Mortgage insurance is an insurance policy that protects the lender or investor in the event that the borrower defaults on their mortgage. It is typically required when the borrower's down payment is less than 20% of the purchase price of the home, as this is considered a riskier investment for the lender. The cost of mortgage insurance is included in the borrower's monthly payments and can increase the overall cost of the loan. Mortgage insurance can help borrowers qualify for a loan that they may not have been able to without insurance, and it can also provide peace of mind in the event of financial hardship. However, it is important to note that mortgage insurance protects the lender and not the borrower. There are different types of mortgage insurance, including private mortgage insurance (PMI), qualified mortgage insurance premium (MIP) insurance, and mortgage title insurance, and it can be mandatory or optional depending on the situation.

| Characteristics | Values |

|---|---|

| Who does it protect? | The lender, not the borrower |

| Who provides it? | Private insurance companies |

| Who pays for it? | The borrower |

| When is it required? | When the down payment is less than 20% of the purchase price of the home |

| Can it be avoided? | Yes, by making a down payment of 20% or more |

| Can it be cancelled? | Yes, once the loan balance equals 80% or less of the original value of the home |

| Types | Private mortgage insurance (PMI), qualified mortgage insurance premium (MIP), mortgage title insurance, mortgage life insurance |

| Pros | Helps people with below-average credit scores or smaller down payments to qualify for a loan |

| Cons | Can be costly and time-consuming; may be difficult to cancel |

Explore related products

$15.95

What You'll Learn

![]()

Mortgage insurance types: private, qualified premium, and title insurance

Insuring a mortgage means paying an additional fee to insure the loan amount in the event that you fall behind on payments. This insurance protects the lender, not the borrower, and is usually required when the down payment is less than 20% of the purchase price. There are several types of mortgage insurance, each with its own unique features and benefits. Here is an overview of three common types: private mortgage insurance, qualified mortgage insurance (also known as Federal Housing Administration (FHA) insurance), and title insurance.

Private mortgage insurance (PMI) is a type of insurance that a borrower may be required to purchase when taking out a conventional loan with a down payment of less than 20% of the property's purchase price. PMI protects the lender in the event that the borrower stops making loan payments and can help the borrower qualify for a loan they might not otherwise obtain. However, it is important to note that PMI does not protect the borrower, and they can still lose their home through foreclosure if they fall behind on payments. PMI can increase the overall cost of the loan, and borrowers should carefully consider their options and compare total costs before deciding.

Qualified mortgage insurance, also known as Federal Housing Administration (FHA) insurance, is required for all FHA loans. Unlike PMI, the cost of FHA insurance is the same regardless of the borrower's credit score, with only a slight increase for down payments less than 5%. FHA insurance includes an upfront cost paid during closing and a monthly cost included in the monthly payment. Similar to PMI, FHA insurance protects the lender and increases the overall cost of the loan. Borrowers who cannot afford the upfront fee can roll it into their mortgage, but this will further increase the loan amount and overall costs.

Farmers Earthquake Insurance: Worth the Cost?

You may want to see also

Explore related products

![]()

Mortgage insurance vs. mortgage life insurance

Insuring a mortgage means protecting yourself and your loved ones financially in the event that you can no longer pay off your mortgage. This can be due to death, injury, illness, unemployment, or other circumstances that affect your ability to work.

There are several types of insurance that can help in such situations, including mortgage protection insurance (MPI), mortgage life insurance, and private mortgage insurance (PMI). Let's focus on the differences between mortgage protection insurance and mortgage life insurance:

Mortgage Protection Insurance (MPI)

Mortgage protection insurance, also known as mortgage payment protection insurance, is a type of life insurance that pays off the remaining balance of your mortgage when you die. The payout goes directly to the lender to cover the mortgage debt. This type of insurance is ideal for individuals who cannot medically qualify for other life insurance policies. MPI does not require a medical exam for qualification, and it aligns with your loan balance. However, one of the drawbacks of MPI is its lack of flexibility. The payout goes directly to the lender, so your family doesn't have the freedom to spend the money as they see fit. Additionally, the death benefit from an MPI policy typically decreases over time as you pay off your mortgage, while your premiums remain the same.

