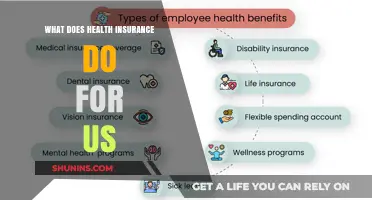

HSP stands for Health Spending Plan in the context of health insurance. It is a type of health insurance plan that allows policyholders to pay for medical expenses using pre-tax dollars. This can include deductibles, copays, and coinsurance. HSPs are often used in conjunction with high-deductible health plans (HDHPs) to help individuals save money on their healthcare costs. By using pre-tax dollars, policyholders can reduce their taxable income, which can lead to lower tax liabilities. HSPs are typically offered by employers as a benefit to their employees, but they can also be purchased individually. It's important to note that HSPs have certain eligibility requirements and contribution limits, so it's essential to understand the specifics of the plan before enrolling.

| Characteristics | Values |

|---|---|

| Definition | HSP stands for Health Service Provider |

| Role | Entity that provides healthcare services to patients |

| Examples | Hospitals, clinics, laboratories, pharmacies |

| Responsibility | Delivering medical care, treatments, and services |

| Accreditation | Often required to be accredited by regulatory bodies |

| Billing | May handle billing and insurance claims |

| Network | Can be part of a larger network of healthcare providers |

| Referrals | May receive referrals from primary care physicians |

| Specialties | Can specialize in specific areas of healthcare |

| Patient Interaction | Direct interaction with patients for service delivery |

Explore related products

What You'll Learn

- HSP Meaning: Health Spending Plan, a type of health insurance plan

- HSP Benefits: Covers medical expenses, often with lower premiums and higher deductibles

- HSP Eligibility: Available to individuals and families, sometimes with income limits

- HSP Providers: Network of healthcare providers offering services at reduced rates

- HSP Enrollment: Process of signing up for an HSP, often through an employer or marketplace

![]()

HSP Meaning: Health Spending Plan, a type of health insurance plan

A Health Spending Plan (HSP) is a type of health insurance plan that allows individuals to set aside a portion of their income for medical expenses. This plan is designed to help people save money on healthcare costs by providing a tax-advantaged way to pay for qualified medical expenses. HSPs are typically offered by employers as a benefit to their employees, but they can also be purchased individually.

One of the key features of an HSP is that it allows individuals to save money on a pre-tax basis. This means that the money contributed to the plan is deducted from the individual's taxable income, reducing their overall tax liability. The funds in the HSP can then be used to pay for a wide range of medical expenses, including doctor visits, hospital stays, prescription medications, and more.

Another important aspect of HSPs is that they are designed to be flexible and customizable. Individuals can choose how much money they want to contribute to the plan each year, and they can also decide how to use the funds. Some HSPs offer a debit card that can be used to pay for medical expenses directly, while others require individuals to submit receipts for reimbursement.

It's also worth noting that HSPs are not the same as Health Savings Accounts (HSAs) or Flexible Spending Accounts (FSAs). While all three types of plans offer a way to save money on healthcare costs, they have different rules and regulations. For example, HSPs are only available to individuals who are enrolled in a high-deductible health plan (HDHP), while HSAs and FSAs are available to a wider range of people.

In conclusion, a Health Spending Plan is a valuable tool for individuals who want to save money on healthcare costs. By allowing people to set aside a portion of their income for medical expenses on a pre-tax basis, HSPs can help make healthcare more affordable and accessible.

Is Vision Insurance Part of Health Coverage? Key Facts Explained

You may want to see also

Explore related products

![]()

HSP Benefits: Covers medical expenses, often with lower premiums and higher deductibles

Health Savings Plans (HSPs) offer a unique advantage in the realm of health insurance by providing a financial incentive for policyholders to manage their healthcare costs effectively. One of the primary benefits of HSPs is their ability to cover medical expenses, often with lower premiums compared to traditional health insurance plans. This cost-saving aspect is particularly appealing to individuals and families looking to reduce their overall healthcare expenditures.

