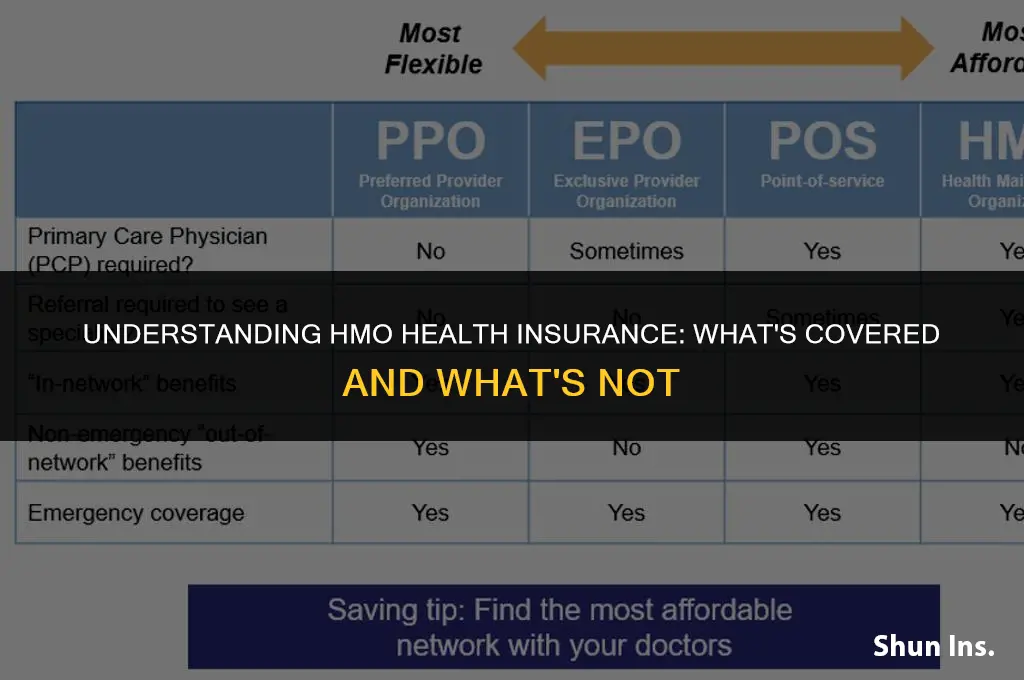

Health Maintenance Organization (HMO) health insurance is a type of managed care plan that provides comprehensive medical coverage to its members. HMOs typically cover a wide range of healthcare services, including preventive care, such as annual check-ups and vaccinations, as well as treatment for illnesses and injuries. They often require members to choose a primary care physician (PCP) who acts as a gatekeeper for referrals to specialists and other healthcare providers. HMO plans may also include prescription drug coverage, mental health services, and dental care, depending on the specific plan and provider. Understanding what an HMO covers can help individuals make informed decisions about their healthcare options and ensure they receive the necessary care while managing their health expenses effectively.

| Characteristics | Values |

|---|---|

| Coverage Type | HMO (Health Maintenance Organization) |

| Network | Limited to HMO network providers |

| Referrals | Required for specialist care |

| Premiums | Generally lower than other plans |

| Deductibles | Typically low or no deductibles |

| Co-payments | Fixed co-payments for covered services |

| Preventive Care | Often covered at no cost |

| Prescription Drugs | Usually covered with co-payments |

| Hospitalization | Covered, but may require pre-authorization |

| Out-of-Network Care | Not typically covered, except in emergencies |

Explore related products

What You'll Learn

- Preventive Care: Coverage for routine check-ups, vaccinations, and screenings to prevent illnesses

- Primary Care: Visits to general practitioners, family doctors, and pediatricians for non-specialized medical care

- Specialist Care: Referrals to specialists for specific medical conditions or treatments

- Hospital Services: Inpatient and outpatient services, including surgeries, lab tests, and imaging

- Prescription Drugs: Coverage for medications prescribed by healthcare providers

![]()

Preventive Care: Coverage for routine check-ups, vaccinations, and screenings to prevent illnesses

Preventive care is a cornerstone of maintaining good health and is fully recognized by HMO health insurance plans. Coverage typically includes routine check-ups, vaccinations, and screenings designed to detect and prevent illnesses before they become serious. For instance, annual physical exams are usually covered, providing an opportunity for healthcare providers to assess overall health, update immunizations, and screen for conditions such as high blood pressure, diabetes, and certain cancers.

