When determining eligibility for marketplace health insurance, the income considered is typically the modified adjusted gross income (MAGI) of the applicant and their household. MAGI is derived from the adjusted gross income (AGI) reported on federal tax returns, with certain adjustments added back in. This figure is used to calculate whether an individual or family qualifies for premium tax credits or cost-sharing reductions. Key factors include household size, income limits based on the federal poverty level (FPL), and the specific rules of the Affordable Care Act (ACA). Understanding which income sources are included—such as wages, self-employment earnings, and certain benefits—is crucial for accurately estimating eligibility and potential subsidies.

| Characteristics | Values |

|---|---|

| Income Range for Subsidies | 100% - 400% of the Federal Poverty Level (FPL) |

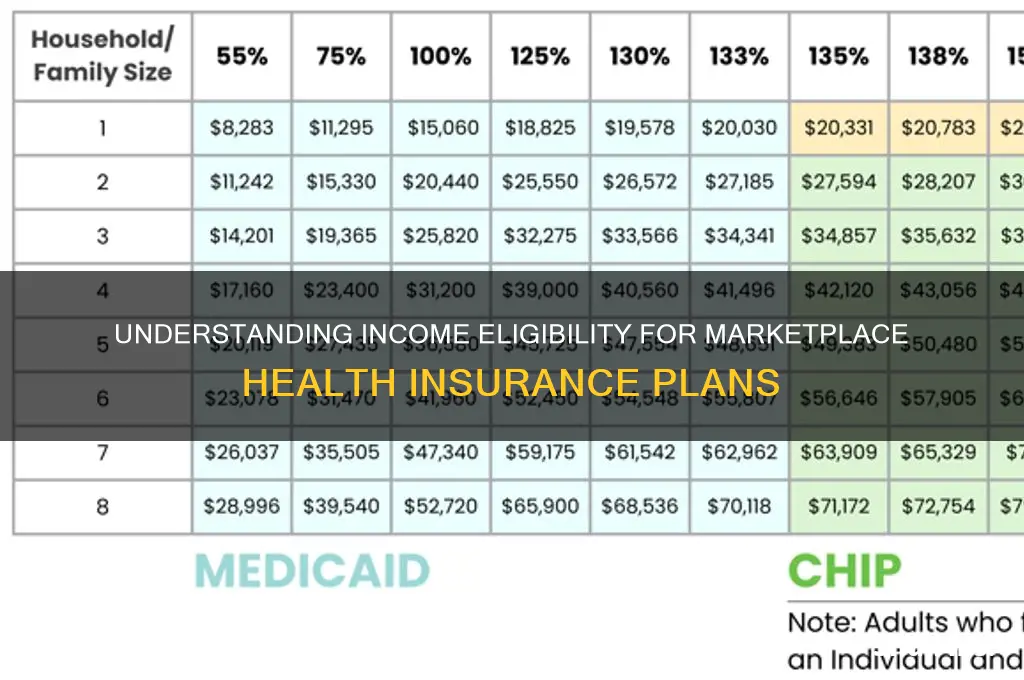

| 2023 FPL for a Single Individual | $14,580 annually |

| 2023 FPL for a Family of Four | $30,000 annually |

| Lower Income Limit (100% FPL) | $14,580 for a single individual; varies by family size |

| Upper Income Limit (400% FPL) | $58,320 for a single individual; $120,000 for a family of four |

| Premium Tax Credits Eligibility | Available for incomes between 100% and 400% FPL |

| Cost-Sharing Reductions (CSRs) | Available for incomes between 100% and 250% FPL |

| Medicaid Eligibility | Typically up to 138% FPL in states that expanded Medicaid |

| Income Calculation | Based on Modified Adjusted Gross Income (MAGI) |

| Annual Updates | FPL and income thresholds are updated annually by the federal government |

| Special Considerations | Certain deductions and expenses may adjust MAGI for eligibility |

Explore related products

What You'll Learn

- Household Income Calculation: Includes wages, salaries, tips, self-employment earnings, and other taxable income sources

- Modified Adjusted Gross Income (MAGI): Used to determine eligibility for premium tax credits