Mortgage Life Insurance

Mortgage life insurance is a type of decreasing life insurance designed to protect a repayment mortgage that reduces over time. The cover amount decreases over the length of the policy, which means that the potential payout to cover the repayment mortgage reduces as well. This type of insurance is typically sold by mortgage lenders, and they are the ones who receive the payout if the policyholder dies. Mortgage life insurance may not be suitable for those who want financial protection that doesn't lessen over time. It is important to note that mortgage life insurance is not a savings or investment product and has no cash value unless a valid claim is made.

Choosing Between MPI and Mortgage Life Insurance

The choice between MPI and mortgage life insurance depends on your financial goals, health, and ability to qualify for coverage. If you are in good health and can qualify for competitively priced term or permanent life insurance, the latter may offer better value for broader coverage. Life insurance provides a lump sum payout that can be used to pay off the mortgage or cover other financial needs, giving your beneficiaries more flexibility. Additionally, if you want to leave behind more than just mortgage protection, life insurance may be a more suitable option.

Mortgage Insurance: Is It Worth the Cost?

You may want to see also

Explore related products

![]()

When is mortgage insurance required?

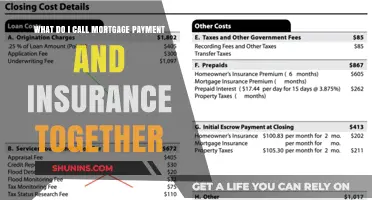

Mortgage insurance is typically required when a borrower makes a down payment of less than 20% of the purchase price of the home. In this case, the lender may require the borrower to purchase private mortgage insurance (PMI) to protect them in the event of default on the loan. The cost of PMI can vary depending on factors such as the size of the loan, credit score, and down payment amount. Borrowers can use a PMI calculator to estimate these costs.

Additionally, certain types of loans, such as Federal Housing Administration (FHA) loans, require ongoing mortgage insurance payments, even if the borrower reaches 20% equity. FHA mortgage insurance includes an upfront cost, paid as part of the closing costs, and a monthly cost included in the monthly payment. Similar to FHA loans, loans from the US Department of Agriculture (USDA) also typically require mortgage insurance.

In some countries, mortgage insurance is mandatory for certain types of properties or loans. For example, in Australia, borrowers must pay Lenders Mortgage Insurance (LMI) for home loans over 80% of the purchase price. In Singapore, owners of HDB flats using their Central Provident Fund (CPF) accounts to pay their monthly mortgage instalments are required to have mortgage insurance, whereas it is not mandatory for owners of private homes.

It is important to note that mortgage insurance should not be confused with mortgage life insurance, which protects heirs if the borrower dies while still owing mortgage payments.

XCover Insurance: Worth the Cost?

You may want to see also

Explore related products

![NMLS Study Guide 2024-2025: 5 Full-Length MLO Practice Exams, SAFE Mortgage Loan Originator Test Prep Secrets Book with Detailed Answer Explanations: [3rd Edition]](https://m.media-amazon.com/images/I/61zi0BJms+L._AC_UL320_.jpg)

![]()

Pros and cons of mortgage insurance

Mortgage insurance is an insurance policy that protects lenders or investors in mortgage-backed securities in the event of the borrower defaulting on payments, passing away, or being unable to meet the contractual obligations of the mortgage. It is also known as mortgage guarantee and home-loan insurance.

There are three types of mortgage insurance: private mortgage insurance (PMI), qualified mortgage insurance premium (MIP) insurance, and mortgage title insurance. Mortgage insurance is typically required when the down payment is less than 20% of the purchase price of the home.

Pros:

- Mortgage insurance allows borrowers to qualify for a loan that they might not otherwise be able to get. It lowers the risk to the lender, making them more likely to approve the loan.

- It can help buyers get into the housing market earlier than they would have otherwise. This is especially beneficial for those with steady incomes, as they are perceived as lower-risk borrowers and may receive lower insurance premiums.

