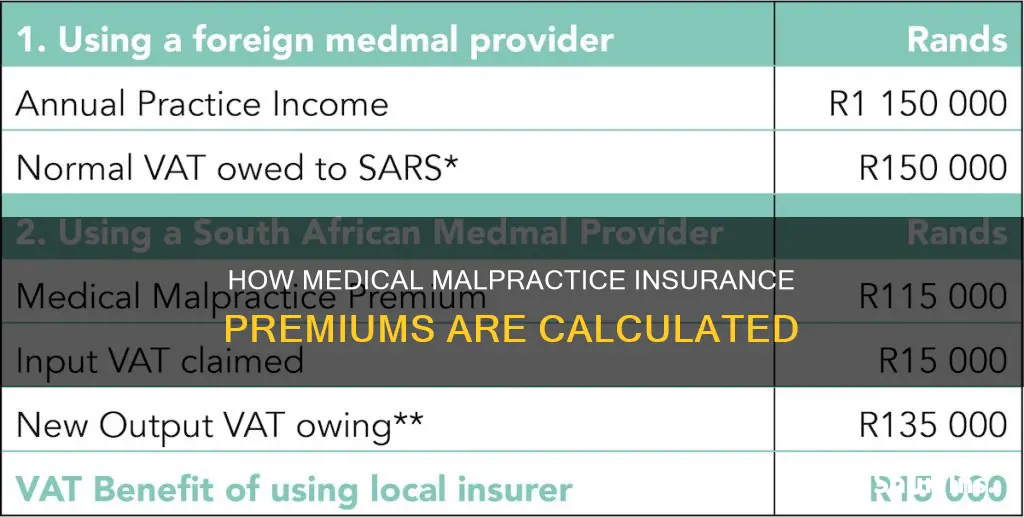

The cost of medical malpractice insurance is determined by a variety of factors, including the type of medical practice, the physician's specialty, geographic location, claims history, and the legal environment of the state in which they practice. Physicians in high-risk specialties, such as surgery, or those with a history of multiple claims, face significantly higher premiums due to the increased likelihood of litigation and financial payouts. Conversely, doctors in low-risk specialties, with fewer or no claims, and proactive risk management strategies benefit from lower premiums. Additionally, state regulations, including tort reform laws, and local legal environments influence premium costs, with some states, such as New York, known for their high premiums due to the absence of tort reform and a high frequency of medical malpractice claims.

| Characteristics | Values |

|---|---|

| Specialty | Obstetricians/gynecologists, neurosurgeons, orthopedic surgeons, and ER doctors are considered high-risk specialties. |

| Geographic location | Premiums vary between states and regions within states. States like New York, Florida, and Illinois are known for their high premiums due to the legal environment and high frequency of medical malpractice claims. |

| Claims history | A history of multiple claims, especially those resulting in large payouts, will lead to higher premiums. |

| Risk management practices | Implementing proactive risk management strategies can help lower premiums. |

| State laws and regulations | States with tort reform laws that limit damages from malpractice lawsuits tend to have lower premiums. |

| Type of practice | Surgical practices are considered higher risk and result in higher premiums. |

| Coverage amount | Physicians who require more coverage or coverage across multiple states will pay higher premiums. |

Explore related products

What You'll Learn

![]()

Specialty of the physician

A physician's specialty is a significant factor in determining the cost of their medical malpractice insurance premiums. Doctors in high-risk specialties, such as obstetrics/gynaecology (OB/GYN), neurosurgery, thoracic surgery, and orthopedic surgery, face the highest premiums due to an increased likelihood of complications and lawsuits. For example, obstetricians/gynaecologists in New York paid annual premiums of up to $215,000 in 2017, while their counterparts in California paid around $50,000. Similarly, in Miami-Dade County, Florida, OB/GYNs may pay up to $218,000 per year.

The nature of the work in these high-risk specialties contributes to the elevated premiums. For instance, surgeons and anesthesiologists, who perform invasive procedures, are more likely to encounter complications and, consequently, legal claims. As a result, their insurance costs are higher than those of non-surgical specialties or specialties that perform minor procedures, such as dermatology or internal medicine.

The risk associated with a specialty is further reflected in the frequency and severity of claims. Specialties with a higher claim frequency and a history of substantial settlements or jury awards will generally face higher premiums. For example, neurosurgeons have been found to pay the most in settlements, influencing the premiums for this specialty. Conversely, physicians in low-risk specialties, such as primary care and psychiatry, typically pay much lower premiums due to the lower likelihood of litigation.

Additionally, the size of a physician's practice can also impact their insurance costs. Larger practices with multiple doctors and support staff may encounter higher premiums due to the increased risk of malpractice claims and the complexities of oversight and coordination.

While specialty is a significant factor, it is important to note that other elements, such as geographic location, claims history, and coverage limits, also play a role in determining medical malpractice insurance premiums.

Houston Students: Buying the Right Medical Insurance

You may want to see also

Explore related products

![]()

Geographic location

For example, New York is known for having high insurance premiums due to its legal environment and high frequency of medical malpractice claims. The absence of tort reform laws in New York means there are no caps on economic or non-economic damages, resulting in higher premiums. In 2023, New York had the highest value of direct premiums earned by the medical professional liability insurance market in the United States, amounting to over $1.6 billion.

In contrast, states like North Dakota have favourable tort laws, including caps on non-economic damages, which help keep premiums lower. Physicians in North Dakota also benefit from lower rates of wages, living expenses, and healthcare costs, which contribute to reduced malpractice insurance premiums.

Even within a state, premiums can vary between regions. For instance, in New York, physicians in New York City face some of the highest premiums in the country, while metro areas like Buffalo and Albany have slightly lower but still elevated premiums.