- Excludable Income Types: Certain benefits like SSI, child support, or foster care payments are excluded

- Projected Annual Income: Estimated income for the upcoming year affects subsidy eligibility

- Income Verification Process: Requires documentation like tax returns, pay stubs, or employer letters

![]()

Household Income Calculation: Includes wages, salaries, tips, self-employment earnings, and other taxable income sources

Understanding how household income is calculated for marketplace health insurance is crucial for accurate premium tax credit determination. The process involves more than just adding up paychecks; it encompasses a broad spectrum of income sources. Wages, salaries, and tips from employment form the foundation, but self-employment earnings and other taxable income, such as rental income or investment dividends, are equally vital components. This comprehensive approach ensures that the financial picture used to assess eligibility and subsidies reflects the true economic status of the household.

For self-employed individuals, calculating income requires a nuanced approach. Net profit from self-employment, derived from business revenue minus allowable deductions, is the figure considered. This means meticulous record-keeping is essential, as both income and expenses must be accurately documented. For instance, a freelance graphic designer must account for all client payments received throughout the year, subtracting legitimate business expenses like software subscriptions or equipment purchases. Failure to include all taxable income sources can lead to incorrect subsidy calculations, potentially resulting in repayment of excess credits.

Tips and irregular income sources also play a significant role in household income calculation. For tipped employees, such as restaurant servers, both reported wages and tips must be included. If tips are not fully reported to employers, individuals should still account for them when estimating income for health insurance purposes. Similarly, seasonal or gig workers must consider their annual earnings, even if income fluctuates throughout the year. Estimating annual income based on past trends or projected work can help ensure accuracy in marketplace applications.

One practical tip for households with multiple income streams is to gather all relevant tax documents, such as W-2s, 1099s, and profit/loss statements, before applying for marketplace insurance. This simplifies the process and reduces the risk of errors. Additionally, using the Modified Adjusted Gross Income (MAGI) method, which includes most taxable income sources, provides a standardized way to calculate household income. For families with dependents, understanding how certain deductions or credits might affect MAGI is also important, as it directly impacts subsidy eligibility.

In conclusion, household income calculation for marketplace health insurance is a detailed process that demands attention to all taxable income sources. From wages and self-employment earnings to tips and investment income, every component matters. By carefully accounting for these elements, individuals can ensure they receive the appropriate subsidies and avoid financial surprises. Proactive planning, accurate documentation, and a clear understanding of income inclusion rules are key to navigating this critical aspect of health insurance enrollment.

Tennessee's Medical Insurance Offerings: What You Need to Know

You may want to see also

Explore related products

![]()

Modified Adjusted Gross Income (MAGI): Used to determine eligibility for premium tax credits

Understanding your income is crucial when navigating the complexities of health insurance, especially if you're considering plans through the Health Insurance Marketplace. One key metric that plays a pivotal role in this process is the Modified Adjusted Gross Income (MAGI). This figure is not just a number; it's a gateway to determining your eligibility for premium tax credits, which can significantly reduce your health insurance costs.

Calculating MAGI: A Step-by-Step Guide

To begin, MAGI is derived from your Adjusted Gross Income (AGI), which you report on your federal tax return. However, MAGI goes a step further by including certain tax-exempt income sources that AGI might exclude. Here's a simplified breakdown:

- Start with your AGI: This includes wages, salaries, tips, and other income sources, minus specific deductions like student loan interest and contributions to retirement accounts.

- Add back certain deductions: Include foreign earned income, housing expenses for those living abroad, and any excluded or exempt income from sources like Puerto Rico, American Samoa, Guam, the Commonwealth of the Northern Mariana Islands, or the U.S. Virgin Islands.

- Include tax-exempt interest: This encompasses interest from municipal bonds and other tax-free investments.

For instance, if your AGI is $40,000, and you have $2,000 in tax-exempt interest and $5,000 in foreign earned income, your MAGI would be $47,000.

