When discussing health insurance coverage, it's essential to understand the various forms and documents that verify your insurance status throughout the year. One such form is the 1095-C, which is provided by your employer and details the health insurance coverage you had during the previous year. This form is crucial for tax purposes and helps you determine if you had continuous health insurance coverage. It includes information such as the months you were covered, the type of coverage, and the employer's contribution to your premiums. By reviewing this form, you can ensure that you had health insurance all year and avoid any potential tax penalties for gaps in coverage.

| Characteristics | Values |

|---|---|

| Form Type | Health Insurance Form |

| Coverage Period | All Year |

| Purpose | To provide proof of health insurance coverage |

| Required Information | Personal details, insurance provider, policy number, coverage dates |

| Submission Method | Online, mail, or in-person |

| Processing Time | Varies depending on the provider |

| Importance | Essential for tax purposes, employer verification, or eligibility for certain programs |

Explore related products

What You'll Learn

- Understanding the Form: Explanation of the specific form that indicates year-long health insurance coverage

- Key Sections to Review: Highlighting the important parts of the form to verify continuous insurance

- Common Mistakes to Avoid: Tips on avoiding errors when filling out or interpreting the insurance form

- Proof of Coverage: What constitutes valid proof of health insurance coverage throughout the year

- Consequences of Lapses: Potential impacts of gaps in health insurance coverage and how to address them

![]()

Understanding the Form: Explanation of the specific form that indicates year-long health insurance coverage

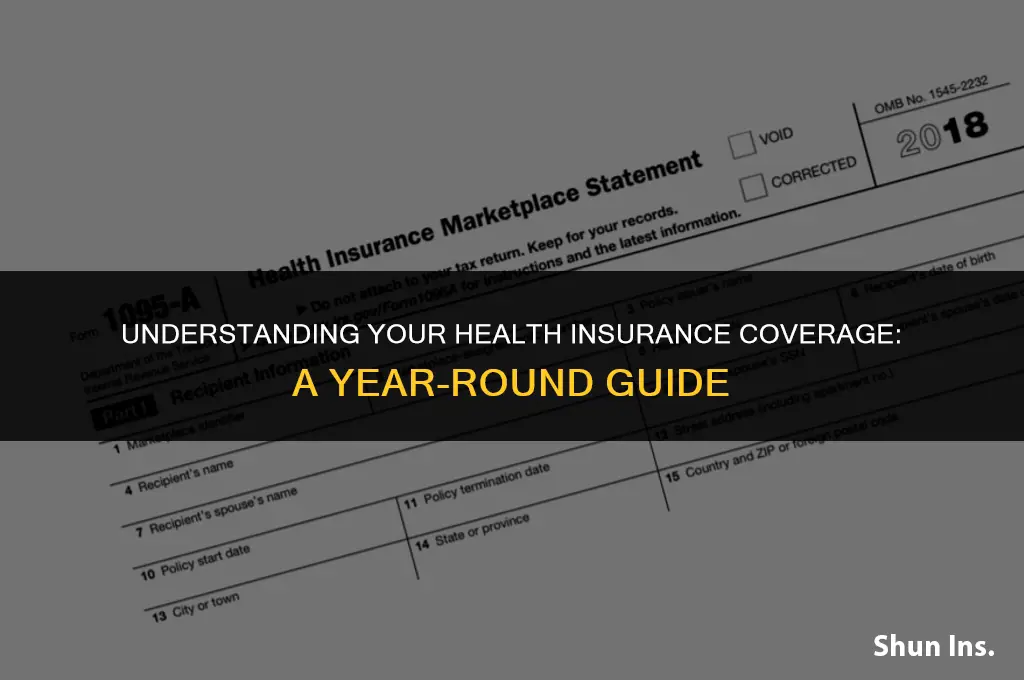

The form that indicates year-long health insurance coverage is typically a 1095 form, which is issued by your health insurance provider. This form is crucial for tax purposes, as it verifies that you had health insurance coverage for the entire year, which is a requirement under the Affordable Care Act (ACA). The 1095 form includes important information such as the dates of coverage, the type of plan, and the premium amounts paid. It is essential to review this form carefully to ensure that all the information is accurate, as any discrepancies could lead to issues with your tax return.

