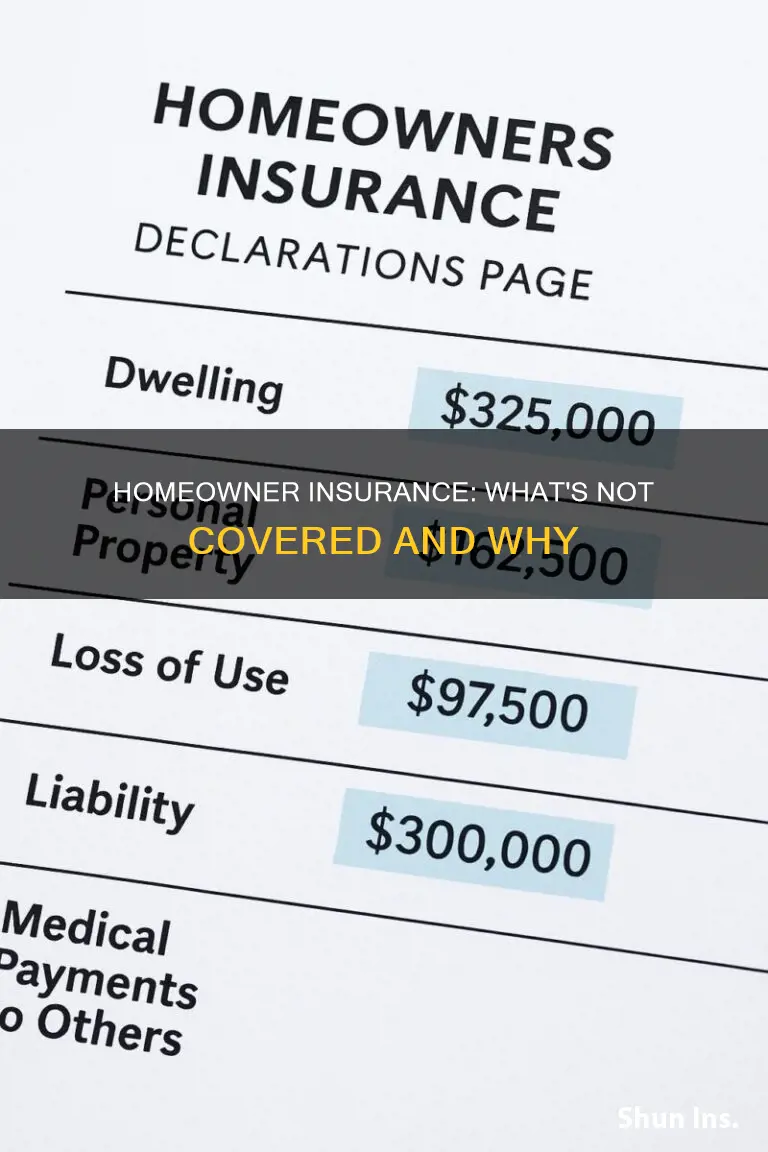

Homeowner's insurance is designed to protect you financially from damage and losses to your home by a covered event. However, it's important to note that not all insurance policies are the same, and there are certain exclusions and limitations to coverage that you should be aware of. Understanding what is not covered by your homeowner's insurance policy is crucial to ensure you have the necessary protection in place.

| Characteristics | Values |

|---|---|

| Basic maintenance and wear and tear | Not covered |

| Damage caused by insects and rodents | Not covered |

| Damage caused by natural disasters (earthquakes, landslides, floods) | Not covered, but can be covered under a separate policy |

| Damage caused by war or nuclear accidents | Not covered |

| Damage caused by government entities | Not covered |

| Home-based businesses | Not covered |

| Jewelry and other high-value items | Covered up to a certain amount, additional coverage may be required |

| Wind damage | Not covered in high-risk areas |

Explore related products

$15.75

What You'll Learn

- Home insurance does not cover damages caused by insects, rodents, or other vermin

- It also doesn't cover damage from natural disasters like earthquakes, landslides, or floods

- Home insurance typically doesn't cover the cost of basic maintenance and wear and tear

- It does not cover damage caused by governmental entities or acts of public authorities

- Home-based businesses are usually not covered by standard homeowner's insurance policies

![]()

Home insurance does not cover damages caused by insects, rodents, or other vermin

Home insurance is designed to protect you financially from damages and losses to your home by a covered event. However, it's important to note that not all types of damage are covered by standard home insurance policies. One notable exclusion is damage caused by insects, rodents, or other vermin.