The cost of medical malpractice insurance in a specific geographic location is influenced by the local legal landscape, the frequency of claims, and the presence or absence of tort reforms. These factors collectively contribute to the variability of premiums across different states and regions within the United States.

Heart Check-ups: Are You Covered by Your Medical Insurance?

You may want to see also

Explore related products

![]()

Claims history

The impact of claims history on premiums is influenced by several factors. Firstly, the type and volume of procedures performed affect the likelihood of claims. Physicians in high-risk specialties, such as surgery or emergency medicine, tend to face higher premiums due to the increased risk of complications and lawsuits.

Secondly, the quality of patient communication is essential. Poor communication can increase the risk of misunderstandings, disputes, and legal actions. Effective communication builds trust and can help prevent malpractice claims.

Thirdly, implementing risk management strategies, such as following best practices, adhering to medical guidelines, and participating in ongoing training, is crucial. Insurers view these proactive measures favorably and may offer lower premiums to physicians who actively manage risk.

Additionally, the geographic location of a physician's practice impacts premiums due to variations in local legal environments, malpractice claim prevalence, and state-specific reforms. States like New York, with no tort reform and higher malpractice claims, have significantly higher premiums than states with tort laws and damage caps, such as North Dakota.

Lastly, the type of malpractice insurance policy held by a physician can affect premiums. "Claims-made" insurance covers malpractice claims only if the same insurance company is retained from the incident date to the claim filing date. In contrast, "occurrence-made" insurance provides seamless coverage regardless of job or location changes, covering claims provided the insurer was the carrier at the time of the incident. Physicians should carefully consider their insurance type, as additional tail coverage may be needed when switching carriers to ensure continuous protection.

Vets in Tyler, Texas: Using Medical Insurance for Pets?

You may want to see also

Explore related products

![]()

Risk associated with the work

The cost of medical malpractice insurance is largely determined by the risks associated with the type of work. The specialty of the physician is the most significant factor, with doctors in high-risk specialties facing higher premiums. These include OB/GYN, neurosurgery, orthopedic surgery, and emergency medicine. Such specialties carry an increased likelihood of complications and lawsuits, driving up insurance costs. Conversely, physicians in low-risk specialties, such as primary care and psychiatry, typically pay lower premiums due to the reduced risk of claims.

Invasive procedures also contribute to risk levels. Specialists who perform invasive procedures, like surgeons or anesthesiologists, face higher premiums than those in non-surgical specialties or those performing minor procedures, such as dermatology or internal medicine. The nature of the procedures and the potential for adverse outcomes significantly influence the cost of malpractice insurance.

Geographic location is another critical factor in determining the cost of medical malpractice insurance. Premiums vary significantly between states and regions within states. Local legal environments, the prevalence of medical malpractice claims, and state-specific reforms influence these variations. For example, states like New York, Florida, and Illinois are known for their high premiums due to their legal environment and the frequency of medical malpractice claims. The metro areas of New York City, Buffalo, and Albany have notably high premiums.

In addition to location and specialty, a physician's claims history is a key consideration. Insurers view doctors with multiple claims or large payouts as higher risks, leading to significantly higher premiums. Even a single large claim can substantially increase insurance costs, as it indicates a higher likelihood of future incidents. Conversely, a clean claims history can help lower premiums, along with proactive risk management strategies and lower claim frequencies.

The cost of malpractice insurance is a complex interplay of various factors, all of which contribute to the overall risk assessment. By understanding these factors, physicians can make informed decisions about their insurance choices and manage their costs effectively.

Strategies for Tracking DPSS Medical Insurance Coverage

You may want to see also

Explore related products

![]()

State laws and tort reform

Tort reform refers to changes in personal injury law aimed at reducing the number of medical malpractice lawsuits and the overall cost of healthcare. These reforms can directly impact insurance premiums by limiting the financial damages awarded in malpractice lawsuits. By capping non-economic damages, states can reduce the cost of malpractice insurance. For instance, Texas enacted tort reform in the early 2000s, which included a $250,000 cap on non-economic damages. This reduced the number of "frivolous" lawsuits, lowered medical liability premiums, and improved patient access to doctors.

However, the effectiveness of tort reforms in reducing insurance premiums is debated. Some studies suggest that tort reforms have not translated into significant insurance savings. The American Bar Association (ABA) opposes tort reform, arguing that it restricts patient rights by limiting the amount of financial recovery through damage caps. Additionally, opponents argue that limiting malpractice liability may not significantly impact healthcare spending.

While tort reforms can influence insurance premiums, other state-specific factors also come into play. The frequency and severity of claims, specialty practices, and geographic location all contribute to the variation in malpractice insurance premiums across states. Ultimately, state laws and tort reforms are crucial factors in shaping the landscape of medical malpractice insurance, but they interact with other elements to determine the final cost of coverage.

Montclair State: Medical Insurance Availability and Benefits

You may want to see also

Frequently asked questions

Medical malpractice insurance helps medical professionals cover legal costs in the event of a lawsuit.

The premiums for medical malpractice insurance are determined by the risks associated with the type of work. Factors such as specialty, geographic location, claims history, and state regulations play a significant role in determining the cost of premiums.

Doctors in high-risk specialties, such as obstetrics/gynecology, neurosurgery, orthopedic surgery, and emergency medicine, typically face the highest premiums due to the increased likelihood of complications and lawsuits.

Location can significantly impact premiums due to factors like local legal environments, the prevalence of medical malpractice claims, and state-specific reforms or their absence. For example, New York is known for its high premiums due to the absence of tort reform and a high frequency of medical malpractice claims.