Understanding the 1095 form is key to ensuring that you are in compliance with the ACA's individual mandate. The form is divided into several sections, each providing specific details about your health insurance coverage. For example, Part II of the form lists the months of the year and indicates whether you had coverage during each month. This section is particularly important, as it allows you to see at a glance whether there were any gaps in your coverage. If you notice any errors in this section, it is important to contact your health insurance provider immediately to have the form corrected.

Another important aspect of the 1095 form is Part III, which provides information about the type of health insurance plan you had. This section includes details such as the plan name, the plan ID, and the network type. It is essential to review this information to ensure that it matches the plan you selected during the enrollment period. If there are any discrepancies, it could indicate that you were enrolled in the wrong plan, which could have implications for your coverage and your tax liability.

In addition to providing information about your health insurance coverage, the 1095 form also includes details about the premium amounts you paid throughout the year. This information is important for tax purposes, as it allows you to calculate the premium tax credit you may be eligible for. The premium tax credit is a subsidy that helps make health insurance more affordable for low- and middle-income individuals. To be eligible for the premium tax credit, you must have purchased health insurance through the health insurance marketplace and have a household income within certain limits.

In conclusion, the 1095 form is a critical document that provides proof of year-long health insurance coverage. It is essential to review this form carefully to ensure that all the information is accurate and to identify any potential issues that could affect your tax return. By understanding the different sections of the form and the information they provide, you can ensure that you are in compliance with the ACA's individual mandate and that you are taking advantage of any available subsidies.

Does Health Insurance Cover Labiaplasty? Understanding Coverage and Costs

You may want to see also

Explore related products

$26.99

![]()

Key Sections to Review: Highlighting the important parts of the form to verify continuous insurance

To verify continuous health insurance, it's crucial to review specific sections of the form meticulously. The first key section is the "Coverage Period" which clearly states the start and end dates of your insurance policy. Ensure that there are no gaps between the dates, as even a single day without coverage can lead to complications. Next, examine the "Policy Details" section, which should list the type of coverage, any exclusions, and the premium payment history. This section is vital as it confirms that you have maintained the necessary payments to keep your policy active.

Another important part to review is the "Claims History" section. This will show any claims you've made during the year and their status. If there are any denied claims, investigate the reasons behind them to ensure they don't indicate a lapse in coverage. Additionally, check the "Beneficiary Information" to ensure that your designated beneficiaries are up-to-date, as changes in personal circumstances can affect who receives benefits in case of an emergency.

Lastly, pay close attention to any "Renewal Information" provided. This section will detail the process for renewing your policy and any changes in terms or conditions that may apply. By reviewing these key sections, you can ensure that your health insurance coverage has been continuous and that you are fully protected.

Your Guide to Applying for Health Insurance in Washington, DC

You may want to see also

Explore related products

$11.3 $22.96

![]()

Common Mistakes to Avoid: Tips on avoiding errors when filling out or interpreting the insurance form

One common mistake to avoid when filling out or interpreting the insurance form is failing to read the instructions carefully. Insurance forms often contain specific guidelines on how to complete each section, and overlooking these can lead to errors. For example, some forms may require you to list all healthcare providers you've visited in the past year, while others may only ask for information about hospitalizations. Make sure to follow the instructions precisely to ensure your form is filled out correctly.

Another mistake to avoid is not double-checking your information. It's easy to make typos or forget important details when filling out a form, especially if you're doing it quickly. Take the time to review your responses and make sure everything is accurate and complete. This includes verifying your personal information, such as your name, address, and date of birth, as well as ensuring that all dates and medical information are correct.

When interpreting the insurance form, be cautious of ambiguous language. Insurance policies can be complex, and the wording on the form may not always be clear. If you're unsure about what a particular question is asking or what a term means, don't hesitate to reach out to your insurance provider for clarification. It's better to ask questions upfront than to make assumptions and potentially submit incorrect information.

Additionally, be aware of any deadlines associated with submitting the form. Insurance companies often have strict timeframes for when forms must be completed and returned, and missing these deadlines can result in penalties or loss of coverage. Make sure to note any due dates on your calendar and allow yourself plenty of time to fill out and submit the form.

Finally, keep a copy of the completed form for your records. This can be helpful in case you need to reference the information later or if there are any disputes about your coverage. Having a copy on hand can also make it easier to fill out future forms, as you'll have a reference point for the information you've previously provided.