Why MAGI Matters for Premium Tax Credits

The Affordable Care Act (ACA) uses MAGI to assess your eligibility for premium tax credits, which are subsidies designed to make health insurance more affordable. These credits are available to individuals and families with incomes between 100% and 400% of the Federal Poverty Level (FPL). For 2023, this translates to an annual income range of approximately $13,590 to $54,360 for an individual and $27,750 to $111,000 for a family of four.

Practical Tips for Estimating MAGI

Estimating your MAGI accurately is essential for planning your health insurance budget. Here are some practical tips:

- Keep detailed records: Track all income sources, including tax-exempt interest and foreign earnings, throughout the year.

- Use online calculators: Numerous online tools can help you estimate your MAGI based on your expected income and deductions.

- Consult a tax professional: If your financial situation is complex, consider seeking advice from a tax expert to ensure accuracy.

The Impact of MAGI on Your Health Insurance Options

Your MAGI not only determines your eligibility for premium tax credits but also influences the amount of assistance you receive. Lower MAGI levels generally result in higher subsidies, making health insurance more accessible. For example, a family of four with a MAGI of $30,000 (approximately 110% of FPL) would qualify for more substantial tax credits than a similar family with a MAGI of $100,000 (approximately 365% of FPL).

In summary, Modified Adjusted Gross Income (MAGI) is a critical factor in the health insurance marketplace, particularly for those seeking premium tax credits. By understanding how MAGI is calculated and its implications, you can make informed decisions about your health coverage, ensuring you receive the maximum benefits available to you.

Does Health Insurance Automatically Cover Your Spouse? Key Facts Explained

You may want to see also

Explore related products

![]()

Excludable Income Types: Certain benefits like SSI, child support, or foster care payments are excluded

Not all income is created equal when it comes to calculating eligibility for marketplace health insurance. While most earnings are factored in, certain benefits and payments are specifically excluded from the equation. This means they won't push you over the income threshold for subsidies or Medicaid, potentially saving you money on premiums.

Understanding which income types are excluded is crucial for accurately estimating your costs and finding the best plan.

Let's take Supplemental Security Income (SSI) as an example. This federal program provides monthly payments to individuals with disabilities and limited income. SSI is not considered income for marketplace health insurance purposes. This exclusion recognizes that SSI is meant to meet basic needs and shouldn't penalize recipients by reducing their eligibility for other essential benefits like healthcare. Similarly, child support payments received are excluded. These payments are intended to cover a child's living expenses and shouldn't be factored into the parent's income for insurance purposes.

Foster care payments, another excluded income type, follow the same logic. These payments are meant to support the care of a child in foster care and shouldn't impact the caregiver's eligibility for affordable health insurance.

It's important to note that while these specific benefits are excluded, other government assistance programs might be treated differently. For instance, unemployment benefits are generally considered income for marketplace health insurance calculations. Always consult the official Healthcare.gov website or a qualified navigator for specific guidance on your individual situation.

Knowing which income types are excluded can significantly impact your marketplace health insurance options. By understanding these exclusions, you can ensure you're getting the most accurate cost estimates and accessing the coverage you need.

Adding Your Newborn to Health Insurance: A Marketplace Guide

You may want to see also

Explore related products

![]()

Projected Annual Income: Estimated income for the upcoming year affects subsidy eligibility

Estimating your projected annual income is a critical step when applying for health insurance through the Marketplace, as it directly determines your eligibility for premium tax credits and cost-sharing reductions. Unlike past income, which is a fixed number, projected income requires foresight and accuracy. Overestimating could lead to reduced subsidies, while underestimating might result in unexpected repayments at tax time. For instance, if you anticipate a job change, bonus, or side gig, these must be factored into your estimate to ensure you receive the appropriate financial assistance.

To calculate your projected income, start by reviewing your current earnings, including wages, self-employment income, and any other taxable sources. Next, consider foreseeable changes—a raise, reduced hours, or a new business venture. For self-employed individuals, analyzing past trends and market conditions can provide a more accurate forecast. Tools like pay stubs, tax returns, and financial planners can aid in this process. Remember, the goal is to paint a realistic picture of your financial future, not to speculate wildly.