Insect infestations, such as termites, bees, or wood-boring insects, are typically not covered by home insurance. Insurers often view these infestations as a maintenance issue, making it the homeowner's responsibility to address and prevent. While termites may cause extensive damage to a home, it is often specifically excluded from coverage. Similarly, damage caused by rodents, such as rats, mice, squirrels, or chipmunks, is generally not covered. If the infestation was preventable or the homeowner was aware of the issue and did not take measures to address it, the insurer may deny coverage, deeming it a "lack of maintenance".

It's important to understand the concept of "sudden and accidental" when it comes to damage caused by insects or rodents. Home insurance is not intended to cover gradual damage that occurs over time. A lightning strike, for example, would be covered as it is sudden and accidental. In contrast, an insect infestation or rodent problem typically takes time to cause significant damage, and there are usually signs that allow for early intervention before extensive damage occurs.

In some rare cases, there may be partial coverage for damage caused by insects or rodents. For instance, if there is a collapse in your home due to hidden damage from termites, your insurer might cover the cost of repairing the collapse, excluding the termite-damaged beam. Even in this scenario, the termite damage would need to be unseen for coverage to apply. Visible termite damage is unlikely to be covered by home insurance.

To protect your home from insects, rodents, and other vermin, it's essential to take preventive measures. Regularly inspect your house, roof, and attic for any holes or entry points that can be patched or sealed. Remove food sources that may attract pests and store trash in lockable bins. By taking proactive steps, you can help prevent infestations and reduce the risk of damage to your home.

Tower Hill Insurance: Is It Worth the Premium?

You may want to see also

Explore related products

![]()

It also doesn't cover damage from natural disasters like earthquakes, landslides, or floods

Homeowner's insurance is designed to protect you financially from damages and losses to your home by a covered event. While it typically covers a broad range of possible damages, it's important to understand that not all policies are the same, and there may be gaps in your coverage.

One significant exclusion from standard homeowner's insurance policies is damage from natural disasters like earthquakes, landslides, and floods. These events are not typically covered due to their unique risks and potential for extensive damage. For example, earthquakes are a specific type of natural disaster that can cause widespread destruction and are often excluded from basic policies. If you live in an area prone to earthquakes, you may need to purchase separate earthquake insurance or an endorsement to ensure you're protected.

Similarly, if your home is located in an area susceptible to landslides, it's crucial to review your policy carefully. Landslides can result from various factors, including heavy rainfall, earthquakes, or unstable slopes, and their impact can be devastating. Standard homeowner's insurance policies typically do not include landslide coverage, and you may need to purchase additional protection.

Flooding is another natural disaster that is generally not covered by basic homeowner's insurance policies. Flood coverage is typically provided by specialised insurance or government agencies like the Federal Emergency Management Agency (FEMA). If your home is at risk of flooding due to its location or environmental factors, it's essential to consider flood insurance to protect your property.

It's worth noting that while these natural disasters may not be covered by standard policies, separate coverage options are usually available. These can include purchasing additional insurance policies or endorsements specifically for earthquakes, landslides, or floods. It's important to consult with your insurance provider to understand your specific coverage and any exclusions or limitations that may apply.

Credit Reporting Act: Insurance and Fairness

You may want to see also

Explore related products

![]()

Home insurance typically doesn't cover the cost of basic maintenance and wear and tear

Home insurance is designed to provide financial protection against unexpected events and accidents. However, it is important to understand that home insurance does not cover the cost of basic maintenance and wear and tear. This means that homeowners are responsible for covering the costs of routine repairs and replacements that are required due to the normal ageing and use of their property.

Basic maintenance refers to the regular upkeep and care needed to keep a home in good condition. This includes tasks such as fixing leaky pipes, patching holes in walls or roofs, and maintaining appliances. These are considered the homeowner's responsibility and are not typically covered by insurance. For example, if your air conditioning unit breaks down due to normal wear and tear, you will need to pay for the repairs or replacement yourself.

Wear and tear refers to the gradual deterioration or depreciation of a property or its contents over time due to regular use. This can include issues such as a leaking roof, rotting fence, chipping paint, or mechanical problems with appliances. These are considered normal aspects of homeownership and are generally not covered by home insurance. In the case of an older roof that develops a leak, insurance companies may attribute this to the roof reaching the end of its lifespan and deny coverage.

