Failing to renew your health insurance can have significant and far-reaching consequences, leaving you financially vulnerable and without access to essential healthcare services. Without active coverage, you’ll be responsible for paying the full cost of medical treatments, prescriptions, and preventive care out of pocket, which can quickly become overwhelming in the event of an unexpected illness or injury. Additionally, you may face penalties or gaps in coverage that could exclude you from certain benefits or pre-existing condition protections when you eventually re-enroll. Long-term, lapsed coverage can also disrupt your ability to maintain continuity of care with trusted providers, potentially impacting your overall health and well-being. Understanding these risks underscores the importance of prioritizing timely renewal to ensure uninterrupted protection and peace of mind.

| Characteristics | Values |

|---|---|

| Loss of Coverage | You will no longer have health insurance benefits, including doctor visits, hospitalization, prescription drugs, and preventive care. |

| Financial Risk | You become personally responsible for all medical expenses, which can be extremely costly in case of emergencies or chronic conditions. |

| Penalty (U.S. Specific) | In some states, you may face a tax penalty for not having health insurance, though the federal individual mandate penalty was eliminated in 2019. |

| Pre-Existing Conditions | If you have a pre-existing condition, you may face higher premiums or be denied coverage when you try to re-enroll later. |

| Waiting Periods | Re-enrolling in a new plan may subject you to waiting periods before certain benefits (e.g., pre-existing conditions) are covered. |

| Loss of Subsidies | If you were receiving subsidies or tax credits to help pay for insurance, you will lose these benefits. |

| Difficulty in Re-Enrollment | Re-enrolling may require going through a new application process, including medical underwriting in some cases. |

| Impact on Preventive Care | Without insurance, you may skip preventive care, leading to undetected health issues that could worsen over time. |

| Emergency Care Costs | Emergency room visits without insurance can result in bills ranging from thousands to tens of thousands of dollars. |

| Impact on Mental Health | Lack of insurance may limit access to mental health services, potentially worsening mental health conditions. |

| **Legal Consequences (Country-Specific) | In some countries with mandatory health insurance, failure to renew may result in fines or legal penalties. |

| Employer-Sponsored Plans | If your insurance was through an employer, you may lose access to group rates and employer contributions. |

| Impact on Family Coverage | If you have dependents on your plan, they will also lose coverage, leaving them uninsured. |

| Administrative Hassles | Re-enrolling later may require additional paperwork, medical exams, or proof of insurability. |

| Long-Term Health Impact | Lack of continuous coverage can lead to delayed treatments, poorer health outcomes, and increased long-term healthcare costs. |

Explore related products

What You'll Learn

- Loss of Coverage: Immediate end to benefits, leaving you uninsured and financially vulnerable for medical expenses

- Pre-Existing Conditions: Risk losing coverage for pre-existing conditions if you reapply later

- Tax Penalties: Potential fines for non-compliance with mandatory health insurance laws in some regions

- Waiting Periods: Face waiting periods for new policies, delaying access to healthcare services

- Out-of-Pocket Costs: Full responsibility for medical bills without insurance coverage or subsidies

![]()

Loss of Coverage: Immediate end to benefits, leaving you uninsured and financially vulnerable for medical expenses

Failing to renew your health insurance triggers an immediate and irreversible loss of coverage. The moment your policy lapses, you’re no longer protected by its benefits. This means no more access to subsidized doctor visits, prescription drug discounts, or preventive care services. For instance, a routine checkup that would have cost $50 with insurance could now run you $200 or more out-of-pocket. This abrupt end to benefits leaves you exposed to the full financial burden of medical expenses, no matter how minor or major.

Consider the scenario of a 35-year-old individual who skips renewing their health insurance, thinking they’re healthy and unlikely to need care. A week later, they slip and fracture their wrist, requiring an emergency room visit, X-rays, and a cast. Without insurance, the bill could easily exceed $5,000. This example illustrates how quickly and unexpectedly medical costs can escalate, turning a manageable situation into a financial crisis. The absence of coverage doesn’t just affect emergencies; it also eliminates access to affordable chronic care management, mental health services, and maternity care, which are often included in comprehensive plans.

