Not enrolling in health insurance can have significant financial and health-related consequences. Without coverage, individuals are responsible for paying the full cost of medical services out of pocket, which can lead to substantial debt or even bankruptcy in the event of a serious illness or injury. Additionally, uninsured individuals may delay or forgo necessary medical care due to cost concerns, potentially worsening health conditions and increasing long-term healthcare expenses. Beyond personal risks, the Affordable Care Act (ACA) imposes a tax penalty for not having insurance in some states, though this penalty has been eliminated at the federal level. Overall, lacking health insurance exposes individuals to financial vulnerability and compromises their ability to access timely and affordable healthcare.

| Characteristics | Values |

|---|---|

| Financial Penalties | No federal penalty for not having health insurance (as of 2023), but some states (e.g., California, Massachusetts, New Jersey, Rhode Island, Vermont) impose penalties or taxes for uninsured residents. |

| Out-of-Pocket Costs | Full responsibility for medical expenses, including emergencies, hospitalizations, and routine care, without insurance coverage. |

| Limited Access to Care | Difficulty accessing affordable healthcare; providers may require upfront payment or deny non-emergency services. |

| Preventive Care | Lack of coverage for preventive services (e.g., vaccinations, screenings), increasing long-term health risks. |

| Emergency Care | Legally guaranteed emergency care under EMTALA, but uninsured individuals are responsible for all costs afterward. |

| Prescription Drugs | Full payment for medications without insurance discounts or subsidies. |

| Long-Term Health Risks | Delayed or forgone care due to cost, leading to untreated conditions and poorer health outcomes. |

| Debt and Bankruptcy | Medical debt is a leading cause of bankruptcy for uninsured individuals. |

| State-Specific Consequences | Some states offer limited safety-net programs, but coverage is inconsistent and often insufficient. |

| Tax Implications | No federal tax penalty, but state penalties may apply and reduce refunds or increase taxes owed. |

| Impact on Family | Uninsured individuals may strain family finances if medical emergencies occur. |

| Alternative Options | May qualify for Medicaid, CHIP, or short-term health plans, but coverage is limited compared to ACA-compliant plans. |

Explore related products

What You'll Learn

![]()

Financial penalties for not having insurance

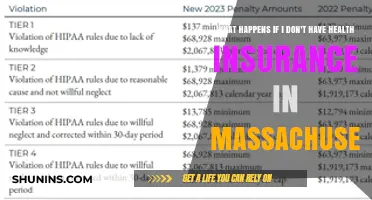

Failing to enroll in health insurance can trigger financial penalties, particularly in regions with individual mandates. In the United States, while the federal tax penalty for not having insurance under the Affordable Care Act (ACA) was eliminated in 2019, several states have implemented their own mandates. For example, California, Massachusetts, New Jersey, Rhode Island, and the District of Columbia impose penalties on residents who go without coverage. These penalties vary but often mirror the previous federal structure, calculating fees as a percentage of income or a flat amount, whichever is higher. For instance, California’s penalty can reach up to 2.5% of annual household income, while New Jersey’s flat fee starts at $695 per adult. Understanding your state’s specific rules is critical to avoiding unexpected costs.

The financial impact of these penalties extends beyond the immediate fine. Uninsured individuals often face higher out-of-pocket costs when medical needs arise, as they lack the negotiated rates and coverage benefits that insurance provides. A single emergency room visit, for example, can cost upwards of $1,000 without insurance, compared to a typical $200-$300 copay for insured patients. Over time, these expenses can compound, creating a financial burden that far exceeds the cost of annual premiums. Thus, while avoiding insurance might seem like a short-term savings strategy, it often leads to greater long-term financial vulnerability.

From a comparative perspective, the penalties for not having insurance are designed to encourage enrollment by making non-compliance financially unattractive. In states with mandates, the penalties are structured to offset the potential costs of uncompensated care, which uninsured individuals might otherwise shift to taxpayers or insured populations. For example, Massachusetts, which pioneered the individual mandate model, has seen lower rates of uncompensated care since implementing its penalty system. This suggests that while penalties may feel punitive, they serve a broader purpose in stabilizing healthcare costs for the community.

