Catastrophic health insurance, once a vital safety net for individuals facing severe medical expenses, has undergone significant changes over the years. Initially designed to cover high-cost medical treatments and procedures, this type of insurance was particularly important for those with chronic conditions or those who faced unexpected health crises. However, with the advent of the Affordable Care Act (ACA) in 2010, the landscape of health insurance shifted dramatically. The ACA aimed to increase access to healthcare and reduce costs, but it also led to the discontinuation of many catastrophic health insurance plans. These plans were often seen as too limited in coverage and too expensive for the average consumer. As a result, many individuals were forced to seek alternative coverage options, such as more comprehensive plans offered through health insurance exchanges or employer-sponsored plans. Today, the legacy of catastrophic health insurance continues to shape the ongoing debate over healthcare reform and the future of health insurance in the United States.

| Characteristics | Values |

|---|---|

| Name | Catastrophic Health Insurance |

| Purpose | Provides coverage for unexpected and high-cost medical expenses |

| Coverage Type | Secondary insurance |

| Primary Insurance Requirement | Must have primary health insurance |

| Deductible | Typically high |

| Premium | Lower than primary insurance |

| Coverage Limit | Covers expenses above primary insurance limits |

| Network | Often has a wide network of providers |

| Eligibility | Available to individuals and families |

| Enrollment Period | Can be enrolled in during open enrollment periods |

| Tax Benefits | Premiums may be tax-deductible |

| Impact on Primary Insurance | Does not affect primary insurance coverage |

| Cost-Sharing | May involve coinsurance or copays |

| Pre-Existing Conditions | Coverage may vary for pre-existing conditions |

| Waiting Period | May have a waiting period before coverage begins |

Explore related products

What You'll Learn

- Market Changes: Shifts in healthcare market dynamics and provider networks

- Regulatory Impact: Effects of the Affordable Care Act and other legislation

- Consumer Options: Evolution of health plan choices and coverage levels

- Financial Aspects: Changes in premium costs, subsidies, and out-of-pocket expenses

- Healthcare Access: Variations in access to healthcare services and facilities

![]()

Market Changes: Shifts in healthcare market dynamics and provider networks

The healthcare market has undergone significant transformations in recent years, particularly in the realm of catastrophic health insurance. One of the most notable shifts has been the consolidation of provider networks, where larger healthcare systems absorb smaller, independent practices. This consolidation can lead to reduced competition, potentially driving up costs for consumers. Additionally, the rise of telehealth services has expanded access to care, but also introduced new challenges in terms of reimbursement and quality control.

Another key market change is the increasing prevalence of high-deductible health plans (HDHPs), which have become a popular choice for employers looking to reduce their healthcare costs. While HDHPs can be more affordable for employers, they often result in higher out-of-pocket expenses for employees, particularly those with chronic conditions or who require frequent medical attention. This shift has led to a growing emphasis on health savings accounts (HSAs) and other tax-advantaged savings vehicles to help consumers manage their healthcare expenses.

Furthermore, the Affordable Care Act (ACA) has had a profound impact on the healthcare market, particularly in terms of expanding coverage to previously uninsured individuals. However, the ACA has also faced numerous challenges, including legal battles and political opposition, which have led to uncertainty about its future. This uncertainty has created a volatile market environment, making it difficult for insurers and providers to plan for the long term.

In response to these market changes, many healthcare providers have begun to adopt value-based care models, which focus on improving patient outcomes while reducing costs. This shift away from traditional fee-for-service models has been driven by the need to control costs and improve the quality of care. Value-based care models often involve collaborative relationships between providers, insurers, and patients, with a shared goal of achieving better health outcomes at a lower cost.

Finally, the increasing use of data analytics and artificial intelligence (AI) in healthcare has the potential to revolutionize the way care is delivered and managed. These technologies can help providers identify high-risk patients, predict disease outbreaks, and optimize treatment plans. However, the adoption of these technologies also raises important questions about privacy, security, and the potential for bias in AI algorithms.

Overall, the healthcare market is in a state of flux, with numerous changes and challenges shaping the way care is delivered and paid for. As the market continues to evolve, it is essential for providers, insurers, and policymakers to work together to ensure that high-quality, affordable care remains accessible to all.

Does Health Insurance Cover Funeral Expenses? What You Need to Know

You may want to see also

Explore related products

![]()

Regulatory Impact: Effects of the Affordable Care Act and other legislation

The Affordable Care Act (ACA), signed into law in 2010, marked a significant shift in the U.S. healthcare landscape. One of its primary goals was to increase access to health insurance for millions of Americans, many of whom were struggling with the high costs of catastrophic health insurance. The ACA introduced several key provisions aimed at addressing these issues, including the establishment of health insurance exchanges, the expansion of Medicaid, and the implementation of subsidies to help lower-income individuals afford coverage.