Home insurance is intended to cover sudden and unexpected events, often referred to as "acts of God," such as natural disasters or accidents. For example, if a hailstorm damages your roof, insurance should cover the repairs. However, if the roof is old and develops a leak due to age and wear, it is unlikely to be covered. Similarly, if a pipe breaks and leaks for several months, causing damage to your floors, the insurance company may deny coverage if they believe the damage resulted from neglect or a lack of timely maintenance.

It is important for homeowners to be proactive in maintaining their property and addressing issues promptly. Regular maintenance can help prevent minor issues from becoming major problems and reduce the risk of insurance claims being denied due to neglect or wear and tear. By understanding what is not covered by home insurance, homeowners can make informed decisions about their property's upkeep and financial planning.

Homeowners Insurance: Foundation Sinking Covered?

You may want to see also

Explore related products

![]()

It does not cover damage caused by governmental entities or acts of public authorities

Homeowner's insurance is designed to cover accidents and events beyond the control of the homeowner. However, it does not cover damage caused by governmental entities or acts of public authorities. This includes financial damages due to acts by the US government, acts of war, or nuclear accidents. Government acts could include your property being claimed for eminent domain to build public works projects. Federal law prohibits insurance companies from covering nuclear accidents, but the nuclear power plant in question must pay for all the damages.

Terrorist attacks are not considered acts of war and are often covered by homeowner's insurance. Homeowner's insurance also does not cover damages caused by natural disasters, such as earthquakes, floods, or sinkholes. If you live in an area prone to these types of disasters, you may need to purchase separate insurance or an endorsement to ensure you are protected. For example, flood coverage is generally provided by the Federal Emergency Management Agency (FEMA).

Homeowner's insurance also typically does not cover damage caused by insects, rodents, or animals. This includes damages caused by termites, bees, rats, mice, or bats. Additionally, homeowner's insurance does not cover damages caused by negligence or normal wear and tear. For example, if you do not trim a tree on your property and a falling limb damages your house, your insurance will not cover the repairs.

It is important to note that homeowner's insurance policies can vary, so it is essential to read the fine print before purchasing a policy to understand what is and is not covered.

Eve Insurance: Worth the Cost?

You may want to see also

Explore related products

![]()

Home-based businesses are usually not covered by standard homeowner's insurance policies

Homeowner's insurance is designed to protect your home financially from damage and loss caused by a covered event. It covers the physical structure of your home, personal belongings, and liability protection in case someone is injured on your property. However, it is important to note that homeowner's insurance does not cover home-based businesses.

Home-based businesses are typically not covered by standard homeowners insurance policies. This means that if you run a business from your home, you may not have the necessary protection in place. While some insurance companies may offer limited coverage for business equipment and property, it is usually insufficient for a home-based business. For example, a standard homeowner's policy may only cover up to $2,500 in business equipment, which may not be enough to protect all your business assets.

Additionally, homeowner's insurance does not typically cover liability claims related to your home-based business. This includes personal injury lawsuits, libel, slander, and other legal actions that may arise from your business operations. Without proper coverage, you could be left financially vulnerable in the event of a claim or lawsuit.

To ensure adequate protection for your home-based business, it is recommended to purchase separate business insurance. This type of insurance can provide coverage for business property, equipment, inventory, and other physical assets. It also typically includes liability protection, which can cover you in the event of a lawsuit or claim related to your business activities.

Depending on the nature and size of your home-based business, you may have several options for insurance coverage. You can choose to add an endorsement or rider to your existing homeowner's policy to increase the limits of your business property coverage. Alternatively, you can consider a business owner's policy (BOP), which is designed specifically for small- to mid-sized businesses operating in multiple locations. A BOP provides broader coverage for business property, equipment, loss of income, extra expenses, and liability.

HomeAway Insurance: Is Damage Coverage Worth the Cost?

You may want to see also

Frequently asked questions

Natural disasters like earthquakes are generally excluded from standard home insurance policies. If you live in an area prone to these disasters, you may need to purchase separate insurance.

No, homeowner's insurance does not cover basic maintenance and wear and tear. For example, if your AC breaks down or you need to replace worn-out flooring, you will have to pay for the repairs yourself.

No, damages caused by insects like termites and bees or rodents like rats and mice are typically excluded from home insurance policies. It is the homeowner's responsibility to maintain their property and prevent infestations.

While homeowner's insurance does cover personal belongings, there may be limits on certain high-value items such as jewellery, artwork, collectibles, tools, musical instruments, and firearms. You may need to purchase additional coverage for these items.