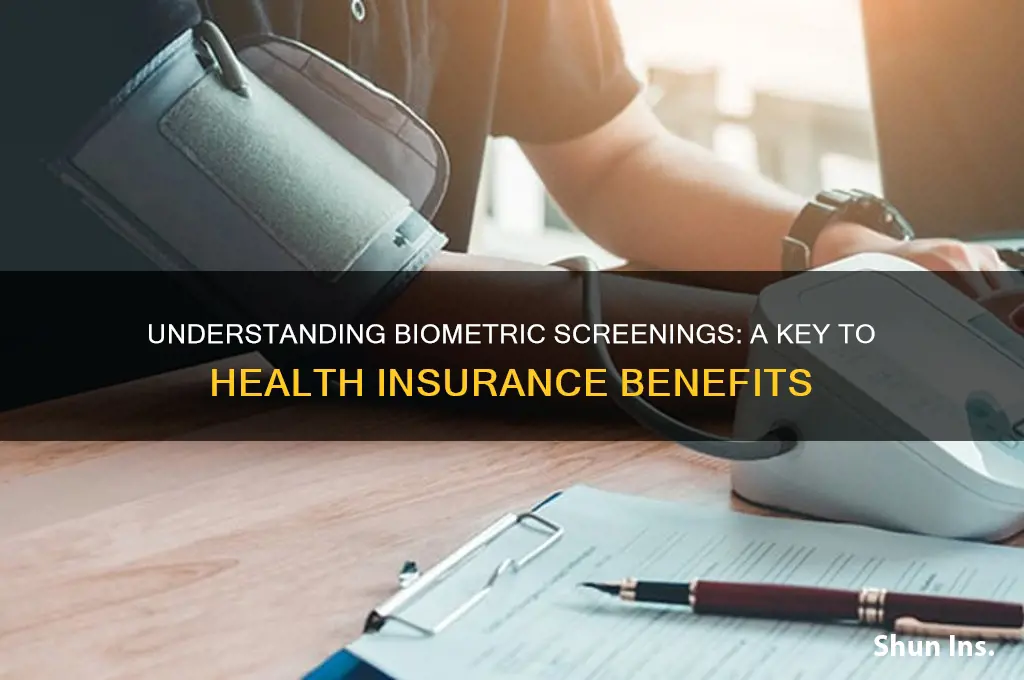

Biometric screenings are essential tools used by health insurance providers to assess an individual’s health status by measuring key physiological markers such as blood pressure, cholesterol levels, blood glucose, and body mass index (BMI). These screenings provide insurers with valuable data to evaluate risk factors associated with chronic conditions like diabetes, heart disease, or obesity, which can influence policy premiums or eligibility. For policyholders, biometric screenings often serve as a proactive way to identify potential health issues early, offering personalized recommendations for lifestyle changes or medical interventions. Many insurance companies incentivize participation in these screenings by offering discounts, rewards, or wellness program benefits, fostering a collaborative approach to preventive healthcare and long-term well-being.

| Characteristics | Values |

|---|---|

| Definition | A health assessment tool used by insurers to evaluate an individual's health risks based on measurable physical traits. |

| Purpose | To determine eligibility, premiums, or personalized health plans for insurance coverage. |

| Common Metrics Measured | Blood pressure, cholesterol levels, blood glucose, BMI, waist circumference, and body fat percentage. |

| Methods of Screening | On-site health fairs, workplace screenings, at-home test kits, or clinical visits. |

| Frequency | Typically conducted annually or as required by the insurance provider. |

| Incentives for Participation | Discounts on premiums, wellness program rewards, or reduced deductibles. |

| Privacy and Data Security | Protected under HIPAA or similar regulations; data used solely for risk assessment. |

| Impact on Premiums | Higher risk scores may lead to increased premiums; lower risk scores may reduce costs. |

| Voluntary vs. Mandatory | Often voluntary, but some employers or insurers may require participation for certain benefits. |

| Latest Trends | Integration with wearable tech (e.g., fitness trackers) and AI-driven health analytics. |

| Criticisms | Concerns about discrimination based on health metrics and potential invasion of privacy. |