From a financial planning perspective, losing health insurance coverage is akin to driving without a seatbelt—risky and avoidable. The Affordable Care Act (ACA) mandates that most plans cover essential health benefits, including hospitalization, maternity care, and prescription drugs. Without these protections, you’re left to navigate the full cost of healthcare, which is notoriously unpredictable. For example, a three-day hospital stay can cost upwards of $30,000, while a single dose of a specialty drug might run $1,000 or more. These expenses can devastate savings, lead to debt, or even result in bankruptcy.

To mitigate this risk, take proactive steps to ensure continuous coverage. Set calendar reminders for renewal deadlines, and review your policy annually to confirm it still meets your needs. If you’re transitioning between jobs or plans, consider short-term health insurance as a temporary bridge, though be aware it often excludes pre-existing conditions and essential benefits. Additionally, explore options like COBRA, which allows you to extend employer-sponsored coverage for up to 18 months, albeit at a higher cost. Finally, if you’ve missed the renewal window, act quickly to enroll during the next open enrollment period or qualify for a special enrollment period due to a life event, such as losing coverage or having a child.

In summary, the immediate loss of health insurance coverage isn’t just an administrative oversight—it’s a critical financial vulnerability. Without benefits, you’re exposed to the full spectrum of healthcare costs, from routine care to catastrophic events. By understanding the stakes and taking proactive measures, you can avoid this precarious situation and maintain the protection you need.

Eddie Bauer Employee Benefits: Which Health Insurance Provider is Offered?

You may want to see also

Explore related products

![]()

Pre-Existing Conditions: Risk losing coverage for pre-existing conditions if you reapply later

Let’s say you’ve been managing asthma for years, and your current health insurance covers your inhalers and specialist visits without hassle. If you let that policy lapse and reapply later, insurers may treat your asthma as a pre-existing condition, excluding it from coverage entirely or imposing steep premiums. This isn’t hypothetical—it’s a real risk under many insurance frameworks, particularly in regions without robust protections like the Affordable Care Act (ACA). The ACA prohibits denying coverage for pre-existing conditions, but only if you maintain continuous coverage. A gap of just 63 days can reset the clock, leaving you vulnerable.

Consider the mechanics: insurers assess risk based on health history. A pre-existing condition like diabetes, hypertension, or even a past surgery can flag you as high-risk. If you reapply after a lapse, underwriters may scrutinize your medical records anew, potentially excluding treatments related to that condition or charging higher rates. For example, a 45-year-old with a history of heart disease might face exclusions for cardiac care or see premiums double compared to continuous coverage. This isn’t just about cost—it’s about access. Without coverage for a pre-existing condition, you’re left paying out-of-pocket for essential medications, tests, or procedures, which can quickly spiral into financial hardship.

Here’s a practical tip: if you’re transitioning between jobs or policies, ensure there’s no gap in coverage. COBRA, short-term health plans, or even Medicaid (if eligible) can bridge the gap temporarily. For instance, COBRA allows you to extend your employer-sponsored insurance for up to 18 months, though premiums are higher. Short-term plans are cheaper but often exclude pre-existing conditions, so read the fine print. If you’re under 26, staying on a parent’s plan can be a lifeline. The key is to avoid the reset—once a condition is labeled "pre-existing," it’s harder to regain comprehensive coverage.

Compare this to the relative stability of continuous coverage. Under the ACA, insurers cannot deny or limit coverage for pre-existing conditions during open enrollment or special enrollment periods (e.g., losing a job or moving). But these protections vanish if you let coverage lapse. For example, a 30-year-old with epilepsy who maintains coverage pays the standard premium and receives full benefits. If they lapse and reapply, they might face exclusions for anti-seizure medications or neurological care, turning a manageable condition into a financial and health crisis.

The takeaway is clear: letting health insurance lapse isn’t just about losing coverage temporarily—it’s about risking long-term access to care for conditions you already have. If you’re debating whether to renew, weigh the immediate cost against the potential consequences. For pre-existing conditions, the risk of losing coverage isn’t theoretical—it’s a tangible threat that can alter your health trajectory. Renewing isn’t just a financial decision; it’s a safeguard for your future.

