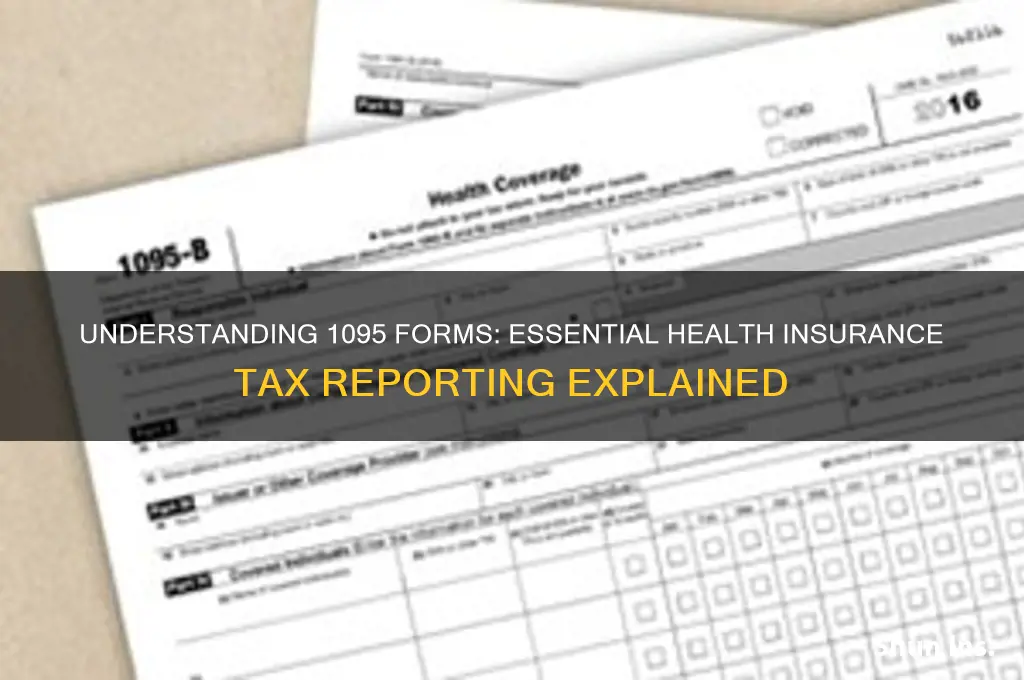

The term 1095 refers to a series of tax forms issued by the Internal Revenue Service (IRS) in the United States, specifically related to health insurance coverage under the Affordable Care Act (ACA). These forms are crucial for individuals and employers to report their health insurance status and comply with federal tax regulations. There are three main types of Form 1095: 1095-A (for health insurance marketplace coverage), 1095-B (provided by health insurance issuers or sponsors of self-insured plans), and 1095-C (used by applicable large employers to report employee health coverage offers). Understanding which 1095 form applies to your situation is essential for accurately filing taxes and avoiding penalties, as it verifies whether you, your family, or your employees had qualifying health coverage during the tax year.

| Characteristics | Values |

|---|---|

| Purpose | Provides proof of health insurance coverage for individuals and employees. |

| Form Types | Form 1095-A, 1095-B, or 1095-C, depending on the source of coverage. |

| Issuing Entities | Health Insurance Marketplace (1095-A), insurers (1095-B), or employers (1095-C). |

| Filing Requirement | Required for individuals to report health coverage on their tax returns. |

| Deadline for Receipt | Typically received by early February each year. |

| Information Included | Coverage period, individuals covered, and issuer details. |

| Relevance to ACA | Ensures compliance with the Affordable Care Act (ACA) individual mandate. |

| Tax Implications | Helps determine eligibility for premium tax credits or penalties. |

| Electronic Delivery | Can be provided electronically with recipient consent. |

| Retention Period | Recommended to keep for at least 3 years for tax records. |

| Penalty for Non-Compliance | No direct penalty for individuals, but affects tax filing accuracy. |

Explore related products

What You'll Learn

![]()

1095-A: Marketplace Coverage

If you purchased health insurance through the Health Insurance Marketplace, you'll receive Form 1095-A, a crucial document for tax season. This form isn't just another piece of paper; it's your proof of health coverage and a key to claiming the premium tax credit if you qualify. Think of it as your financial passport to navigating the intersection of healthcare and taxes.

Understanding the Breakdown:

The 1095-A is packed with essential information. It details your monthly premiums, the number of individuals covered under your plan, and most importantly, the advance payments of the premium tax credit (APTC) you received. This APTC is essentially a subsidy that lowers your monthly insurance costs. The form breaks down these payments month by month, allowing you to reconcile them with your actual income on your tax return.

Reconciling Your Credits:

During tax filing, you'll use the 1095-A to complete Form 8962, Premium Tax Credit. This form calculates whether you received the correct amount of APTC throughout the year. If your income was lower than estimated, you might be eligible for a refund. Conversely, if your income was higher, you may need to repay some of the excess credit.

