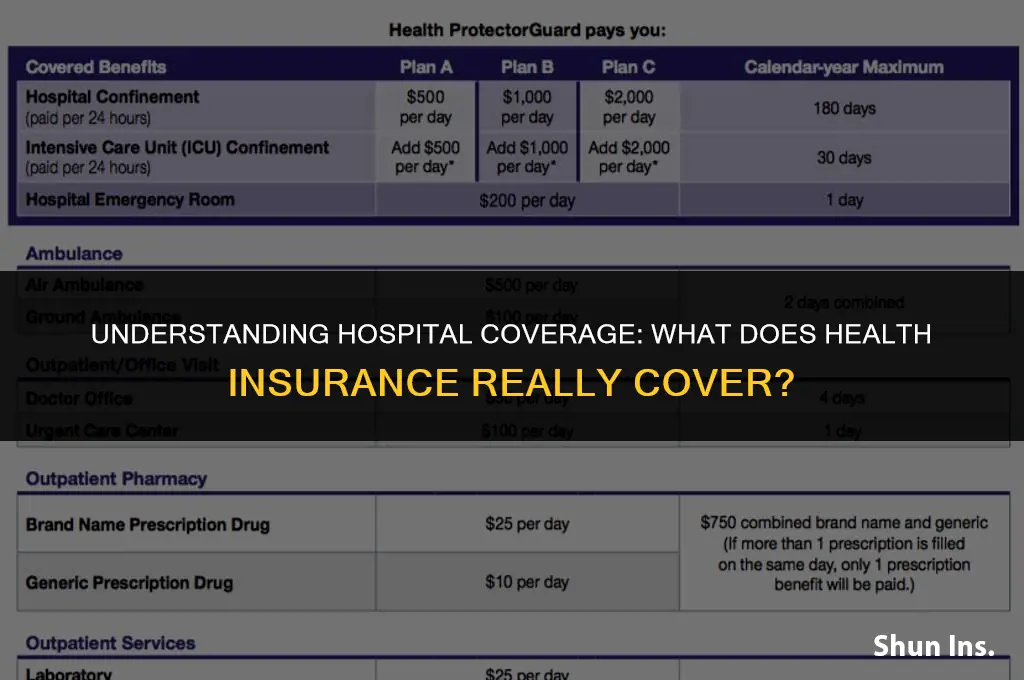

Health insurance coverage in hospitals is a critical aspect of ensuring access to quality healthcare. It typically includes a range of services such as inpatient care, outpatient services, emergency room visits, and various medical procedures. Depending on the specific policy, health insurance may also cover prescription medications, laboratory tests, and diagnostic imaging. Understanding what health insurance covers in hospitals is essential for individuals to make informed decisions about their healthcare needs and to avoid unexpected financial burdens. This paragraph will delve into the specifics of health insurance coverage, exploring the different types of plans available and the extent of their coverage in hospital settings.

| Characteristics | Values |

|---|---|

| Inpatient care | Coverage for hospital stays, including room and board |

| Outpatient care | Coverage for services received outside of a hospital, such as doctor visits |

| Emergency services | Coverage for urgent medical care, including ambulance rides |

| Prescription drugs | Coverage for medications prescribed by a doctor |

| Diagnostic tests | Coverage for tests and procedures to diagnose a medical condition |

| Rehabilitation services | Coverage for physical therapy and other forms of rehabilitation |

| Mental health services | Coverage for counseling and other mental health treatments |

| Preventive care | Coverage for routine check-ups and screenings to prevent illness |

| Maternity care | Coverage for pregnancy-related services, including childbirth |

| Pediatric care | Coverage for medical services for children |

| Dental care | Coverage for dental procedures and check-ups |

| Vision care | Coverage for eye exams and corrective lenses |

| Alternative medicine | Coverage for treatments such as acupuncture and chiropractic care |

| Home health care | Coverage for medical services provided in the home |

| Hospice care | Coverage for end-of-life care |

| Long-term care | Coverage for extended stays in a nursing home or other long-term care facility |

Explore related products

What You'll Learn

- Inpatient Services: Coverage for hospital stays, including room and board, nursing care, and medical treatments

- Emergency Care: Insurance for urgent medical attention, such as ambulance services, ER visits, and urgent surgeries

- Diagnostic Tests: Coverage for various tests and procedures, including blood work, imaging studies, and pathology exams

- Surgical Procedures: Insurance for planned surgeries, including pre-operative care, the surgery itself, and post-operative recovery

- Prescription Medications: Coverage for medications prescribed during hospital stays, including intravenous drugs and other treatments

![]()

Inpatient Services: Coverage for hospital stays, including room and board, nursing care, and medical treatments

Inpatient services are a critical component of health insurance coverage, providing financial protection for individuals during hospital stays. This coverage typically includes room and board, nursing care, and medical treatments, ensuring that patients receive comprehensive care without incurring substantial out-of-pocket expenses. However, the specifics of inpatient coverage can vary significantly depending on the insurance plan, with some policies imposing limitations on the duration of stays or the types of treatments covered.