To mitigate the risk of penalties, proactive steps are essential. First, verify whether your state has an individual mandate and understand the specific penalties for non-compliance. Second, explore available coverage options, including employer-sponsored plans, ACA marketplace plans, or Medicaid, depending on your income level. For those under 30 or with financial hardships, catastrophic health plans or short-term health insurance may offer a lower-cost alternative, though they may not exempt you from state penalties. Finally, take advantage of open enrollment periods or qualifying life events (e.g., marriage, job loss) to secure coverage without facing gaps that could trigger fines.

In conclusion, financial penalties for not having health insurance are a tangible consequence in states with individual mandates, serving as both a deterrent and a mechanism to balance healthcare costs. By understanding these penalties, assessing your coverage options, and taking timely action, you can avoid unnecessary financial strain while ensuring access to essential healthcare services. Ignoring this responsibility not only risks penalties but also exposes you to the high costs of unexpected medical expenses, making insurance a critical component of financial planning.

Thyroid Medication Costs Without Insurance: What You Need to Know

You may want to see also

Explore related products

![]()

Limited access to healthcare services

Without health insurance, the financial burden of medical care often leads to delayed or forgone treatment. A 2021 Commonwealth Fund survey found that 43% of uninsured adults skipped necessary care due to cost, compared to 17% of insured adults. This delay can turn minor, treatable conditions—like infections or early-stage chronic diseases—into severe, costly emergencies. For example, an untreated urinary tract infection, manageable with a $20 antibiotic, can escalate to a $20,000 hospitalization for sepsis. Similarly, a missed annual mammogram (averaging $100–$250 without insurance) increases the likelihood of detecting breast cancer at a late, harder-to-treat stage.

The uninsured often rely on emergency departments (EDs) for primary care, a costly and inefficient workaround. Federal law mandates EDs stabilize patients regardless of insurance, but this does not cover follow-up care. A 2018 study in *Health Affairs* showed uninsured patients were 40% more likely to use the ED for preventable issues like asthma exacerbations or diabetes complications. These visits average $1,300 each, compared to $150 for a primary care visit. Without preventive management, conditions like hypertension (affecting 1 in 3 adults) go uncontrolled, raising the risk of heart attacks or strokes—events that cost $100,000+ to treat.

Uninsured individuals face barriers to specialty care, even when referred. A 2020 Kaiser Family Foundation report found 45% of specialists refuse uninsured patients outright, while others charge 2–3 times the insured rate. For instance, a 30-minute dermatology consultation averages $300 uninsured vs. $100 with insurance. This limits access to critical services like mental health therapy (average $125/session uninsured) or physical therapy ($80–$150/session), forcing patients to self-manage conditions like depression or post-surgical recovery. Adolescents and young adults (ages 18–26) are particularly vulnerable, as 14% remain uninsured and often lack employer-based coverage.

Practical strategies can mitigate, though not eliminate, these gaps. Federally Qualified Health Centers (FQHCs) offer sliding-scale fees based on income, reducing costs by up to 75% for services like dental cleanings ($50–$150) or blood tests ($20–$50). Prescription discount apps (e.g., GoodRx) cut medication costs by 50–80%, though they don’t replace comprehensive coverage. For example, insulin, averaging $300/month uninsured, drops to $50–$100 with discounts. However, these solutions address symptoms, not the root problem: without insurance, systemic barriers persist, leaving millions at risk of suboptimal care.

When and Why to Switch Health Insurance Plans for Optimal Coverage

You may want to see also

Explore related products

![]()

Risk of high out-of-pocket costs

Without health insurance, a routine doctor’s visit can spiral into a financial crisis. Consider this: a minor emergency room trip for a sprained ankle averages $1,233 out-of-pocket, while an uninsured appendectomy can exceed $30,000. These aren’t edge cases—they’re common scenarios that highlight the immediate vulnerability of going uninsured. Even preventive care, like a $150 annual physical, becomes a gamble when weighed against unexpected costs. The absence of negotiated rates, which insurers secure for policyholders, leaves the uninsured paying up to 300% more for services. This isn’t just about big-ticket emergencies; it’s the cumulative weight of smaller, unavoidable expenses that erode financial stability.

