Health insurance is a critical component of financial and personal well-being, providing individuals and families with protection against the high costs of medical care. However, understanding the concept of a health insurance root can be confusing, as it is not a standard term in the industry. Typically, the foundation or root of health insurance lies in its core purpose: to offer coverage for medical expenses, including doctor visits, hospital stays, prescription medications, and preventive care. This foundational aspect ensures that policyholders can access necessary healthcare services without facing overwhelming financial burdens. To fully grasp the benefits and limitations of health insurance, it is essential to explore its key components, such as premiums, deductibles, copayments, and coverage networks, which collectively form the root of its functionality and value.

Explore related products

What You'll Learn

- Coverage Limits: Understand maximum payouts for treatments, procedures, and medications under your policy terms

- Premiums & Deductibles: Monthly costs and out-of-pocket expenses before insurance coverage begins

- Network Providers: In-network vs. out-of-network doctors, hospitals, and specialists for cost efficiency

- Excluded Services: Treatments, conditions, or procedures not covered by your insurance plan

- Claim Process: Steps to file claims, required documentation, and timelines for reimbursement

![]()

Coverage Limits: Understand maximum payouts for treatments, procedures, and medications under your policy terms

Health insurance policies often come with coverage limits, which dictate the maximum amount your insurer will pay for specific treatments, procedures, or medications. These limits can vary widely depending on the policy, provider, and even the state you live in. For instance, a policy might cover up to $500,000 for a major surgery but cap prescription drug coverage at $5,000 annually. Understanding these limits is crucial because exceeding them can leave you with unexpected out-of-pocket expenses. Always review your policy’s Summary of Benefits and Coverage (SBC) to identify these thresholds and plan accordingly.

Consider a scenario where a 45-year-old individual requires a knee replacement surgery, which typically costs around $50,000. If their policy has a $30,000 coverage limit for orthopedic procedures, they’ll be responsible for the remaining $20,000. Similarly, medications like insulin or specialty drugs for chronic conditions can quickly hit annual caps, forcing patients to pay full price afterward. To avoid such surprises, compare policies during open enrollment, focusing on limits for services you’re likely to need. Some insurers offer supplemental plans to extend coverage, though these come with additional premiums.

Analyzing coverage limits requires a proactive approach. Start by listing your anticipated medical needs for the year, including prescriptions, specialist visits, or ongoing treatments. Cross-reference this list with your policy’s limits to identify potential gaps. For example, if you take a brand-name medication with a $3,000 annual cap but your yearly cost is $4,500, explore alternatives like generic options or patient assistance programs. Additionally, some policies have separate limits for in-network vs. out-of-network care, with out-of-network services often having lower caps or no coverage at all.

Persuasively, it’s worth noting that coverage limits aren’t just about big-ticket items like surgeries. Even routine care can be affected. For instance, physical therapy sessions might be limited to 20 visits per year, or mental health counseling could be capped at 10 sessions annually. These restrictions can hinder long-term treatment plans, especially for chronic conditions. Advocate for yourself by discussing limits with your healthcare provider and insurer. Sometimes, medical necessity appeals can override caps if your doctor documents the need for additional care.

Finally, a comparative look at policies reveals that high-deductible health plans (HDHPs) often have lower coverage limits for certain services but pair them with health savings accounts (HSAs) to offset costs. Conversely, comprehensive plans may have higher limits but come with steeper premiums. Evaluate your financial situation and health needs to determine which trade-off works best. For families, consider policies with aggregate limits, which combine individual and family caps, providing more flexibility. Understanding these nuances ensures you’re not just insured, but adequately protected.

Vaping vs. Tobacco: Health Insurance Implications and Coverage Differences

You may want to see also

Explore related products

![]()

Premiums & Deductibles: Monthly costs and out-of-pocket expenses before insurance coverage begins

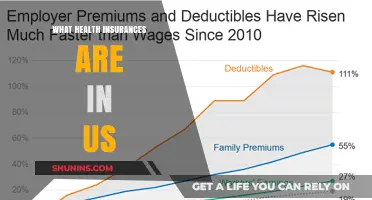

Health insurance premiums are the monthly or annual fees you pay to maintain coverage, regardless of whether you use medical services. Think of them as a subscription to financial protection against high healthcare costs. For instance, a 30-year-old nonsmoker might pay $300 monthly for a mid-tier plan, while a family of four could face premiums exceeding $1,200. Premiums vary based on factors like age, location, plan type, and provider network. Lower premiums often come with higher deductibles, a trade-off that shifts more upfront costs to the policyholder.