When considering inpatient services, it's essential to understand the different types of hospital stays that may be covered. These can range from routine procedures, such as childbirth or elective surgeries, to emergency admissions resulting from accidents or severe illnesses. Insurance plans may also differentiate between inpatient and outpatient services, with inpatient care generally requiring an overnight stay in the hospital.

The cost of inpatient services can be a significant factor in choosing a health insurance plan. Deductibles, copayments, and coinsurance are common cost-sharing mechanisms used by insurers to manage expenses. Patients may be responsible for a deductible before their coverage kicks in, followed by a copayment or coinsurance for each service received. It's crucial to review these costs and understand how they apply to different types of inpatient care.

Another important aspect of inpatient coverage is the quality of care provided. Health insurance companies often have networks of preferred hospitals and healthcare providers, which can impact the level of care and the out-of-pocket costs for patients. Choosing a plan with a robust network of high-quality hospitals can be beneficial, especially for individuals with complex medical needs.

In conclusion, inpatient services are a vital part of health insurance coverage, offering financial protection and access to necessary medical care during hospital stays. By understanding the specifics of inpatient coverage, including the types of stays, cost-sharing mechanisms, and quality of care, individuals can make informed decisions when selecting a health insurance plan that meets their needs.

Does Colonial Penn Offer Health Insurance? Exploring Coverage Options

You may want to see also

Explore related products

![]()

Emergency Care: Insurance for urgent medical attention, such as ambulance services, ER visits, and urgent surgeries

In the event of a medical emergency, timely access to care can be a matter of life and death. Health insurance plans typically cover emergency care, which includes ambulance services, emergency room (ER) visits, and urgent surgeries. This coverage is crucial as it ensures that individuals can receive immediate medical attention without the burden of upfront costs.

Ambulance services are generally covered under emergency care provisions. This means that if you require transportation to a hospital due to a medical emergency, your health insurance will likely cover the cost of the ambulance ride. It's important to note that some plans may have stipulations regarding the use of ambulance services, such as requiring prior authorization or limiting coverage to certain types of emergencies.

Emergency room visits are another key component of emergency care coverage. If you experience a sudden illness or injury that requires immediate attention, your health insurance will typically cover the costs associated with an ER visit. This includes the facility fees, physician services, and any necessary diagnostic tests or treatments. However, it's essential to be aware that some health plans may impose copays or deductibles for ER visits, especially if the visit is deemed non-emergency by the healthcare provider.

Urgent surgeries are also usually covered under emergency care. If you require a surgical procedure to address a life-threatening condition or severe injury, your health insurance will generally cover the costs of the surgery, including the surgeon's fees, anesthesia, and hospital stay. As with other emergency services, there may be limitations or requirements that need to be met, such as obtaining prior approval from your insurance provider.

When it comes to emergency care, it's vital to understand the specifics of your health insurance plan. Familiarize yourself with the coverage details, including any exclusions, limitations, or requirements for prior authorization. This knowledge can help ensure that you're prepared in the event of a medical emergency and can navigate the healthcare system more effectively.

Super Visa Medical Insurance: What's the Cost?

You may want to see also

Explore related products

![]()

Diagnostic Tests: Coverage for various tests and procedures, including blood work, imaging studies, and pathology exams

Health insurance coverage for diagnostic tests in hospitals can vary widely depending on the specific policy and the type of test required. Generally, most health insurance plans cover a range of diagnostic tests and procedures, including blood work, imaging studies, and pathology exams, but the extent of coverage and any associated costs can differ significantly.

Blood work is typically covered by health insurance, as it is a fundamental diagnostic tool used to assess a patient's overall health and identify potential issues. Common blood tests, such as complete blood counts (CBC), blood chemistry panels, and lipid profiles, are usually included in standard health insurance plans. However, more specialized tests, such as genetic testing or certain infectious disease screenings, may require prior authorization or may not be covered at all.

Imaging studies, such as X-rays, CT scans, and MRIs, are also generally covered by health insurance, but the coverage may be subject to certain conditions. For example, some plans may require prior authorization for certain types of imaging studies, or they may impose limits on the number of studies that can be performed within a certain timeframe. Additionally, the cost-sharing for imaging studies can vary, with some plans requiring higher copays or coinsurance for more expensive procedures.

Pathology exams, which involve the analysis of tissues and cells to diagnose diseases, are typically covered by health insurance as well. This includes common procedures such as biopsies and Pap smears. However, as with other diagnostic tests, the coverage may be subject to certain limitations or requirements, such as prior authorization or cost-sharing provisions.