Alabama Insurance Oversight: Who Regulates and Monitors Insurance Companies?

You may want to see also

Explore related products

$163.1 $245.95

![]()

Tax Penalties: Potential fines for non-compliance with mandatory health insurance laws in some regions

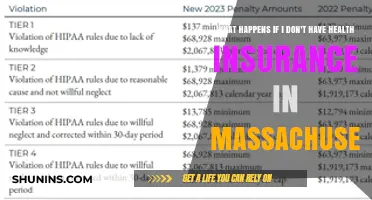

In regions with mandatory health insurance laws, failing to renew your coverage can trigger tax penalties, turning a lapse in insurance into a financial burden. These fines are designed to enforce compliance and maintain the stability of healthcare systems. For instance, in the United States under the Affordable Care Act (ACA), individuals without qualifying health insurance may face a penalty known as the Shared Responsibility Payment. While this penalty was reduced to $0 at the federal level in 2019, some states, like Massachusetts and New Jersey, have reinstated their own versions. In Massachusetts, the penalty for non-compliance can reach up to 50% of the lowest-cost monthly premium for a qualified health plan, calculated annually.

Understanding the mechanics of these penalties is crucial for avoiding unexpected costs. Penalties are often calculated based on the number of months you go without coverage and the income level of your household. For example, in California, the penalty for 2023 is either 2.5% of your household income over the tax filing threshold or a flat rate of $800 per adult and $400 per child, whichever is higher. To mitigate this, individuals should carefully track their insurance status and explore options like short-term plans or state-specific exemptions if they anticipate a coverage gap.

From a persuasive standpoint, these penalties serve as a reminder of the broader societal benefits of universal health coverage. By ensuring that everyone contributes to the system, mandatory insurance laws reduce the strain on public resources and promote equitable access to care. However, critics argue that such penalties disproportionately affect low-income individuals who may struggle to afford insurance premiums. To address this, many regions offer subsidies or waivers for those below certain income thresholds. For example, in New Jersey, households earning less than 200% of the federal poverty level may qualify for exemptions from the state’s individual mandate penalty.

Comparatively, tax penalties for non-compliance vary widely across regions, reflecting differing healthcare policies and priorities. In Switzerland, for instance, residents are required to purchase private health insurance, and failure to do so can result in fines and automatic enrollment in a plan, with the government covering the cost if necessary. This contrasts with the U.S. approach, where penalties are primarily financial and enforced through tax filings. Regardless of the region, the takeaway is clear: staying informed about local laws and proactively managing your insurance status can save you from unnecessary fines and ensure continuous access to healthcare.

Does Healthy Kids Offer Adult Health Insurance Coverage? Explained

You may want to see also

Explore related products

![]()

Waiting Periods: Face waiting periods for new policies, delaying access to healthcare services

Failing to renew your health insurance can trigger a waiting period if you decide to purchase a new policy later. This delay, often imposed by insurers to mitigate risk, means you won’t have immediate access to certain healthcare services, even after paying premiums. For example, pre-existing conditions might require a 12- to 36-month waiting period before coverage kicks in, leaving you financially vulnerable during that time. Maternity care often has a 9- to 12-month waiting period, which can disrupt family planning if you’re uninsured during the gap. Understanding these specifics is crucial for avoiding unexpected healthcare costs.

Consider the scenario of a 35-year-old individual who lets their insurance lapse for six months due to job loss. When they finally secure a new policy, they might face a 24-month waiting period for coverage of chronic conditions like diabetes or hypertension. During this time, routine check-ups, medications, and specialist visits would be out-of-pocket expenses, potentially totaling thousands of dollars. Even preventive services, such as vaccinations or cancer screenings, may not be covered until the waiting period ends, increasing the risk of undetected health issues. This financial and health burden underscores the importance of maintaining continuous coverage.

To mitigate the impact of waiting periods, take proactive steps if you anticipate a gap in insurance. First, explore short-term health plans, which typically have shorter waiting periods but limited coverage. Second, negotiate with your current insurer for a grace period or extension if you’re unable to renew immediately. Third, utilize community health clinics or government programs like Medicaid, which often have no waiting periods for eligible individuals. Finally, maintain a health savings account (HSA) to cover unexpected medical expenses during the waiting period. These strategies can provide a safety net while you transition to a new policy.