Top Corporate Investors Dominating Health Insurance Company Stock Ownership

You may want to see also

Explore related products

![]()

Proof of Coverage: What constitutes valid proof of health insurance coverage throughout the year

Valid proof of health insurance coverage throughout the year typically includes documents that verify your enrollment and payment status with an insurance provider. These documents may vary depending on the type of insurance you have, but common examples include:

- Insurance Cards: Most insurance providers issue cards that display your name, policy number, effective dates, and contact information for the insurance company. These cards serve as a quick reference for healthcare providers and can be used to verify your coverage at appointments or when filling prescriptions.

- Explanation of Benefits (EOB) Statements: These statements are sent to you after a claim has been processed and detail the services provided, the amount billed, and the portion covered by your insurance. EOBs can serve as proof of coverage for specific medical expenses and can be useful in resolving disputes or understanding your out-of-pocket costs.

- Policy Certificates: For some types of insurance, such as individual or family plans, you may receive a policy certificate that outlines the terms of your coverage, including the effective dates, coverage limits, and exclusions. This document can be used to verify that you have maintained continuous coverage throughout the year.

- Payment Receipts: If you pay your insurance premiums directly, keeping receipts for these payments can serve as proof of coverage. This is particularly important if you have a lapse in coverage and need to demonstrate that you have been making regular payments to reinstate your policy.

- Employer-Provided Documents: If you receive health insurance through your employer, they may provide you with documents such as a Summary Plan Description (SPD) or a Certificate of Creditable Coverage. These documents can be used to verify your coverage and may be required when applying for other types of insurance or government benefits.

It's important to keep these documents organized and easily accessible, as you may need to provide proof of coverage when filing taxes, applying for financial aid, or resolving disputes with healthcare providers. Additionally, maintaining continuous coverage throughout the year can help you avoid penalties and ensure that you have access to necessary medical care.

Medical Insurance: Individual Coverage Explained

You may want to see also

Explore related products

![]()

Consequences of Lapses: Potential impacts of gaps in health insurance coverage and how to address them

Lapses in health insurance coverage can have severe consequences, affecting not only an individual's health but also their financial stability. A gap in coverage can lead to delayed or forgone medical care, resulting in untreated conditions that may worsen over time. This can culminate in higher medical costs when treatment is eventually sought, as well as potential long-term health complications.

One of the most significant impacts of a coverage lapse is the risk of incurring substantial medical debt. Without insurance, even routine medical procedures can become prohibitively expensive, forcing individuals to either delay care or pay out-of-pocket. This can lead to financial strain, damaged credit scores, and even bankruptcy in extreme cases. Furthermore, gaps in coverage can result in the loss of continuity of care, making it difficult for healthcare providers to manage chronic conditions effectively.

To address these issues, it is crucial to maintain continuous health insurance coverage. This can be achieved by carefully reviewing and understanding the terms of one's insurance policy, ensuring timely renewal, and exploring options for temporary coverage if a lapse occurs. Additionally, individuals should be aware of their rights and protections under healthcare laws, such as the Affordable Care Act, which may provide avenues for obtaining coverage or appealing denials.

In some cases, individuals may be eligible for Medicaid or other government-assisted programs, which can help fill gaps in coverage. It is also important to consider supplemental insurance options, such as short-term health plans or health savings accounts, which can provide additional financial protection in the event of a coverage lapse. By taking proactive steps to maintain continuous coverage, individuals can mitigate the risks associated with gaps in health insurance and ensure they have access to necessary medical care.

Understanding RAMQ: Quebec's Public Medical Insurance Plan

You may want to see also

Frequently asked questions

The form you need is typically a 1095 form, which is sent to you by your health insurance provider.

The 1095 form includes information about your health insurance coverage, such as the dates of coverage, the type of plan, and the amount of premiums paid.

Your health insurance provider should send you the 1095 form by January 31st each year. If you don't receive it, you can contact your provider to request a copy.

The 1095 form is important because it serves as proof of health insurance coverage when filing your taxes. It helps you avoid the penalty for not having health insurance and can also be used to claim certain tax credits.

If you had multiple health insurance plans, you may receive separate 1095 forms for each plan. You should keep all of these forms and provide them when filing your taxes to ensure accurate reporting of your coverage.