It is important for individuals to review their specific health insurance policy to understand the coverage for diagnostic tests and procedures. This can help ensure that they are prepared for any potential costs or limitations when seeking medical care. Additionally, healthcare providers can often assist patients in navigating their insurance coverage and advocating for necessary diagnostic tests.

Your Guide to Applying for Health Insurance in Kentucky

You may want to see also

Explore related products

![]()

Surgical Procedures: Insurance for planned surgeries, including pre-operative care, the surgery itself, and post-operative recovery

Health insurance coverage for surgical procedures typically encompasses a range of services associated with planned surgeries. This includes pre-operative care, which involves consultations with surgeons and anesthesiologists, diagnostic tests, and any necessary medications. The surgery itself is covered, including the cost of the operating room, surgical team, and any implants or devices used during the procedure. Post-operative recovery is also included, covering hospital stays, follow-up appointments, physical therapy, and medications to manage pain and prevent infection.

It's important to note that while many health insurance plans cover surgical procedures, there may be limitations and exclusions. For example, some plans may require pre-authorization for certain surgeries or may not cover elective procedures. Additionally, the coverage may vary depending on the type of surgery and the reason it is being performed. For instance, a surgery to correct a congenital condition may be covered differently than a cosmetic surgery.

When planning for a surgery, it's crucial to understand your insurance coverage and any potential out-of-pocket costs. This includes deductibles, copayments, and coinsurance. It's also important to be aware of any network restrictions, as some insurance plans may only cover surgeries performed by in-network providers.

To ensure you have a clear understanding of your coverage, it's recommended to contact your insurance provider directly. They can provide you with detailed information about what is covered, what is not, and any steps you need to take to ensure your surgery is properly authorized and billed.

In summary, health insurance coverage for surgical procedures is comprehensive but may come with certain limitations and requirements. By understanding your coverage and planning accordingly, you can help ensure that your surgery is as financially manageable as possible.

Does Washington Offer Free Health Insurance? Exploring Coverage Options

You may want to see also

Explore related products

![]()

Prescription Medications: Coverage for medications prescribed during hospital stays, including intravenous drugs and other treatments

During a hospital stay, patients often receive a variety of prescription medications, including intravenous drugs and other treatments. These medications are typically covered by health insurance, but the extent of coverage can vary depending on the specific policy and the circumstances of the hospitalization. It's important for patients to understand their insurance coverage to avoid unexpected costs.

One key aspect of prescription medication coverage is the formulary, which is a list of drugs that the insurance plan covers. Drugs not on the formulary may not be covered, or may require prior authorization from the insurance company. Patients should review their insurance plan's formulary to ensure that any medications they are currently taking or may need during a hospital stay are included.

Another factor that can affect coverage is the method of administration. Intravenous drugs, for example, may be covered differently than oral medications. Some insurance plans may require a copay or coinsurance for certain types of medications, regardless of whether they are administered in the hospital or at home. Patients should be aware of these potential costs and discuss them with their healthcare provider and insurance company.

In addition to the specific medications, the length of the hospital stay can also impact coverage. Some insurance plans may limit the number of days that certain medications are covered, or may require prior authorization for extended stays. Patients should be aware of these limitations and work with their healthcare provider to develop a plan for managing their medications after discharge.

Finally, it's important for patients to keep track of their medication usage during a hospital stay. This can help ensure that they receive the correct medications and dosages, and can also help with billing and insurance claims. Patients should ask their healthcare provider for a list of all medications they received during their stay, including the name, dosage, and frequency of each medication.

By understanding their insurance coverage for prescription medications during a hospital stay, patients can better manage their healthcare costs and ensure that they receive the necessary treatments without unexpected financial burdens.

Discover Affordable Health Insurance Options for Your Budget and Needs

You may want to see also

Frequently asked questions

Health insurance usually covers a range of hospital services including inpatient care, outpatient services, emergency room visits, surgical procedures, diagnostic tests, and prescription medications administered within the hospital.

Yes, some health insurance plans may not cover certain hospital services such as cosmetic surgery, alternative treatments, or services deemed experimental. It's important to check with your insurance provider for specific exclusions.

Health insurance coverage can vary depending on whether the hospital is in-network or out-of-network with your insurance provider. In-network hospitals typically have negotiated rates with the insurer, leading to lower out-of-pocket costs for the patient. Out-of-network hospitals may be covered, but at a higher cost to the patient.

Common out-of-pocket expenses for hospital visits include deductibles, copayments, coinsurance, and any costs for services not covered by your insurance plan. These expenses can add up quickly, so it's important to understand your insurance coverage and potential costs before receiving hospital care.