Understanding what income counts for health insurance is crucial for determining eligibility and calculating premiums, especially under programs like the Affordable Care Act (ACA). Generally, the income considered includes wages, salaries, tips, self-employment earnings, unemployment compensation, and Social Security benefits, among other sources. For individuals and families applying for subsidies or Medicaid, Modified Adjusted Gross Income (MAGI) is typically used, which adjusts gross income for certain deductions. Excluded income sources, such as gifts, inheritances, or certain tax-exempt interest, are not factored into these calculations. Accurately reporting all relevant income ensures compliance with regulations and helps secure appropriate coverage at the right cost.

| Characteristics | Values |

|---|---|

| Modified Adjusted Gross Income (MAGI) | Primary income metric used to determine eligibility for health insurance subsidies. |

| Included Income Sources | Wages, salaries, tips, self-employment income, unemployment compensation, Social Security benefits, pensions, and investment income. |

| Excluded Income Sources | Certain Social Security benefits, child support payments, gifts, and inheritances. |

| Household Size Consideration | MAGI is calculated based on the total income of all household members, including dependents. |

| Poverty Level Threshold | Eligibility for Medicaid or Marketplace subsidies is often based on income as a percentage of the Federal Poverty Level (FPL). |

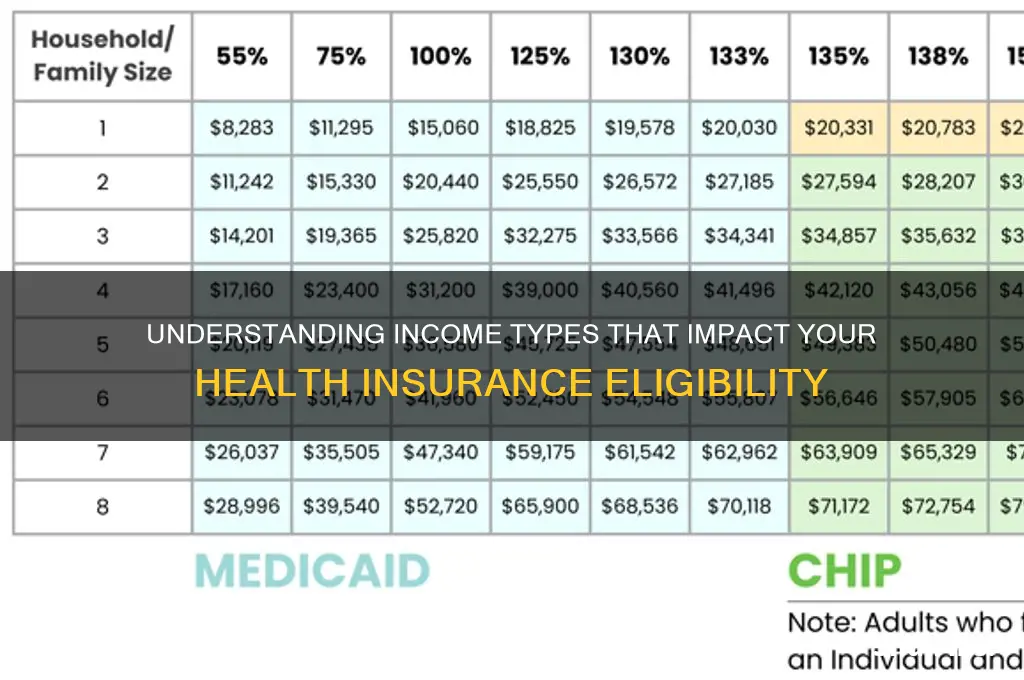

| 2023 Federal Poverty Level (FPL) | Varies by household size; e.g., $14,580 for an individual, $30,000 for a family of four. |

| Medicaid Eligibility | Typically up to 138% of FPL in states that expanded Medicaid under the ACA. |

| Marketplace Subsidies Eligibility | 100%–400% of FPL for premium tax credits; cost-sharing reductions up to 250% of FPL. |

| Taxable vs. Nontaxable Income | Both taxable and nontaxable income are generally included in MAGI calculations. |

| Foreign Income | Foreign-earned income may be included if it is taxable in the U.S. |

| Capital Gains | Included in MAGI if reported on tax returns. |

| Alimony | Included in MAGI for the recipient (as of 2019 tax law changes). |

| Retirement Account Withdrawals | Taxable withdrawals are included in MAGI. |

| Self-Employment Deductions | Deductions for self-employment taxes and business expenses are considered. |

| Updated Annually | Income limits and FPL thresholds are updated annually by the federal government. |