Keeping it Safe:

Treat your 1095-A like a valuable document. You'll typically receive it in the mail by January 31st. If you haven't received it by early February, contact the Marketplace. Keep it with your other tax documents, as you'll need it to accurately file your return and avoid potential delays or penalties. Remember, this form is your key to unlocking potential savings or ensuring compliance with tax regulations.

Steps to Qualify and Sell Health Insurance Successfully: A Guide

You may want to see also

Explore related products

![]()

1095-B: Minimum Essential Coverage

The 1095-B form is a critical document for individuals who received health insurance coverage through certain providers, such as government-sponsored programs or self-insured group health plans. This form serves as proof that you and any covered dependents had minimum essential coverage (MEC) during the tax year, a requirement under the Affordable Care Act (ACA). Without this documentation, you may face penalties or delays when filing your taxes.

Understanding the Purpose

The 1095-B is issued by insurance providers to report the months of coverage for each individual on the plan. Unlike the 1095-A, which is tied to Marketplace plans, the 1095-B is broader, covering Medicaid, Medicare, CHIP, and employer-sponsored self-insured plans. Its primary purpose is to verify compliance with the ACA’s individual mandate, ensuring you’ve met the legal requirement for health insurance. If you received this form, it’s essential to retain it for tax purposes, even if you don’t need to file it with your return.

Key Details to Verify

When you receive your 1095-B, carefully review the information for accuracy. Check the covered individuals’ names, Social Security numbers, and the months of coverage. Errors can lead to complications during tax filing, such as discrepancies with IRS records. If you notice mistakes, contact your insurance provider immediately to request a corrected form. This step is crucial, as inaccurate data could trigger unnecessary audits or penalties.

Practical Tips for Handling the 1095-B

Keep your 1095-B in a secure location with other tax-related documents. While you typically don’t submit it with your tax return, the IRS may request it if there’s a question about your coverage status. If you’re covered by multiple plans during the year, you may receive separate 1095-B forms from each provider. Ensure you account for all coverage periods when assessing your compliance with MEC requirements. For families, verify that each dependent’s coverage is accurately reported, especially if they’re enrolled in different programs like CHIP or Medicaid.

Takeaway for Taxpayers

The 1095-B is more than just another tax form—it’s your proof of compliance with federal health insurance laws. While it simplifies the process of demonstrating MEC, its accuracy is your responsibility. By understanding its purpose, verifying its details, and keeping it accessible, you can navigate tax season with confidence and avoid potential pitfalls related to health coverage reporting.

Medicaid Health Insurance: Open Enrollment End Dates

You may want to see also

Explore related products

![]()

1095-C: Employer-Provided Insurance

Employers with 50 or more full-time employees must provide Form 1095-C to both their workers and the IRS, confirming the health insurance coverage they offered during the tax year. This requirement stems from the Affordable Care Act (ACA), which mandates that large employers provide affordable, minimum essential coverage to their full-time employees. Failure to comply can result in significant penalties, making the 1095-C a critical document for both employers and employees.

The 1095-C form is divided into several parts, each serving a specific purpose. Part I identifies the employer and employee, while Part II details the coverage offered to the employee and their dependents. Part III is where employers indicate the months during which coverage was available. This section is particularly important because it helps the IRS determine whether an employer has met the ACA’s employer mandate. For employees, this form is essential when filing taxes, as it verifies their health insurance status and may affect their eligibility for premium tax credits.

One common misconception is that the 1095-C is only relevant for employees who receive insurance through their employer. However, even if an employee declines the offered coverage, the employer must still report the availability of insurance on the form. This ensures transparency and compliance with ACA regulations. Employees should carefully review their 1095-C to ensure accuracy, as errors can lead to complications during tax filing or when applying for subsidies through the Health Insurance Marketplace.

For employers, preparing and distributing 1095-C forms requires meticulous attention to detail. They must track eligibility, enrollment, and coverage periods for each full-time employee throughout the year. Utilizing payroll or HR software that integrates ACA compliance features can streamline this process. Employers should also be aware of deadlines: Form 1095-C must be furnished to employees by January 31 and filed with the IRS by February 28 (or March 31 if filing electronically). Missing these deadlines can result in fines, with penalties increasing based on the number of forms not filed.

In summary, the 1095-C is a vital tool for enforcing the ACA’s employer mandate and ensuring employees have proof of insurance coverage. Both employers and employees must understand its purpose, components, and implications to avoid penalties and ensure compliance. By staying informed and organized, stakeholders can navigate the complexities of this form effectively.

Is Medicare Considered Health Insurance for Personal Responsibility?

You may want to see also

Explore related products

![]()

Purpose of Form 1095

Form 1095 is a critical document in the realm of health insurance, serving as proof of an individual’s health care coverage for a given tax year. Its primary purpose is to comply with the Affordable Care Act (ACA), which mandates that everyone have qualifying health insurance or face a tax penalty. This form is issued by insurance providers, employers, or government programs and is submitted to both the policyholder and the IRS. Without it, individuals may struggle to verify their coverage status during tax filing, potentially leading to penalties or delays.