Vaccinations are another critical component of preventive care. HMO plans generally cover a range of vaccines, from those for common childhood illnesses like measles and polio to adult vaccines such as the flu shot and shingles vaccine. Some plans may also cover travel vaccines if deemed medically necessary. It's important to check with your specific HMO provider for a list of covered vaccines, as this can vary by plan.

Screenings for various health conditions are also typically included in preventive care coverage. These might encompass mammograms for breast cancer, colonoscopies for colorectal cancer, and bone density tests for osteoporosis, among others. The frequency and age at which these screenings are recommended can depend on individual risk factors and general health guidelines. For example, women are generally advised to start mammograms at age 40, while men may begin colorectal cancer screenings at age 50.

One of the key benefits of HMO plans is their emphasis on coordinated care. This means that your primary care physician will work with you to develop a personalized preventive care plan, taking into account your medical history, lifestyle, and any existing health conditions. This coordinated approach can help ensure that you receive the most appropriate and effective preventive care services.

It's also worth noting that preventive care services are often provided at no additional cost to the insured individual. This is because the goal of these services is to prevent more costly and serious health issues down the line. By investing in preventive care, both patients and insurance providers can potentially save money and improve health outcomes in the long run.

In summary, preventive care coverage under HMO health insurance plans is designed to support proactive health management. By providing access to routine check-ups, vaccinations, and screenings, these plans help individuals stay healthy and detect potential health issues early, when they are most treatable.

Adding a Boyfriend to Your Medical Insurance: Is It Possible?

You may want to see also

Explore related products

![Health Insurance Benefits Advisory Council annual report on Medicare covering the period ... Volume 1966-1967 1967 [Leather Bound]](https://m.media-amazon.com/images/I/61IX47b4r9L._AC_UY218_.jpg)

![]()

Primary Care: Visits to general practitioners, family doctors, and pediatricians for non-specialized medical care

Under an HMO health insurance plan, primary care visits to general practitioners, family doctors, and pediatricians for non-specialized medical care are typically covered with minimal out-of-pocket costs. These visits serve as the foundation for maintaining overall health and preventing more serious medical conditions.

One unique aspect of HMO plans is the emphasis on coordinated care. When you visit a primary care physician within your HMO network, they will often serve as your main point of contact for all health-related concerns. This doctor can refer you to specialists, order tests, and prescribe medications, all while ensuring that your care is managed efficiently and effectively.

It's important to note that HMO plans usually require you to choose a primary care physician (PCP) from within the network. This PCP will be responsible for providing you with routine check-ups, preventive care, and managing any chronic conditions you may have. If you need to see a specialist, your PCP will typically need to provide a referral.

In terms of cost, HMO plans often have lower premiums and out-of-pocket costs compared to other types of health insurance plans. However, this can vary depending on the specific plan and your location. It's always a good idea to review the details of your plan to understand what is covered and what your financial responsibilities may be.

Remember, preventive care is a key component of primary care visits. Regular check-ups, vaccinations, and screenings can help catch potential health issues early on, when they are often easier and less expensive to treat. By taking advantage of these preventive care services, you can not only improve your overall health but also potentially save money on medical costs in the long run.

Medical Insurance: Job Loss and Coverage Options

You may want to see also

Explore related products

![]()

Specialist Care: Referrals to specialists for specific medical conditions or treatments

Under an HMO health insurance plan, specialist care is typically covered, but with certain stipulations. One of the key aspects of HMO plans is that they often require a referral from a primary care physician (PCP) before you can see a specialist. This means that if you have a specific medical condition or need a particular treatment, you'll likely need to discuss it with your PCP first. They will then determine if a referral to a specialist is necessary and, if so, facilitate that process.

The referral process can vary depending on the specific HMO plan and the healthcare provider network. Some plans may have a more streamlined process, allowing for quick referrals, while others may have more stringent requirements. It's important to understand your plan's specific procedures to ensure you receive the care you need in a timely manner.

Specialist care can encompass a wide range of medical services, from consultations with cardiologists or oncologists to treatments like physical therapy or occupational therapy. HMO plans generally cover these services, but the extent of coverage and any associated costs (such as copays or coinsurance) can differ. It's crucial to review your plan's benefits and limitations to understand what is covered and what you may be responsible for financially.

In some cases, HMO plans may also require pre-authorization for certain specialist services or treatments. This means that before you can receive the care, the insurance company must approve it. This can be an additional step in the process, but it's designed to ensure that the care is medically necessary and appropriate.

When navigating specialist care under an HMO plan, it's essential to be proactive and informed. Understand your plan's requirements, work closely with your PCP, and don't hesitate to ask questions or seek clarification if needed. By doing so, you can help ensure that you receive the specialist care you need while minimizing any potential delays or financial surprises.