Explore related products

What You'll Learn

- Taxable Income: Wages, salaries, tips, and other taxable earnings count towards health insurance eligibility

- Self-Employment Income: Net profit from self-employment is included in income calculations

- Investment Income: Dividends, interest, and capital gains may factor into health insurance assessments

- Retirement Income: Pension, Social Security, and retirement account distributions can count as income

- Non-Taxable Income: Some non-taxable sources, like child support, may still be considered

![]()

Taxable Income: Wages, salaries, tips, and other taxable earnings count towards health insurance eligibility

Understanding which income counts for health insurance is crucial for accurately assessing your eligibility and potential subsidies. Taxable income, including wages, salaries, tips, and other earnings subject to federal income tax, plays a central role in this calculation. These figures are reported on your tax return and directly influence your Modified Adjusted Gross Income (MAGI), the metric used by the Affordable Care Act (ACA) to determine eligibility for premium tax credits and Medicaid. For instance, if your annual salary is $40,000, this amount, minus certain deductions, will be factored into your MAGI, potentially qualifying you for reduced premiums on the health insurance marketplace.

When calculating taxable income for health insurance purposes, it’s essential to include all sources of earned income. Tips, whether reported to an employer or not, must be accounted for, as they are considered taxable earnings. Similarly, freelance or contract work income, reported on a 1099 form, is also included. For example, a waiter earning $30,000 in wages and $10,000 in tips would have a total taxable income of $40,000, which would be used to determine their health insurance eligibility. Failing to report all taxable income can lead to incorrect subsidy calculations, resulting in unexpected costs or penalties.

One common misconception is that only full-time employment income counts toward health insurance eligibility. However, part-time wages, seasonal earnings, and even gig economy income are all taxable and therefore relevant. For instance, a college student working part-time earning $15,000 annually and driving for a ride-sharing service earning an additional $5,000 would have a total taxable income of $20,000. This combined income could make them eligible for Medicaid or subsidized marketplace plans, depending on their state’s income thresholds.

Practical tip: Keep detailed records of all income sources throughout the year, including tips, bonuses, and side hustle earnings. Use tax software or consult a tax professional to ensure accurate reporting, as this directly impacts your health insurance options. For example, if you’re self-employed, track your net profit (income minus business expenses) as this will be your taxable income. Understanding these nuances ensures you maximize available benefits while avoiding compliance issues.

In conclusion, taxable income—encompassing wages, salaries, tips, and other earnings—is the cornerstone of health insurance eligibility calculations. By accurately reporting all taxable income, individuals can ensure they receive the appropriate subsidies or qualify for Medicaid, making health coverage more affordable. Whether you’re a full-time employee, part-time worker, or freelancer, every dollar of taxable income matters in determining your health insurance options.

Health Insurance After Termination: What Happens When You're Let Go?

You may want to see also

Explore related products

![]()

Self-Employment Income: Net profit from self-employment is included in income calculations

Self-employed individuals often face unique challenges when navigating health insurance options, particularly in understanding how their income is assessed. Unlike traditional employees with a steady paycheck, self-employed workers must report their net profit—not gross revenue—as the basis for income calculations. This distinction is critical because it directly impacts eligibility for subsidies, Medicaid, or marketplace plans under the Affordable Care Act (ACA). For instance, if a freelancer earns $80,000 in gross revenue but has $30,000 in business expenses, only the $50,000 net profit is considered for health insurance purposes.

Calculating net profit requires meticulous record-keeping. Start by tracking all business income and deductible expenses, such as office supplies, travel, or home office costs. Use IRS Schedule C to determine your net profit, which is then reported on your tax return. This figure becomes the foundation for health insurance applications. A common mistake is overestimating income by using gross revenue, which can lead to paying higher premiums or missing out on subsidies. For example, a self-employed graphic designer with $60,000 in gross income and $20,000 in expenses might qualify for a premium tax credit based on their $40,000 net profit, significantly reducing their health insurance costs.

Fluctuating income is another challenge for self-employed individuals. If your earnings vary year-to-year, estimate your current-year net profit as accurately as possible when applying for coverage. The ACA allows for adjustments later if your income changes significantly. For instance, if you project a $45,000 net profit but end up earning $55,000, you may need to repay some subsidies at tax time. Conversely, if your income drops, you could qualify for additional assistance mid-year. Tools like the Healthcare.gov subsidy calculator can help estimate your eligibility based on projected net profit.