Deductibles, on the other hand, are the out-of-pocket expenses you must pay before insurance coverage kicks in. For example, if your plan has a $2,000 deductible, you’ll cover the first $2,000 of medical costs annually before insurance starts paying its share. High-deductible plans (HDHPs), like those paired with Health Savings Accounts (HSAs), often have deductibles of $1,500 or more for individuals and $3,000+ for families. These plans appeal to those who rarely need medical care but want protection against catastrophic expenses. However, they can be risky if unexpected medical needs arise, as you’re responsible for the full deductible before coverage applies.

The interplay between premiums and deductibles requires strategic planning. For instance, a young, healthy individual might opt for a high-deductible plan with lower monthly premiums, saving money if they rarely visit the doctor. Conversely, someone with chronic conditions or frequent medical needs may prefer a low-deductible plan with higher premiums to minimize out-of-pocket costs. Employers often subsidize premiums for group plans, reducing employee expenses but sometimes limiting plan choices. Understanding this balance is crucial for aligning your budget with your healthcare needs.

Practical tips can help navigate these costs. First, review your annual medical expenses to determine whether a high- or low-deductible plan suits your usage patterns. Second, consider pairing a high-deductible plan with an HSA to save pre-tax dollars for medical expenses. Third, compare plans during open enrollment, as premiums and deductibles can change annually. Finally, don’t overlook additional costs like copays and coinsurance, which further impact your total out-of-pocket spending. By analyzing these components, you can select a plan that minimizes financial strain while providing adequate coverage.

In summary, premiums and deductibles are foundational elements of health insurance, each representing distinct financial commitments. Premiums ensure ongoing coverage, while deductibles dictate how much you pay before insurance takes effect. Balancing these costs requires assessing your health needs, budget, and risk tolerance. With careful consideration, you can choose a plan that offers both affordability and protection, ensuring you’re prepared for whatever healthcare challenges arise.

Getting Medical Insurance for Your Newborn: What You Need to Know

You may want to see also

Explore related products

![]()

Network Providers: In-network vs. out-of-network doctors, hospitals, and specialists for cost efficiency

Choosing healthcare providers within your insurance network can significantly reduce out-of-pocket costs. Insurance companies negotiate discounted rates with in-network doctors, hospitals, and specialists, passing those savings onto policyholders. For example, a routine office visit might cost $150 out-of-network but only $50 in-network after the negotiated rate is applied. This price difference extends to procedures, prescriptions, and hospitalizations, making in-network care a financially prudent choice for most insured individuals.

However, relying solely on in-network providers isn’t always feasible. Specialized treatments, rare conditions, or geographic limitations may require seeking out-of-network care. In such cases, costs can escalate quickly. Out-of-network providers bill at their standard rates, and insurance typically covers a smaller portion—or none at all—leaving you responsible for the balance. For instance, a $5,000 out-of-network surgery might result in a $2,000 out-of-pocket expense, even with insurance, compared to $500 for the same procedure in-network.

To navigate this dilemma, review your insurance plan’s out-of-network coverage policy carefully. Some plans offer partial coverage for out-of-network services after meeting a higher deductible, while others exclude them entirely. If out-of-network care is unavoidable, request a cost estimate upfront and verify coverage with your insurer. Additionally, consider appealing denied claims or negotiating directly with providers for reduced rates, especially for high-cost procedures.

For those with chronic conditions or complex medical needs, balancing cost efficiency and access to specialized care is critical. Hybrid plans, which offer both in- and out-of-network benefits, provide flexibility but often come with higher premiums. Alternatively, supplementing a basic plan with a health savings account (HSA) can offset out-of-network expenses. Ultimately, understanding your network options and planning for exceptions ensures you maximize insurance benefits while minimizing financial strain.

HIPAA's Role in Shaping Health Insurance and Reimbursement Processes

You may want to see also

Explore related products

![]()

Excluded Services: Treatments, conditions, or procedures not covered by your insurance plan

Health insurance policies often come with a list of excluded services, which can leave policyholders unexpectedly responsible for significant costs. Understanding these exclusions is crucial for anyone navigating the complexities of healthcare coverage. For instance, many plans exclude cosmetic procedures, such as elective rhinoplasty or Botox injections, unless they are deemed medically necessary. Similarly, experimental treatments, like certain gene therapies or unapproved stem cell procedures, are frequently not covered. Even some preventive services, like genetic testing for conditions without immediate clinical implications, may fall outside the scope of your plan. Knowing these limitations can help you avoid financial surprises and plan for out-of-pocket expenses.