One of the most notable effects of the ACA was the reduction in the number of Americans without health insurance. According to the Kaiser Family Foundation, the uninsured rate dropped from 16.3% in 2010 to 9.2% in 2019. This decline was particularly pronounced among low-income individuals and those with pre-existing conditions, who had previously faced significant barriers to obtaining affordable coverage.

The ACA also had a profound impact on the health insurance industry itself. Insurers were required to adhere to new regulations, such as the prohibition on denying coverage based on pre-existing conditions and the mandate to cover essential health benefits. These changes led to a more competitive marketplace, with insurers vying to offer plans that met the new standards while remaining affordable for consumers.

However, the ACA was not without its challenges and controversies. Critics argued that the law led to higher premiums for some individuals, particularly those who did not qualify for subsidies. Additionally, the requirement for individuals to maintain coverage or face a penalty was met with resistance, with some viewing it as an infringement on personal freedom.

In the years following the ACA's implementation, there have been numerous attempts to repeal or modify the law. The Tax Cuts and Jobs Act of 2017, for example, eliminated the individual mandate penalty, leading to concerns that fewer Americans would maintain coverage. However, the ACA has proven to be resilient, with many of its key provisions remaining in place despite these challenges.

Overall, the ACA and other legislation have had a significant impact on the availability and affordability of catastrophic health insurance in the United States. While there are still challenges to be addressed, the law has undoubtedly expanded access to healthcare for millions of Americans and has fundamentally changed the way the health insurance industry operates.

Understanding Government Subsidies for Health Insurance: Benefits and Eligibility

You may want to see also

Explore related products

![]()

Consumer Options: Evolution of health plan choices and coverage levels

Over the past few decades, the landscape of health insurance has undergone significant changes, particularly in the realm of consumer options. The evolution of health plan choices and coverage levels has been marked by a shift towards more diverse and tailored plans, catering to a wide range of consumer needs and preferences. This transformation has been driven by various factors, including changes in healthcare policy, advancements in medical technology, and shifting consumer attitudes towards health and wellness.

One notable development has been the rise of high-deductible health plans (HDHPs), which have become increasingly popular among consumers seeking to lower their monthly premiums. These plans typically feature lower premiums in exchange for higher out-of-pocket costs, including deductibles and copays. HDHPs have been particularly appealing to younger, healthier individuals who are less likely to require frequent medical care. However, they have also raised concerns about the potential for increased financial burden on consumers who may face unexpected medical expenses.

Another significant trend has been the growth of health savings accounts (HSAs) and flexible spending accounts (FSAs), which allow consumers to set aside pre-tax dollars for healthcare expenses. These accounts have provided consumers with greater flexibility and control over their healthcare spending, enabling them to save for future medical needs or cover out-of-pocket costs more efficiently. Additionally, the increasing prevalence of telemedicine and virtual healthcare services has expanded consumer access to medical care, particularly in rural or underserved areas.

The Affordable Care Act (ACA) has also played a crucial role in shaping consumer options in health insurance. The ACA introduced new regulations and standards for health plans, including the requirement for essential health benefits and the prohibition of pre-existing condition exclusions. These changes have led to a more standardized and transparent health insurance market, making it easier for consumers to compare plans and make informed decisions about their coverage.

Furthermore, the emergence of health insurance exchanges and online marketplaces has revolutionized the way consumers shop for health insurance. These platforms have made it possible for consumers to easily compare plans, prices, and coverage levels from multiple insurers, facilitating a more competitive and consumer-friendly market. The increasing use of data analytics and artificial intelligence in healthcare has also enabled insurers to offer more personalized and targeted health plans, based on individual consumer needs and risk profiles.

In conclusion, the evolution of consumer options in health insurance has been characterized by a move towards greater diversity, flexibility, and personalization. While these changes have brought about numerous benefits for consumers, including lower premiums and increased access to care, they have also introduced new challenges and complexities. As the healthcare landscape continues to evolve, it is essential for consumers to stay informed and adapt to the changing options and coverage levels available to them.