One practical tip is to consult a tax professional or use accounting software to streamline income tracking. Programs like QuickBooks or FreshBooks can categorize expenses and calculate net profit automatically, reducing errors. Additionally, consider setting aside a portion of your gross income for taxes and health insurance premiums to avoid financial strain. For example, allocating 20–30% of each payment for taxes and insurance can provide a buffer for unexpected costs.

In conclusion, self-employed individuals must focus on net profit, not gross revenue, when determining their income for health insurance purposes. Accurate record-keeping, careful estimation of annual earnings, and leveraging tools or professional advice can ensure compliance and optimize benefits. By understanding this key distinction, self-employed workers can navigate the health insurance landscape more confidently and affordably.

Who is RLI Insurance Company? A Comprehensive Overview and Guide

You may want to see also

Explore related products

![]()

Investment Income: Dividends, interest, and capital gains may factor into health insurance assessments

Investment income, including dividends, interest, and capital gains, can significantly impact your health insurance assessments, particularly when determining eligibility for subsidized plans or Medicaid. Unlike earned income from wages or salaries, investment income is often considered part of your modified adjusted gross income (MAGI), which is a key factor in calculating premiums and subsidies under the Affordable Care Act (ACA). For instance, if you receive $5,000 in dividends from stocks and $3,000 in interest from bonds, these amounts are added to your MAGI, potentially pushing you into a higher income bracket and reducing your subsidy eligibility. Understanding how these income sources are treated is crucial for accurate financial planning and avoiding unexpected healthcare costs.

When assessing your health insurance options, it’s essential to differentiate between taxable and tax-exempt investment income. Taxable dividends, interest, and capital gains are typically included in your MAGI, while tax-exempt interest (e.g., from municipal bonds) is generally excluded. For example, if you have $10,000 in taxable interest and $2,000 in tax-exempt interest, only the $10,000 will affect your health insurance calculations. This distinction can make a substantial difference, especially for retirees or individuals relying heavily on investment income. Pro tip: Consult a tax advisor to ensure you’re accurately reporting these income types and maximizing your subsidy potential.

Capital gains, whether short-term or long-term, are another critical component of investment income that insurers consider. Short-term capital gains (from assets held for one year or less) are taxed as ordinary income and fully included in your MAGI. Long-term capital gains, however, may be taxed at a lower rate but are still factored into your income for health insurance purposes. For example, selling stocks for a $15,000 long-term gain could increase your MAGI, potentially disqualifying you from premium tax credits. To mitigate this, consider strategic timing of asset sales or explore tax-advantaged accounts like IRAs or 401(k)s, which can shield investment income from immediate tax and MAGI calculations.

For individuals nearing retirement or already retired, investment income often becomes the primary source of funds, making it a central factor in health insurance assessments. Retirees aged 65 and older may qualify for Medicare, but those under 65 must navigate ACA marketplace plans, where investment income plays a pivotal role. For example, a retired couple with $60,000 in annual dividends and interest might find themselves ineligible for subsidies if their MAGI exceeds 400% of the federal poverty level. Practical advice: Diversify your income sources and consider Roth conversions to reduce future taxable income, which can help maintain subsidy eligibility as you age.

Finally, understanding the interplay between investment income and health insurance requires proactive financial management. Regularly review your investment portfolio and projected income to anticipate how dividends, interest, and capital gains will affect your MAGI. Tools like online MAGI calculators can provide estimates, but consulting a financial planner or insurance broker can offer tailored strategies. For instance, if you’re approaching a year with significant capital gains, you might delay asset sales or offset gains with losses to manage your income level. By staying informed and strategic, you can optimize your health insurance costs while maximizing your investment returns.

Exploring New Mexico's Health Insurance Options: Plans, Coverage, and Benefits

You may want to see also

Explore related products

![]()

Retirement Income: Pension, Social Security, and retirement account distributions can count as income

Retirement income, including pensions, Social Security benefits, and distributions from retirement accounts like 401(k)s or IRAs, is often considered taxable income by the IRS. This classification directly impacts how health insurance premiums are calculated, particularly for Medicare and Affordable Care Act (ACA) plans. For instance, if your modified adjusted gross income (MAGI) exceeds certain thresholds, you may pay higher premiums for Medicare Part B and Part D. Understanding which retirement income sources count can help you plan withdrawals strategically to minimize costs.

Consider this scenario: A 67-year-old retiree collects a $30,000 annual pension, $20,000 in Social Security benefits, and withdraws $15,000 from their IRA. All $65,000 is taxable and factored into their MAGI. If this MAGI pushes them into a higher income bracket, their Medicare premiums could increase significantly. For 2023, individuals with a MAGI above $97,000 and couples above $194,000 pay surcharges for Part B and Part D. Knowing this, the retiree might delay IRA withdrawals or use Roth accounts (tax-free distributions) to manage their taxable income.