The form comes in three variants—1095-A, 1095-B, and 1095-C—each tailored to different coverage scenarios. For instance, 1095-A is for those enrolled in Marketplace plans, while 1095-C is for employees of large businesses. Understanding which version applies to you is essential for accurate tax reporting. For example, if you’re self-employed and purchased a plan through Healthcare.gov, you’ll receive a 1095-A, which includes details like monthly premiums and advance premium tax credits (APTC). This specificity ensures the IRS can cross-reference your coverage claims with the data provided by insurers or employers.

One practical tip for handling Form 1095 is to retain it with your tax documents, even if you don’t need to file it directly with your return. For instance, if you’re claiming the Premium Tax Credit, the IRS may request your 1095-A to verify eligibility. Similarly, if you’re an employer providing coverage, ensuring timely distribution of 1095-Cs to employees by January 31 is crucial to avoid penalties. Mistakes on this form, such as incorrect coverage dates or missing dependents, can complicate tax filings, so double-checking its accuracy is a must.

A comparative analysis highlights the form’s role in bridging health insurance and tax compliance. Unlike other tax documents, Form 1095 doesn’t require action from most recipients—it’s primarily informational. However, its existence underscores the ACA’s emphasis on accountability. For example, while a W-2 reports income, the 1095 series reports coverage, ensuring individuals and businesses adhere to the individual mandate. This dual purpose—informing taxpayers and enforcing compliance—makes it a unique and indispensable tool in the tax ecosystem.

In conclusion, the purpose of Form 1095 extends beyond mere documentation; it’s a linchpin in the ACA’s framework, ensuring transparency and adherence to health insurance requirements. Whether you’re an individual taxpayer or an employer, understanding its nuances can streamline tax season and prevent costly errors. By recognizing its variants, retaining it properly, and verifying its accuracy, you can navigate this aspect of health insurance with confidence.

AD&D Insurance: How Does It Differ from Accident Insurance?

You may want to see also

Explore related products

![]()

Filing Requirements & Deadlines

The IRS mandates that applicable large employers (ALEs) and certain other entities file Form 1095 to report health insurance coverage offered to employees. This requirement stems from the Affordable Care Act (ACA), which aims to verify compliance with the employer shared responsibility provisions and individual mandate. Filing Form 1095 is not optional; it’s a legal obligation with specific rules and timelines that vary depending on the filer’s status and the method of submission.

For ALEs, the filing requirements are clear-cut: if you had 50 or more full-time employees (including full-time equivalents) in the previous year, you must file Form 1095-C for each employee. Smaller employers may need to file Form 1095-B if they self-insure or provide coverage through a health insurance issuer. Deadlines are strict: for paper filing, the due date is typically February 28, while electronic filing (required for 10 or more forms) extends the deadline to March 31. Missing these dates can result in penalties ranging from $290 to $580 per form, depending on intentional disregard.

Electronic filing is not just a deadline extender—it’s a strategic choice. The IRS’s Affordable Care Act Information Returns (AIR) system allows bulk uploads, reducing errors and processing time. To file electronically, you must first apply for a transmitter control code (TCC) through the IRS’s FIRE (Filing Information Returns Electronically) system, a process that can take up to 45 days. This step is often overlooked, causing last-minute delays. Pro tip: start the TCC application in December to ensure readiness for the March deadline.

Corrections are inevitable, but they follow a different timeline. If errors are discovered after filing, Form 1095-C corrections must be submitted on a separate form by the same deadlines as the original filing. For example, if you filed electronically and need to correct a form, the corrected version must still be submitted by March 31. However, if corrections affect employee eligibility for premium tax credits, prompt action is critical to avoid employee confusion and potential IRS inquiries.

Finally, state-specific requirements add another layer of complexity. While federal deadlines are consistent, states like California and New Jersey have their own reporting mandates, often with earlier deadlines. For instance, California requires Form 1095-B and 1095-C submissions by March 31 for both paper and electronic filing. Ignoring state rules can lead to additional penalties, so cross-referencing federal and state guidelines is essential. Practical advice: use a compliance calendar to track both federal and state deadlines, ensuring no detail slips through the cracks.

Understanding Health Net Insurance: Coverage, Benefits, and How It Works

You may want to see also

Frequently asked questions

A 1095 form is a tax document that provides proof of health insurance coverage for individuals and their dependents. It is required under the Affordable Care Act (ACA) and is used to verify compliance with the individual mandate.

Individuals who had health insurance coverage through an employer, the Health Insurance Marketplace, or certain government programs (like Medicare or Medicaid) will receive a 1095 form. It is sent to both the insured individual and the IRS.

Yes, there are three types: 1095-A (for Marketplace coverage), 1095-B (for coverage through insurers or self-insured employers), and 1095-C (for large employers offering health insurance).

No, you do not need to file the 1095 form with your taxes. However, you should keep it for your records in case the IRS requests verification of your health insurance coverage.

If you haven’t received your 1095 form by early February, contact your employer, insurance provider, or the Health Insurance Marketplace. You can also access a copy of your 1095-A through your Marketplace account if applicable.