Now, let’s break down the mechanics of this risk. Without insurance, you’re responsible for 100% of medical costs upfront. Hospitals and providers often charge uninsured patients their full "list price," which is significantly higher than the discounted rates insurers negotiate. For instance, a CT scan billed at $5,000 might be reduced to $1,500 for an insured patient. Add to this the lack of cost-sharing mechanisms like copays or deductibles, and you’re left with no financial buffer. Even prescription medications, which can cost $300–$500 monthly for chronic conditions, become unaffordable without insurance subsidies. This system isn’t designed for individual payers—it’s structured around bulk discounts that exclude the uninsured.

To mitigate this risk, consider these practical steps. First, research safety-net programs like community health centers, which offer sliding-scale fees based on income. For example, a family of four earning $50,000 annually might pay $50 for a visit instead of $200. Second, negotiate medical bills directly with providers. Many hospitals have financial assistance policies but require proactive requests. Third, explore prescription discount cards (e.g., GoodRx) to reduce medication costs by up to 80%. Finally, set aside a health-specific emergency fund, even if it’s just $20 monthly—small savings can offset minor expenses before they compound.

The psychological toll of high out-of-pocket costs cannot be overlooked. Studies show that 66.5% of bankruptcies cite medical issues as a cause, often tied to uninsured or underinsured expenses. The stress of choosing between healthcare and essentials like rent or groceries creates a cycle of deferred care, worsening health outcomes and inflating future costs. For instance, untreated diabetes, which costs $1,000 annually to manage, can lead to $50,000 hospitalizations for complications. This isn’t merely a financial risk—it’s a threat to long-term well-being and stability.

In conclusion, the risk of high out-of-pocket costs without insurance isn’t theoretical; it’s a predictable consequence of a system designed around coverage. While stopgap measures like negotiation and safety nets can help, they’re no substitute for comprehensive insurance. The real takeaway? The cost of forgoing coverage often exceeds the price of a policy, making it a gamble few can afford to lose.

Understanding Insurance Company Permits: Key Regulations and Compliance Explained

You may want to see also

Explore related products

![]()

No preventive care coverage

Skipping health insurance means forgoing preventive care coverage, a decision that can lead to a cascade of health and financial consequences. Preventive care includes routine check-ups, vaccinations, screenings, and counseling aimed at detecting and mitigating health risks before they escalate. Without insurance, these services often come with out-of-pocket costs that many individuals delay or avoid altogether. For instance, a mammogram, which can detect breast cancer early, costs between $100 and $250 without insurance. Similarly, a colonoscopy, critical for colorectal cancer screening, can range from $500 to $3,000. These expenses, though seemingly manageable, often deter people from seeking timely care.

Consider the long-term implications of neglecting preventive care. Chronic conditions like diabetes, hypertension, and heart disease often develop silently, with symptoms appearing only after significant damage has occurred. Regular blood pressure checks, cholesterol screenings, and glucose tests—typically covered under preventive care—can identify these conditions early. Without insurance, individuals may not undergo these tests until symptoms force them to seek medical attention, by which time treatment becomes more invasive, costly, and less effective. For example, managing uncontrolled hypertension without early intervention can lead to stroke, heart attack, or kidney failure, requiring lifelong medication and potentially hospitalization.

From a financial perspective, the absence of preventive care coverage shifts the burden of healthcare costs entirely onto the individual. Vaccinations, such as the annual flu shot or the HPV vaccine, which prevent serious illnesses, can cost $50 to $200 without insurance. Similarly, well-child visits, which include developmental screenings and immunizations, are essential for children under 5 but can cost $100 to $200 per visit. These expenses add up quickly, especially for families. Moreover, the cost of treating preventable diseases far exceeds the price of preventive measures. For instance, treating advanced-stage cancer can cost hundreds of thousands of dollars, compared to the relatively modest cost of early detection screenings.