Strategic planning is key. For ACA plans, retirement income also counts toward MAGI, determining eligibility for premium tax credits. If your MAGI falls between 100% and 400% of the federal poverty level, you may qualify for subsidies. For example, a single retiree with a MAGI of $54,360 in 2023 (400% of the poverty level) could receive substantial assistance. However, exceeding this threshold means paying full price for premiums. Retirees should estimate their total income, including all retirement sources, before enrolling in a plan.

One practical tip is to coordinate withdrawals from taxable and tax-free accounts. For instance, pair taxable pension income with tax-free Roth IRA distributions to lower your overall MAGI. Another strategy is to time capital gains or large withdrawals in years when your income is naturally lower. Consulting a financial advisor can help align your retirement income strategy with healthcare costs, ensuring you maximize benefits while minimizing expenses.

In summary, retirement income is not exempt from health insurance calculations. Pensions, Social Security, and retirement account distributions all contribute to your MAGI, influencing Medicare premiums and ACA subsidies. By understanding these rules and planning withdrawals carefully, retirees can avoid unexpected surcharges and optimize their healthcare spending.

Does Insurance Cover Slashed Tires? Understanding Your Policy's Limits

You may want to see also

Explore related products

![]()

Non-Taxable Income: Some non-taxable sources, like child support, may still be considered

Non-taxable income often slips under the radar when calculating eligibility for health insurance, yet it can significantly impact your coverage options. While sources like child support, gifts, or certain disability benefits aren’t taxed, they may still count toward your household income for health insurance purposes. This discrepancy arises because health insurance programs, such as Medicaid or Affordable Care Act (ACA) subsidies, use Modified Adjusted Gross Income (MAGI) as their benchmark, which includes some non-taxable income. Understanding this distinction is crucial to avoid underestimating your income and risking ineligibility or overpayment.

Consider child support, a prime example of non-taxable income that’s often factored into health insurance calculations. For instance, if you receive $500 monthly in child support, this amount could increase your MAGI, potentially affecting your eligibility for premium tax credits or Medicaid. Similarly, tax-exempt interest from municipal bonds or certain veterans’ benefits might also be included. To navigate this, gather all income documentation, including non-taxable sources, and consult the specific rules of the health insurance program you’re applying for. Tools like the Healthcare.gov income calculator can help estimate your MAGI accurately.

The inclusion of non-taxable income isn’t arbitrary; it’s designed to ensure fairness in determining financial need. For example, a single parent earning $30,000 annually with $12,000 in child support might appear low-income based on taxable earnings alone. However, their total household resources are $42,000, which could disqualify them from certain subsidies. Conversely, failing to report such income could lead to penalties or repayment of excess credits. Transparency is key—report all income sources, even if they’re non-taxable, to avoid complications.

Practical steps can simplify this process. First, categorize your income into taxable and non-taxable streams. Second, review the MAGI guidelines for your health insurance program, as rules vary by state and plan. Third, use official calculators or consult a certified application counselor to ensure accuracy. For instance, if you’re applying for ACA subsidies, include child support, worker’s compensation, and tax-exempt interest in your calculations. Finally, keep detailed records of all income sources to support your application and resolve any discrepancies swiftly.

In conclusion, non-taxable income isn’t a free pass when it comes to health insurance eligibility. By understanding which sources count and how they’re factored into MAGI, you can make informed decisions and secure the coverage you need. Treat non-taxable income with the same diligence as taxable earnings, and you’ll avoid pitfalls that could jeopardize your access to affordable healthcare.

Did Health Insurance Cover Jazz's Surgery? Unraveling the Facts

You may want to see also

Frequently asked questions

No, only your modified adjusted gross income (MAGI) is used to determine eligibility for health insurance subsidies. This includes wages, salaries, tips, self-employment income, and other taxable income, but excludes certain deductions and exemptions.

It depends. Social Security income, including retirement and disability benefits, is generally not counted as part of your MAGI for health insurance purposes, unless it is taxable. If your Social Security benefits are taxable, the taxable portion may be included in your MAGI.

Yes, unemployment compensation is considered taxable income and is included in your MAGI when determining eligibility for health insurance subsidies or programs like Medicaid. Be sure to report it accurately on your application.

![Magi Adventure of Sinbad COMPLETE BOX (Limited Edition) [Blu-ray] JAPANESE EDITION](https://m.media-amazon.com/images/I/71oJ3zSScuL._AC_UY218_.jpg)