In addition to lower premiums, HSPs typically feature higher deductibles, which means that policyholders are responsible for a larger portion of their medical costs before the insurance coverage kicks in. While this may seem like a drawback, it actually encourages individuals to be more mindful of their healthcare spending and to seek out cost-effective treatment options. By promoting consumerism in healthcare, HSPs can help drive down overall medical costs and improve the efficiency of the healthcare system.

Furthermore, HSPs often come with tax advantages, as contributions to the plan are usually tax-deductible. This can result in significant savings for policyholders, especially those in higher tax brackets. Additionally, the funds in an HSP can be rolled over from year to year, allowing individuals to build up a reserve of funds for future medical expenses. This flexibility can be particularly beneficial for those with unpredictable healthcare needs or for those looking to save for long-term care.

Another key benefit of HSPs is their portability. Unlike some other types of health insurance plans, HSPs are not tied to a specific employer or job, which means that policyholders can take their plan with them if they change jobs or become self-employed. This portability can provide a sense of security and continuity in an individual's healthcare coverage, even during times of transition.

In conclusion, Health Savings Plans offer a range of benefits that can help individuals and families manage their healthcare costs more effectively. By providing lower premiums, higher deductibles, tax advantages, and portability, HSPs promote consumerism in healthcare and offer a flexible, cost-saving alternative to traditional health insurance plans.

Boots Glasses Insurance: Is It Covered by Medical Insurance?

You may want to see also

Explore related products

![]()

HSP Eligibility: Available to individuals and families, sometimes with income limits

Health Savings Plans (HSPs) are a type of health insurance plan that allows individuals and families to save money on a tax-advantaged basis for qualified medical expenses. One of the key aspects of HSP eligibility is that it is available to individuals and families, sometimes with income limits. This means that not everyone may qualify for an HSP, and understanding the eligibility requirements is crucial for those who are considering this type of health insurance plan.

To be eligible for an HSP, individuals must first have a high-deductible health plan (HDHP) and not be enrolled in Medicare. Additionally, they cannot be claimed as a dependent on someone else's tax return. For families, the eligibility requirements are similar, but the HDHP must cover all family members. Income limits may also apply, depending on the specific HSP provider and the state in which the individual or family resides.

It's important to note that HSPs are designed to help individuals and families save money on healthcare costs, but they are not suitable for everyone. Those who have frequent medical expenses or require ongoing treatment may find that an HSP is not the best option for them. On the other hand, individuals and families who have relatively few medical expenses and want to save money on healthcare costs may find that an HSP is a good fit.

When considering an HSP, it's essential to carefully review the eligibility requirements and understand how the plan works. This includes understanding the contribution limits, withdrawal rules, and any potential penalties for non-qualified withdrawals. By doing so, individuals and families can make an informed decision about whether an HSP is right for them.

In conclusion, HSP eligibility is available to individuals and families, sometimes with income limits. Understanding the specific requirements and how the plan works is crucial for making an informed decision about whether an HSP is the right choice for healthcare savings.

Affordable Family Medical Insurance: Cost for a Trio

You may want to see also

Explore related products

![]()

HSP Providers: Network of healthcare providers offering services at reduced rates

HSP providers form a crucial network within the healthcare system, offering services at reduced rates to ensure accessibility and affordability for a broader population. These providers are integral to the functioning of Health Spending Plans (HSPs), which are designed to help individuals and families manage their healthcare expenses more effectively. By partnering with HSPs, healthcare providers can offer their services at lower costs, making quality healthcare more attainable for those who might otherwise struggle to afford it.

One of the key benefits of HSP providers is their ability to offer a wide range of services, from primary care to specialized treatments, all at reduced rates. This network includes doctors, hospitals, clinics, and other healthcare facilities that have agreed to provide services at discounted prices to HSP members. This not only helps individuals save money on their healthcare costs but also encourages providers to streamline their operations and reduce overhead expenses, leading to a more efficient healthcare system overall.