The societal impact of forgoing preventive care cannot be overlooked. Uninsured individuals who delay or avoid preventive services are more likely to end up in emergency rooms with advanced, costly-to-treat conditions. This not only strains healthcare resources but also drives up insurance premiums for everyone. For example, a study by the American Journal of Preventive Medicine found that preventable hospitalizations cost the U.S. healthcare system over $30 billion annually. By investing in preventive care, individuals not only protect their health but also contribute to a more sustainable healthcare system.

In practical terms, those without insurance can explore alternatives to mitigate the lack of preventive care coverage. Community health clinics often offer low-cost or sliding-scale services, including screenings and vaccinations. Employers or schools may provide free flu shots or health fairs with basic screenings. Additionally, government programs like Medicaid or the Children’s Health Insurance Program (CHIP) offer preventive care benefits for eligible individuals. While these options may not fully replace comprehensive insurance, they provide a safety net for those who cannot afford private coverage. Ultimately, understanding the value of preventive care and exploring available resources can help minimize the risks of going uninsured.

How an HSA Account Can Complement Your Health Insurance Plan

You may want to see also

Explore related products

$19.99 $26.99

![]()

Potential debt from medical emergencies

Medical emergencies don’t wait for convenient timing, and without health insurance, the financial fallout can be devastating. A single trip to the emergency room for a broken bone or appendicitis can easily cost thousands of dollars. For instance, the average ER visit in the U.S. ranges from $1,000 to $2,000, but complex cases like heart attacks or strokes can soar into the tens of thousands. These costs often include facility fees, physician charges, and diagnostic tests, none of which are discounted for uninsured patients. Without coverage, you’re left paying out of pocket, and hospitals are quick to send bills to collections if payment isn’t made promptly.

Consider the scenario of a 30-year-old uninsured individual who experiences a sudden appendicitis. The surgery, hospital stay, and post-operative care could total $15,000 or more. Without insurance, the hospital may offer a payment plan, but the monthly installments could still be prohibitively expensive. Missed payments lead to debt accumulation, damaged credit scores, and potential legal action. This isn’t just a hypothetical—studies show that medical debt is the leading cause of bankruptcy in the U.S., with uninsured individuals disproportionately affected.

The lack of insurance also discourages preventive care, which can exacerbate emergencies. For example, untreated high blood pressure or diabetes can lead to heart attacks or kidney failure, both of which are costly to treat. A $100 annual checkup could prevent a $50,000 emergency, but without insurance, many forgo these visits. This cycle of avoidance and crisis is a direct consequence of being uninsured, turning manageable conditions into financial disasters.

To mitigate this risk, explore low-cost options like community health clinics or state-funded programs. For instance, some states offer discounted care for uninsured residents based on income. Additionally, negotiate hospital bills—many providers reduce charges for self-pay patients if asked. While these steps can help, they’re no substitute for insurance. The takeaway is clear: medical emergencies don’t discriminate, but their financial impact does, and being uninsured leaves you vulnerable to debt that can derail your life.

Reporting Minor Accidents: When to Involve Insurance

You may want to see also

Frequently asked questions

If you don’t enroll in health insurance, you may face high out-of-pocket costs for medical care, including doctor visits, hospitalizations, and prescriptions. Additionally, in some regions, you might be subject to a tax penalty for not having coverage, though this varies by location and current laws.

Yes, you can still see a doctor without insurance, but you’ll be responsible for paying the full cost of services, which can be significantly higher than insured rates. Some clinics offer sliding-scale fees or payment plans for uninsured individuals.

Yes, alternatives include short-term health plans, health-sharing ministries, or community health centers that offer low-cost or free services. You may also qualify for government programs like Medicaid or subsidies through the Affordable Care Act (ACA) marketplace, depending on your income.