coverage. Insurance plans often require detailed information about family members, their relationships to the primary insured, and whether they are included in the plan. This data helps insurers assess risk, calculate premiums, and ensure that all eligible dependents are covered.

When listing family members, it's essential to include the primary insured's spouse or domestic partner, children, and any other dependents who may qualify for coverage. Relationships must be clearly defined, as different types of relationships (e.g., married, common-law, adopted) may have different implications for eligibility and benefits. For example, a child may be eligible for coverage until a certain age or until they are no longer a dependent, while a spouse or domestic partner may be eligible for coverage as long as they are married or in a registered domestic partnership.

Inclusion in the insurance plan is another crucial aspect of family composition. Insurers need to know which family members are actively enrolled in the plan and which are not. This information is used to determine the total premium cost and to ensure that all enrolled members receive the appropriate benefits. It's important to note that changes in family composition, such as the birth of a child or the end of a marriage, may require updates to the insurance plan to ensure that coverage remains accurate and up-to-date.

In addition to the basic information about family members and their relationships, insurers may also require additional details such as social security numbers, dates of birth, and proof of dependency. This information is used to verify eligibility and to prevent fraud. It's important to provide accurate and complete information to avoid any delays or issues with coverage.

Overall, understanding and accurately reporting family composition is essential for ensuring that all eligible family members receive the appropriate health insurance coverage. By providing detailed and up-to-date information, individuals can help insurers assess risk, calculate premiums, and deliver the best possible service to their clients.

Insurance Companies Utilizing CCC Valuescope for Accurate Claims Assessments

You may want to see also

Explore related products

![]()

Medical History: Records pre-existing conditions, disabilities, and any ongoing medical treatments

Medical history is a critical component of health insurance eligibility, as it provides insurers with essential information about an individual's health status. This section of the insurance application typically includes details about pre-existing conditions, disabilities, and ongoing medical treatments. Insurers use this information to assess the risk associated with providing coverage and to determine the appropriate premium rates.

When filling out the medical history section, it's important to be thorough and accurate. This may involve reviewing medical records and consulting with healthcare providers to ensure that all relevant information is included. Some common pre-existing conditions that may need to be disclosed include diabetes, heart disease, and asthma. Disabilities, such as mobility impairments or mental health conditions, should also be reported. Additionally, any ongoing medical treatments, such as prescription medications or physical therapy, should be listed.

The medical history section may also ask about previous hospitalizations, surgeries, or diagnostic tests. It's important to provide detailed information about these events, including dates, locations, and the reasons for the hospitalizations or tests. This information helps insurers to better understand the individual's health history and to make informed decisions about coverage.

In some cases, insurers may require additional information or documentation to support the medical history provided in the application. This may include medical records, doctor's notes, or test results. It's important to be prepared to provide this information promptly to avoid delays in the insurance application process.

Overall, the medical history section is a crucial part of the health insurance eligibility process. By providing accurate and detailed information, individuals can help to ensure that they receive the appropriate coverage and premium rates for their health insurance needs.

Ohio Medical Assistance: Can It Subsidize Insurance Premiums?

You may want to see also

Explore related products

![]()

Insurance Details: Specifies current insurance coverage, policy numbers, and expiration dates

Insurance details are a critical component of health insurance eligibility, providing essential information about an individual's current coverage status. This section specifies the current insurance coverage, policy numbers, and expiration dates, which are vital for determining eligibility for new policies or changes to existing ones.

The current insurance coverage field indicates whether the individual is currently insured, and if so, what type of coverage they have. This could include employer-sponsored insurance, individual plans, or government-provided coverage such as Medicare or Medicaid. The policy numbers field contains the unique identifiers for each insurance policy, allowing insurers to quickly access and verify the individual's coverage history and claims.

Expiration dates are equally important, as they indicate when the current coverage will end. This information is crucial for individuals who are transitioning between policies or who may be at risk of losing coverage. By providing these details, insurers can ensure that there is no lapse in coverage and that the individual remains protected.

When filling out insurance details, it's essential to be accurate and thorough. Any errors or omissions could lead to delays in processing or even denial of coverage. Individuals should have their current insurance cards or policy documents on hand to ensure they can provide the correct information.

In addition to the basic insurance details, some forms may also ask for information about the individual's insurance history, including any previous policies or claims. This information can help insurers assess the individual's risk profile and determine the most appropriate coverage options.

Overall, the insurance details section is a critical part of the health insurance eligibility process, providing insurers with the necessary information to make informed decisions about coverage. By understanding the importance of this section and providing accurate information, individuals can help ensure a smooth and successful insurance application process.

Understanding Insurance Coverage: Doctor or Medical Group?

You may want to see also

Frequently asked questions

The primary data fields required to determine health insurance eligibility typically include personal information such as name, date of birth, social security number, and contact details. Additionally, information regarding employment status, income level, and family size may also be necessary to assess eligibility for certain programs.

Employment status plays a significant role in health insurance eligibility. Individuals who are employed full-time may be eligible for employer-sponsored health insurance plans. Those who are unemployed or work part-time may qualify for Medicaid or other state-funded programs, depending on their income level and family size.

Income level is a crucial factor in determining health insurance eligibility. Many health insurance programs, such as Medicaid and the Children's Health Insurance Program (CHIP), have income thresholds that applicants must meet to qualify for coverage. Additionally, individuals with lower incomes may be eligible for subsidies to help cover the cost of private health insurance plans purchased through health insurance exchanges.