Discover Maxwell the Pig's Insurance Company: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Hospital Services: Inpatient and outpatient services, including surgeries, lab tests, and imaging

Under an HMO health insurance plan, hospital services are typically covered with certain stipulations. Inpatient services, which include overnight stays, are generally covered when deemed medically necessary by the plan's guidelines. This can encompass a wide range of scenarios from surgeries to intensive care. However, the specifics of what is covered can vary greatly depending on the individual policy, including the length of stay, the type of room, and any additional services provided during the hospitalization.

Outpatient services, such as lab tests and imaging, are also commonly covered under HMO plans. These services are usually utilized to diagnose or monitor medical conditions and can include everything from routine blood work to advanced imaging techniques like MRI or CT scans. As with inpatient services, the extent of coverage can differ based on the policy, and some plans may require prior authorization or referrals from a primary care physician.

One unique aspect of HMO coverage for hospital services is the emphasis on cost-effectiveness and quality of care. HMO plans often have negotiated rates with healthcare providers, which can result in lower out-of-pocket costs for members. Additionally, these plans may focus on evidence-based medicine and preventive care to reduce the overall need for hospital services.

When considering HMO health insurance, it's important to carefully review the plan's details regarding hospital services. This includes understanding the coverage for both inpatient and outpatient services, any limitations or exclusions, and the process for obtaining necessary care. By doing so, individuals can make informed decisions about their healthcare and ensure they have the appropriate coverage for their needs.

Congressional Health Coverage: Understanding the Benefits and Plans Available

You may want to see also

Explore related products

![]()

Prescription Drugs: Coverage for medications prescribed by healthcare providers

Under an HMO (Health Maintenance Organization) plan, prescription drug coverage is a crucial aspect that can significantly impact your healthcare experience. Unlike some other types of health insurance, HMOs typically require you to use a specific network of pharmacies and healthcare providers. This means that your prescription drug coverage may be limited to certain medications and pharmacies within the HMO's network. It's essential to understand what medications are covered under your HMO plan and how to access them to ensure you receive the care you need.

One unique aspect of HMO prescription drug coverage is the potential for tiered formularies. A tiered formulary is a system where medications are categorized into different tiers based on their cost and effectiveness. Medications in lower tiers are usually more affordable, while those in higher tiers may require higher copays or coinsurance. This system encourages the use of more cost-effective medications, which can help keep overall healthcare costs down. However, it also means that you may need to work with your healthcare provider to find a medication that is both effective and affordable under your plan.

Another important consideration with HMO prescription drug coverage is the possibility of prior authorization requirements. Prior authorization is a process where your healthcare provider must obtain approval from the insurance company before prescribing a certain medication. This is often required for more expensive or specialized medications. Understanding the prior authorization process and working closely with your healthcare provider can help ensure that you receive the medications you need in a timely manner.

When it comes to accessing prescription medications under an HMO plan, it's also important to be aware of any restrictions or limitations. For example, some HMO plans may have quantity limits on certain medications, meaning you can only receive a certain amount at a time. Others may require you to use mail-order pharmacies for certain medications, which can impact how quickly you receive your prescriptions. Being aware of these potential restrictions can help you plan ahead and avoid any disruptions in your medication regimen.

In summary, while HMO prescription drug coverage can provide access to necessary medications, it's important to understand the specific details of your plan, including any tiered formularies, prior authorization requirements, and restrictions on accessing medications. By working closely with your healthcare provider and being proactive in managing your prescription drug coverage, you can ensure that you receive the care you need while also navigating the complexities of your HMO plan.

The Importance of Infant Medical Insurance Coverage

You may want to see also

Frequently asked questions

An HMO (Health Maintenance Organization) health insurance plan is a type of managed care plan that provides health coverage to its members through a network of healthcare providers. Members are typically required to choose a primary care physician (PCP) who coordinates their care and refers them to specialists within the network when necessary.

HMO health insurance plans typically cover a wide range of healthcare services, including preventive care, doctor visits, hospital stays, emergency care, prescription drugs, and mental health services. However, the specific coverage and benefits may vary depending on the plan and the insurance provider.

Yes, HMO health insurance plans often have limitations and restrictions. For example, members may be required to use healthcare providers within the plan's network, and referrals from the PCP may be necessary to see specialists. Additionally, some plans may have deductibles, copayments, or coinsurance requirements for certain services. It's important to review the plan's details carefully to understand any limitations or restrictions that may apply.