Comparing waiting periods across different insurers reveals significant variations. For instance, some policies may waive waiting periods for pre-existing conditions if you’ve maintained continuous coverage for at least 90 days prior to switching plans. Others might reduce the waiting period for maternity care if you’ve had a previous policy with similar benefits. Researching these details before letting your insurance lapse can help you choose a new plan with more favorable terms. Additionally, consulting a licensed insurance broker can provide tailored advice based on your health history and financial situation.

In conclusion, waiting periods are a hidden cost of letting health insurance lapse, delaying access to essential healthcare services and increasing financial risk. By understanding the specifics of these periods and taking proactive measures, you can minimize their impact and ensure continuous care. Whether through short-term plans, negotiating with insurers, or leveraging government programs, staying informed and prepared is key to navigating this challenge effectively.

Understanding Short-Term Medical Insurance Coverage Options

You may want to see also

![]()

Out-of-Pocket Costs: Full responsibility for medical bills without insurance coverage or subsidies

Failing to renew your health insurance shifts the entire financial burden of medical care onto your shoulders. Without the safety net of insurance or subsidies, every doctor’s visit, prescription, and procedure becomes your sole responsibility. This means paying full price for services that insurance companies typically negotiate down to a fraction of the cost. For instance, a routine checkup that might cost an insured individual $25 could soar to $200 or more without coverage. Multiply this by more complex needs—like emergency room visits, surgeries, or chronic condition management—and the costs escalate rapidly.

Consider the scenario of a 35-year-old with no insurance who breaks their arm. The average cost of an emergency room visit for a fracture is around $2,500, not including X-rays, casting, or follow-up care. Without insurance, they’re on the hook for the entire bill. Prescription medications add another layer of expense. For example, a month’s supply of insulin can cost upwards of $300 without insurance, a price many cannot sustain long-term. These examples illustrate how quickly out-of-pocket costs can spiral out of control, turning manageable health issues into financial crises.

To mitigate these risks, it’s crucial to understand your options. If you’ve lost insurance, explore alternatives like short-term health plans, which offer limited coverage for emergencies, or community health clinics that provide services on a sliding scale based on income. For prescriptions, discount programs like GoodRx can reduce costs significantly—a lifesaver for those managing chronic conditions. Additionally, maintaining a health savings account (HSA) can provide a financial cushion for unexpected medical expenses, though contributions must be made while insured.

The psychological toll of forgoing insurance cannot be overlooked. The stress of avoiding necessary care due to cost can exacerbate health issues, creating a vicious cycle. A study by the Kaiser Family Foundation found that uninsured individuals are more likely to delay or skip care altogether, leading to poorer health outcomes. This highlights the importance of viewing insurance not just as a financial tool but as a safeguard for your overall well-being.

In conclusion, letting health insurance lapse means accepting full responsibility for medical bills, often at inflated rates. The financial and health consequences can be severe, but proactive steps—like exploring alternative coverage options and utilizing discount programs—can help manage the risks. While it may seem tempting to save on premiums, the potential costs of going uninsured far outweigh the temporary relief. Prioritizing continuous coverage is not just a financial decision but a critical investment in your long-term health.

Medical Insurance Cards: Progressive's Requirements and Your Privacy

You may want to see also

Frequently asked questions

If you don’t renew your health insurance on time, your coverage will lapse, leaving you uninsured. This means you’ll be responsible for paying all medical expenses out of pocket until you secure new coverage.

Yes, you can still receive medical treatment, but without insurance, you’ll have to pay the full cost of services, which can be significantly higher than insured rates.

In some regions, like the U.S., there is no federal penalty for not having health insurance, but some states may impose penalties. Additionally, you’ll lose access to preventive care and financial protection against high medical costs.

It depends on the insurer and policy. Some insurers may allow late renewals with a grace period, but others may require you to apply for a new policy, which could involve waiting periods or higher premiums.