Prenatal Massage Coverage: What Your Health Insurance May Offer

You may want to see also

Explore related products

![]()

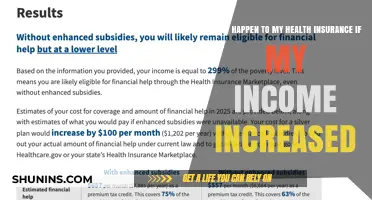

Financial Aspects: Changes in premium costs, subsidies, and out-of-pocket expenses

The financial landscape of catastrophic health insurance has undergone significant transformations in recent years. One of the most notable changes is the fluctuation in premium costs. Insurers have had to adjust their pricing models to account for the increasing costs of healthcare services, resulting in higher premiums for policyholders. This shift has been particularly challenging for individuals and families who rely on catastrophic health insurance for protection against major medical expenses.

In addition to rising premium costs, changes in subsidies have also impacted the affordability of catastrophic health insurance. Government subsidies, which were once a critical component in making health insurance accessible to a broader population, have been reduced or eliminated in some cases. This reduction in financial assistance has left many individuals struggling to afford the coverage they need, forcing them to either opt for less comprehensive plans or forgo insurance altogether.

Out-of-pocket expenses have also seen a significant increase, further exacerbating the financial burden on policyholders. Higher deductibles, copays, and coinsurance rates have become the norm, requiring individuals to pay more upfront for their healthcare needs. This trend has been particularly problematic for those with catastrophic health insurance, as they are often faced with substantial medical bills even after their insurance coverage kicks in.

The cumulative effect of these financial changes has been a shift in the way individuals and families approach health insurance. Many are now more cautious about their healthcare spending, opting for preventive care and wellness programs to mitigate the risk of incurring high medical costs. Others are exploring alternative insurance options, such as health savings accounts (HSAs) and flexible spending accounts (FSAs), to help manage their out-of-pocket expenses.

In conclusion, the financial aspects of catastrophic health insurance have become increasingly complex and challenging. Rising premium costs, reduced subsidies, and higher out-of-pocket expenses have forced individuals to reevaluate their approach to health insurance and seek out new strategies for managing their healthcare costs. As the healthcare landscape continues to evolve, it is essential for policyholders to stay informed and adapt their insurance plans accordingly to ensure they have the coverage they need without breaking the bank.

Private Medical Insurance: Personalized, Swift, Comprehensive Care

You may want to see also

Explore related products

![]()

Healthcare Access: Variations in access to healthcare services and facilities

Variations in access to healthcare services and facilities have significant implications for the effectiveness of catastrophic health insurance. In regions with limited healthcare infrastructure, such as rural areas or low-income countries, individuals may face challenges in obtaining timely and adequate medical care, even when they have insurance coverage. This can lead to delayed diagnoses, inadequate treatment, and ultimately, poorer health outcomes.

One of the key factors contributing to these variations is the distribution of healthcare providers and facilities. In many cases, healthcare resources are concentrated in urban areas, leaving rural and remote populations with limited access to care. This disparity can be exacerbated by factors such as transportation costs, language barriers, and cultural differences, which can further hinder individuals' ability to access healthcare services.

Another important factor is the availability of specialized care. In some regions, there may be a shortage of specialists or advanced medical equipment, making it difficult for individuals to receive the care they need for complex or chronic conditions. This can be particularly problematic for those with catastrophic health insurance, as they may require more intensive and specialized care than those with more comprehensive coverage.

To address these variations in access to healthcare services and facilities, policymakers and healthcare organizations can implement a range of strategies. These may include increasing funding for healthcare infrastructure in underserved areas, providing incentives for healthcare providers to work in rural or remote locations, and investing in telemedicine technologies to improve access to care. Additionally, efforts to improve health literacy and address cultural and language barriers can help to ensure that all individuals have the knowledge and resources they need to access healthcare services effectively.

Ultimately, addressing variations in access to healthcare services and facilities is critical to ensuring that catastrophic health insurance is effective in protecting individuals from financial ruin due to unexpected medical expenses. By improving access to care, we can help to ensure that all individuals have the opportunity to receive the care they need, regardless of where they live or their socioeconomic status.

Does Mexican Health Insurance Meet U.S. Shared Responsibility Requirements?

You may want to see also

Frequently asked questions

After the ACA, catastrophic health insurance plans became less common because the law required most health plans to cover essential health benefits, which these plans typically did not. However, they still exist in some forms, such as short-term limited-duration insurance and health savings accounts (HSAs).

The ACA changed the definition of catastrophic health insurance by requiring that all health plans, including catastrophic plans, cover essential health benefits and meet certain actuarial values. This meant that catastrophic plans could no longer be as bare-bones as they were before, and they had to provide more comprehensive coverage.

Yes, catastrophic health insurance plans are still available for purchase, but they are less common than they were before the ACA. They are typically only available to people who are under 30 or who qualify for a hardship exemption. Additionally, some states have their own versions of catastrophic plans that are available to residents.