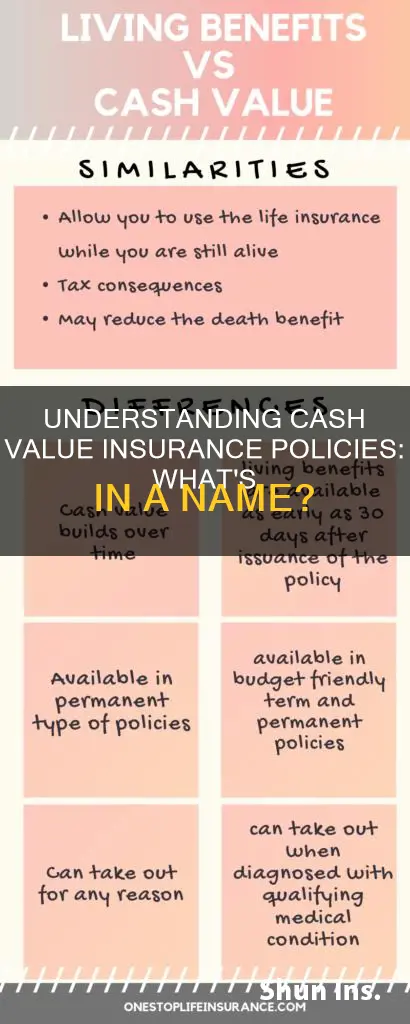

Cash value life insurance is a type of permanent life insurance that features a cash value savings component. It is sometimes referred to as ordinary life or straight life. This type of insurance policy allows the policyholder to withdraw money from their policy or borrow against the accumulated cash value. Cash value life insurance is more expensive than term life insurance as part of the payment goes towards savings. There are several types of cash value life insurance policies, including whole life insurance, variable life insurance, and universal life insurance.

Explore related products

What You'll Learn

![]()

Permanent life insurance

The two primary types of permanent life insurance are whole life and universal life. The cash value of whole life insurance grows at a guaranteed rate, while universal life insurance features more flexible premium options and its earnings are based on market interest rates. Variable life and variable universal life provide expanded options to invest the cash value in mutual funds and other financial instruments. Whole life insurance is also called "ordinary life" or "straight life", and the premium depends on the age of the buyer. The younger the buyer, the lower the premium as they will pay into it for longer. Universal life insurance is also called "flexible premium adjustable life insurance", and it lets the policyholder save money that grows tax-free.

Private Insurance in the US: How Many Are Covered?

You may want to see also

Explore related products

![]()

Whole life insurance

When considering whole life insurance, it is important to weigh the costs and benefits against those of alternative options, such as term life insurance. Whole life insurance may be a suitable choice for individuals seeking permanent coverage, fixed premiums, and access to cash value during their lifetime. By consulting with licensed agents and considering their lifestyle, health, family situation, and future goals, individuals can make informed decisions about their insurance choices.

Private vs Public Insurance: What's the Real Difference?

You may want to see also

Explore related products

![]()

Universal life insurance

One key difference between universal life insurance and whole life insurance is that universal life insurance allows the policyholder to change the value of premium payments. This adjustability can be advantageous for individuals in different seasons of life. Additionally, with universal life insurance, the death benefit can be scaled up or down according to unique circumstances.

Variable Universal Life Insurance offers the same lifetime protection and payment flexibility as standard universal life insurance, with the added benefit of more investment options. Policyholders can invest part or all of their cash value in "subaccounts," but this comes with increased risk, including the possibility of losing the principal amount.

Overall, universal life insurance provides policyholders with a flexible way to obtain permanent life insurance coverage while building cash value over time.

Private Insurance: Individual Benefits and Coverage Explained

You may want to see also

Explore related products

![]()

Variable life insurance

Life insurance with a cash value component is known as "cash value life insurance". Whole life, variable life, and universal life insurance are examples of cash value life insurance. Term insurance, on the other hand, is not a type of cash value insurance.

Huntington Bank Accounts: Are They Insured?

You may want to see also

Explore related products

![]()

Indexed universal life insurance

Life insurance with cash value is a form of permanent life insurance that features a cash value savings component. Whole life, variable life, and universal life insurance are all examples of cash-value life insurance. Indexed universal life (IUL) insurance is a type of universal life insurance that provides a cash value component along with a death benefit.

IUL insurance lets the policyholder decide how much cash value to assign to an equity-indexed account and to a fixed-rate account, if available. The money in a policyholder's cash value account can earn interest by tracking a stock market index selected by the insurer, such as the Nasdaq-100 or the Standard & Poor's 500. The interest rate derived from the equity index account can fluctuate, but the policy offers an interest rate guarantee, which limits losses. It may also cap your gains.

IUL policies are more volatile than fixed universal life policies but are less risky than variable UL insurance policies because IUL does not invest in equity positions. IUL policies usually cap your returns but also guarantee a minimum interest rate. As with universal life insurance, IUL policies have adjustable premiums. You can underpay or skip premiums, and you may be able to adjust your death benefit.

IUL insurance offers permanent, lifelong coverage when premiums are kept up to date. It also offers flexible premiums and a death benefit that may also be flexible. The cash value can be invested in an equity index account or a fixed-interest option. IUL insurance also offers the ability to borrow against the cash value accumulated in the policy. However, if the loans are not paid back, they are deducted from the death benefit.

IUL policies are more expensive than other types of life insurance due to higher premium costs and potential fees. They are best suited for high-net-worth individuals seeking supplementary retirement income or life insurance.

Key Bank and Federal Deposit Insurance: What You Need to Know

You may want to see also

Frequently asked questions

Cash value insurance is a form of permanent life insurance that lasts for the lifetime of the holder and features a cash value savings component. The policyholder can use the cash value for various purposes, including borrowing or withdrawing cash from it, or using it to pay policy premiums.

There are three types of cash value life insurance policies: whole life insurance, universal life insurance, and variable life insurance. Whole life insurance offers a fixed premium and guarantees a minimum death benefit. Universal life insurance allows the policyholder to change the value of premium payments and scale the death benefit up or down. Variable life insurance uses investments, with the death benefit and cash values varying based on the performance of the investments.

Cash value insurance offers a combination of protection and savings, providing financial flexibility during the lifetime of the policyholder. The cash value can be used to pay premiums, as a source of income, or to increase the death benefit. Withdrawals from the cash value are typically tax-free, and the cash value can grow tax-deferred.