To take advantage of the reduced rates offered by HSP providers, individuals typically need to enroll in an HSP program. This often involves paying a monthly or annual fee, which grants access to the network of providers and their discounted services. Once enrolled, members can choose from a variety of providers within the network and receive the agreed-upon reduced rates for their healthcare services. This can lead to significant savings, especially for those with chronic conditions or who require frequent medical attention.

In addition to offering reduced rates, HSP providers also play a role in promoting preventive care and wellness. By making healthcare more affordable, HSPs encourage individuals to seek regular check-ups, screenings, and other preventive services that can help detect and manage health issues before they become more serious and costly to treat. This focus on preventive care not only improves health outcomes but also helps to reduce the overall burden on the healthcare system.

Overall, HSP providers are a vital component of the healthcare landscape, offering a practical solution to the challenge of rising healthcare costs. By providing services at reduced rates, these providers help to ensure that quality healthcare remains accessible and affordable for a wide range of individuals and families.

Securing Proof of Health Insurance: A Step-by-Step Guide for Policyholders

You may want to see also

Explore related products

$10.21 $18.95

![]()

HSP Enrollment: Process of signing up for an HSP, often through an employer or marketplace

Enrolling in an HSP, or Health Savings Plan, is a process that typically involves signing up through an employer or a health insurance marketplace. This enrollment process is a crucial step for individuals looking to take advantage of the tax benefits and savings opportunities that HSPs offer. To begin the enrollment process, individuals should first check with their employer to see if an HSP is available as part of their employee benefits package. If an HSP is offered, the employer will usually provide detailed information about the plan, including eligibility requirements, contribution limits, and any associated fees.

If an individual's employer does not offer an HSP, or if they are self-employed, they may be able to enroll in an HSP through a health insurance marketplace. In this case, the individual will need to research and compare different HSP options to find the one that best meets their needs. Factors to consider when choosing an HSP include the plan's contribution limits, investment options, and any associated fees or penalties.

Once an individual has chosen an HSP, the enrollment process typically involves filling out an application form and providing any required documentation, such as proof of employment or income. The individual will also need to decide how much they want to contribute to the HSP each year, up to the maximum allowed limit. It's important to note that contributions to an HSP are usually made on a pre-tax basis, which can help reduce an individual's taxable income and lower their overall tax liability.

After enrolling in an HSP, individuals will need to monitor and manage their account to ensure they are making the most of their savings opportunities. This may involve tracking their contributions, monitoring their account balance, and making investment decisions to grow their savings over time. By taking advantage of an HSP, individuals can set aside money for future healthcare expenses while also enjoying the benefits of tax-advantaged savings.

Do Electrical Contractors Have Health Insurance? Exploring Coverage Options

You may want to see also

Frequently asked questions

HSP stands for Health Spending Plan, which is a type of health insurance plan that allows policyholders to pay for medical expenses using pre-tax dollars.

An HSP works by allowing policyholders to set aside a certain amount of money from their income, which is then used to pay for qualified medical expenses. This money is typically deducted from the policyholder's paycheck on a pre-tax basis, which can help reduce their taxable income.

The benefits of an HSP include tax savings, as the money set aside for medical expenses is not subject to federal or state income taxes. Additionally, HSPs can help policyholders save money on out-of-pocket medical expenses, as they can use the funds in their HSP to pay for these costs.

One drawback of an HSP is that the funds must be used for qualified medical expenses, or else they may be subject to taxes and penalties. Additionally, HSPs may not be available to everyone, as they are typically offered through employers or other organizations.

An HSP is similar to a Health Savings Account (HSA) in that both allow policyholders to set aside pre-tax dollars for medical expenses. However, HSAs are typically only available to individuals who have a high-deductible health plan (HDHP), while HSPs may be available to a wider range of individuals. Additionally, HSAs can earn interest over time, while HSPs typically do not.