- Mortgage insurance has a high acceptance rate, even for those with health concerns or riskier jobs that may make life insurance more difficult to obtain. It provides peace of mind for those with tight budgets or health issues.

- In the event of the borrower's death, mortgage insurance can protect family members from mortgage default. It takes the guesswork out of how much is still owed, ensuring that the remaining mortgage balance is covered without the need for loved ones to crunch numbers during a stressful time.

- Borrowers may be able to cancel their mortgage insurance once they have paid off a certain portion of their loan, such as when the loan balance reaches 78% or 80% of the original home's value.

Cons:

- Mortgage insurance increases the overall cost of the loan. It is an additional expense that protects the lender, not the borrower.

- If the borrower falls behind on payments, their credit score could suffer, and they could lose their home through foreclosure.

- In some cases, the borrower may be able to avoid paying for mortgage insurance by making a larger down payment (typically 20% or more) or choosing a different type of loan.

- There may be alternative options, such as a "piggyback" second mortgage, which may be marketed as a cheaper alternative to mortgage insurance. However, it is important to compare the total cost before making a decision, as these alternatives may not always be cheaper.

Farmers Insurance: Uncovering the Headquarters and its Address

You may want to see also

Explore related products

![]()

Cancelling mortgage insurance

Mortgage insurance is an insurance policy that protects the lender or investor in mortgage-backed securities in the event of a borrower defaulting on their payments. It is not a requirement for all mortgages, but if you are unable to make a down payment of at least 20% of the purchase price of the home, you will likely need to pay for mortgage insurance. This is because it lowers the risk to the lender of making a loan to you, allowing you to qualify for a loan that you might not otherwise be approved for.

Mortgage insurance can come in the form of a monthly premium payment or a lump-sum payment at the time of mortgage origination. The type of mortgage insurance you need will depend on factors such as the type of mortgage and the size of your down payment. Private mortgage insurance (PMI) is the most common type of insurance, but there is also mortgage title insurance and mortgage insurance premium (MIP) insurance, which is required for Federal Housing Administration (FHA) and U.S. Department of Agriculture (USDA) loans.

If you have a conventional loan, you can request to cancel your PMI once your loan balance reaches 80% of your home's original value. The Homeowners Protection Act of 1998 (HPA) also requires that mortgage lenders automatically cancel PMI when the loan-to-value (LTV) ratio reaches 78% of the home's purchase price or the month after the midpoint of the loan term. For example, if you have a 30-year loan, your lender must cancel PMI after 15 years.

If your home's value has increased due to appreciation or renovations, you may be eligible to request a PMI cancellation. However, you will need to pay for a home appraisal to verify the new market value.

For FHA loans, you will need to pay MIP for either 11 years or the entire length of the loan, depending on the terms. You can refinance to a conventional loan to get rid of MIP.

It is important to note that mortgage insurance protects the lender, not the borrower. Cancelling mortgage insurance will reduce your monthly costs, but it is essential to understand the risks and ensure that you are current on your payments to be eligible for cancellation.

Hotel Insurance: Is the Cost Worth the Coverage?

You may want to see also

Frequently asked questions

Mortgage insurance is an insurance policy that protects the lender or investor in the event that the borrower defaults on their mortgage. It is also known as mortgage guarantee or home-loan insurance.

Mortgage insurance protects the lender, not the borrower. It lowers the risk to the lender of issuing a loan and helps the borrower qualify for a loan they may not have been able to get without insurance.

Mortgage insurance is typically required when the borrower makes a down payment of less than 20% of the purchase price of the home. It is also usually required for Federal Housing Administration (FHA) and U.S. Department of Agriculture (USDA) loans.

There are two main types of mortgage insurance: mortgage default insurance and mortgage protection insurance. Mortgage default insurance is mandatory for certain loans, while mortgage protection insurance is optional and can help cover payments during financial hardship.

The cost of mortgage insurance varies depending on the loan type and down payment amount. It typically costs between 1% and 4% of the home's purchase price and can be paid monthly or as a lump sum.