Analyzing the rationale behind excluded services reveals a balance between cost management and medical necessity. Insurers often exclude treatments with limited scientific evidence or those considered lifestyle enhancements rather than essential care. For example, fertility treatments like in vitro fertilization (IVF) are excluded in many basic plans, despite their potential life-changing impact. Similarly, long-term care for chronic conditions, such as physical therapy beyond a certain number of sessions (e.g., 20 visits per year), may not be fully covered. This approach allows insurers to keep premiums lower but places the burden on individuals to assess their needs and consider supplemental coverage if necessary.

To navigate excluded services effectively, start by thoroughly reviewing your policy’s Summary of Benefits and Coverage (SBC). Look for specific terms like “not covered,” “excluded,” or “limited coverage.” For example, mental health services might be covered, but only for certain diagnoses or treatment modalities. If you anticipate needing a service that’s excluded, explore alternative funding options, such as health savings accounts (HSAs) or payment plans offered by healthcare providers. Additionally, consider appealing an exclusion if you believe the treatment is medically necessary—some insurers may reconsider their decision with supporting documentation from your healthcare provider.

Comparing excluded services across different plans can highlight significant variations in coverage. For instance, one insurer might exclude bariatric surgery entirely, while another may cover it for individuals with a BMI over 40 and comorbid conditions like diabetes. Similarly, maternity care, including prenatal visits and delivery, is excluded in some short-term health plans but required in comprehensive ACA-compliant policies. When shopping for insurance, use these exclusions as a benchmark to determine which plan aligns best with your health needs and financial situation.

Finally, excluded services often reflect broader trends in healthcare and insurance priorities. As medical technology advances, new treatments may initially fall into the excluded category until their efficacy and cost-effectiveness are widely accepted. For example, telehealth services were once rarely covered but have become more standard in recent years. Staying informed about policy updates and advocating for coverage expansions can help bridge gaps in care. By understanding and proactively addressing excluded services, you can make more informed decisions and minimize the risk of unexpected medical debt.

Malpractice Claims: Can You Sue Without Insurance Coverage?

You may want to see also

Explore related products

![]()

Claim Process: Steps to file claims, required documentation, and timelines for reimbursement

Filing a health insurance claim can feel like navigating a maze, but understanding the process transforms it from daunting to manageable. The first step is always to notify your insurer promptly after receiving medical care. Most plans require you to submit a claim within 90 days of the service date, though some may allow up to a year. Missing this window could mean forfeiting reimbursement entirely. Start by contacting your insurance provider to confirm the exact timeline and any pre-authorization requirements for the treatment received.

Next, gather the necessary documentation, which typically includes the itemized bill from the healthcare provider, a completed claim form, and proof of service such as a doctor’s note or lab results. For prescriptions, include the pharmacy receipt and, if applicable, the prescription itself. Some insurers also require a referral or prior authorization form for specialist visits or procedures. Double-check your policy’s specifics—for instance, certain plans mandate additional forms for out-of-network providers or emergency room visits. Incomplete submissions are a common reason for delays, so meticulousness pays off.

Once your paperwork is in order, submit it through the insurer’s preferred method, whether online, via mail, or through a mobile app. Keep copies of everything for your records, and note the date of submission. If filing digitally, take screenshots as proof. After submission, the waiting game begins. Reimbursement timelines vary widely: some insurers process claims within 15 days, while others may take up to 45 days, depending on the complexity of the case. Federal law requires insurers to process claims within 30 days for electronic submissions and 45 days for paper submissions, but many companies aim for quicker turnarounds to maintain customer satisfaction.

Finally, stay proactive. If your claim is denied, don’t assume it’s the final word. Review the explanation of benefits (EOB) to understand the reason for denial. Common issues include missing documentation, ineligible services, or billing errors. You have the right to appeal, and many denials are overturned upon review. Keep detailed records of all communications with your insurer, including dates, names, and summaries of conversations. Persistence and organization are your allies in ensuring you receive the coverage you’re entitled to.

Medicare vs. Medical Insurance: What's the Difference?

You may want to see also

Frequently asked questions

A health insurance root refers to the foundational or base plan of a health insurance policy, which typically covers essential health services and acts as the starting point for additional coverage options.

A health insurance root usually covers basic medical services such as doctor visits, hospitalization, emergency care, and preventive care, but may exclude specialized treatments or additional benefits.

Yes, most health insurance roots allow policyholders to customize their coverage by adding optional benefits like dental, vision, prescription drugs, or mental health services for an additional cost.