One common pitfall is failing to account for irregular income, such as commissions, tips, or seasonal work. If you fall into this category, average your earnings over the past few years to create a more stable estimate. For example, if you earned $40,000 one year and $50,000 the next, a projected income of $45,000 might be reasonable. Additionally, life events like marriage, divorce, or having a child can significantly impact your income and should be included in your calculations.

Accuracy in projecting income is not just about securing subsidies—it’s also about avoiding penalties. If your actual income differs significantly from your estimate, you may owe money during tax season or receive a smaller refund. Conversely, if you underestimate, you could miss out on benefits you’re entitled to. The Marketplace uses the Federal Poverty Level (FPL) as a benchmark for subsidies, so understanding where your projected income falls relative to this threshold is essential. For 2023, individuals earning between 100% and 400% of the FPL ($13,590 to $54,360) qualify for premium tax credits.

Finally, don’t hesitate to seek assistance if you’re unsure. Certified Application Counselors or tax professionals can provide guidance tailored to your situation. Regularly updating your income information throughout the year, especially if your circumstances change, ensures your coverage remains affordable and aligned with your needs. By approaching projected income with care and precision, you can maximize your subsidies and navigate the Marketplace with confidence.

Dentists and Medical Insurance: What's Covered?

You may want to see also

Explore related products

![]()

Income Verification Process: Requires documentation like tax returns, pay stubs, or employer letters

The income verification process for marketplace health insurance is a critical step in determining eligibility for subsidies and ensuring accurate premium calculations. It’s not just about stating your income—you must provide concrete proof. This process requires specific documentation, such as tax returns, pay stubs, or employer letters, to validate your earnings. Without these, your application may face delays or denials, potentially leaving you without the financial assistance you qualify for.

Let’s break down the types of documents you’ll need. Tax returns are often the gold standard, as they provide a comprehensive view of your annual income, including wages, self-employment earnings, and investment income. If you’re an employee, pay stubs are essential, showing your year-to-date earnings and deductions. For those with irregular income or self-employed individuals, employer letters or profit/loss statements can fill the gaps. Each document serves a unique purpose, and knowing which one to submit can streamline the verification process.

Here’s a practical tip: Gather these documents early in the enrollment period. Waiting until the last minute can lead to stress, especially if you need to request missing records. For example, if you’re self-employed, ensure your profit/loss statements are up-to-date and clearly reflect your income. If you’ve recently changed jobs, collect pay stubs from all employers within the relevant tax year. Proactive preparation not only speeds up verification but also reduces the risk of errors that could affect your subsidy amount.

One common pitfall is assuming estimated income will suffice. While the marketplace may allow initial enrollment based on projected earnings, final verification always requires documentation. For instance, if you estimate your income at $40,000 but your tax return shows $50,000, you could owe back subsidies or face higher premiums. Conversely, underestimating could mean missing out on financial aid. The takeaway? Accuracy is key, and documentation is your safeguard.

Finally, consider the long-term implications of proper income verification. It’s not just about securing affordable health insurance for the current year—it’s about maintaining compliance and avoiding penalties. For example, if you receive advance premium tax credits based on unverified income, you may have to repay them during tax season. By submitting the right documents upfront, you ensure stability in your coverage and peace of mind. Think of it as an investment in your financial and health security.

Does Full-Time Employment in Texas Include Health Insurance Coverage?

You may want to see also

Frequently asked questions

For marketplace health insurance, your Modified Adjusted Gross Income (MAGI) is considered. This includes most types of income, such as wages, salaries, tips, self-employment income, and investment income, but excludes certain deductions and exemptions.

No, only taxable income is considered for marketplace health insurance. Nontaxable items like certain Social Security benefits, child support payments, or gifts may not be included in your MAGI calculation.

If you’re self-employed, the marketplace uses your net profit or loss from your business, as reported on your tax return, to calculate your MAGI for health insurance eligibility.

Yes, if you file taxes jointly, both you and your spouse’s income are combined to determine your household MAGI, which is used to assess eligibility for premium tax credits and Medicaid.

If your income changes, you should update your information on HealthCare.gov as soon as possible. This ensures your premium tax credits or other subsidies are adjusted to reflect your current income and avoid potential repayment at tax time.