Explore related products

What You'll Learn

- Purpose of Screening: Assesses health risks, determines insurance eligibility, and tailors coverage based on individual health data

- Common Tests Included: Blood pressure, cholesterol, glucose, BMI, and lifestyle questions are standard components

- Impact on Premiums: Results can influence insurance costs, with healthier outcomes potentially lowering premium rates

- Privacy Concerns: Data protection laws govern how biometric information is stored and shared by insurers

- Preparation Tips: Fasting, avoiding certain medications, and staying hydrated can ensure accurate test results

![]()

Purpose of Screening: Assesses health risks, determines insurance eligibility, and tailors coverage based on individual health data

Biometric screenings serve as a critical tool for health insurance providers, offering a snapshot of an individual's health status through measurable indicators such as blood pressure, cholesterol levels, glucose, and body mass index (BMI). These metrics are not just numbers; they are predictive markers that help identify potential health risks before they escalate into chronic conditions. For instance, a screening might reveal elevated blood pressure readings, signaling a heightened risk for hypertension, which, if left unmanaged, could lead to heart disease or stroke. By capturing these early warning signs, insurers can intervene proactively, potentially saving lives and reducing long-term healthcare costs.

From an insurance perspective, biometric screenings play a dual role in determining eligibility and setting premiums. Insurers use the data to assess an applicant’s risk profile, which directly influences coverage options and costs. For example, an individual with optimal biometric results—such as a total cholesterol level below 200 mg/dL and a fasting glucose level under 100 mg/dL—may qualify for lower premiums or enhanced benefits. Conversely, those with suboptimal results might face higher costs or be required to participate in wellness programs as a condition of coverage. This approach aligns incentives, encouraging policyholders to take an active role in managing their health.

The true value of biometric screenings lies in their ability to tailor insurance coverage to the individual. Rather than offering one-size-fits-all plans, insurers can customize policies based on specific health data. For instance, someone with prediabetes (fasting glucose between 100–125 mg/dL) might receive coverage that includes diabetes prevention programs, nutritional counseling, or discounted gym memberships. Similarly, an individual with a high BMI could be offered access to weight management resources or bariatric surgery coverage if clinically appropriate. This personalized approach not only improves health outcomes but also fosters a sense of partnership between the insurer and the insured.

However, it’s essential to approach biometric screenings with an understanding of their limitations. While they provide valuable insights, they are not definitive diagnoses. Abnormal results should prompt further evaluation by a healthcare provider rather than immediate alarm. For example, a single high blood pressure reading (above 130/80 mmHg) during a screening does not automatically mean hypertension; it could be due to temporary factors like stress or caffeine intake. Policyholders should view screenings as a starting point for conversation with their doctor, not a final verdict on their health.

In practice, maximizing the benefits of biometric screenings requires active participation and follow-through. Individuals should prepare for screenings by fasting as instructed (typically 8–12 hours for accurate glucose and lipid measurements), avoiding caffeine or strenuous exercise beforehand, and wearing loose-fitting clothing for ease of measurement. Afterward, they should review results with their healthcare provider to create actionable plans, such as dietary modifications, exercise regimens, or medication adjustments. For insurers, the challenge lies in communicating the value of screenings clearly and ensuring that the data collected translates into meaningful, accessible support for policyholders. When executed effectively, biometric screenings become a win-win: individuals gain insights to improve their health, and insurers build a healthier, more engaged customer base.

Does Blue Cross Blue Shield Coverage End at Age 26?

You may want to see also

Explore related products

![]()

Common Tests Included: Blood pressure, cholesterol, glucose, BMI, and lifestyle questions are standard components

Biometric screenings for health insurance typically include a battery of tests designed to assess key health indicators, offering a snapshot of an individual’s overall well-being. Among the most common are blood pressure, cholesterol, glucose, and BMI measurements, alongside lifestyle questions. These metrics are not arbitrary; they are carefully selected to identify risk factors for chronic conditions like hypertension, diabetes, and heart disease, which are leading drivers of healthcare costs. For instance, a blood pressure reading above 130/80 mmHg signals hypertension, while a fasting glucose level exceeding 126 mg/dL indicates diabetes. Understanding these benchmarks is the first step in leveraging biometric screenings for preventive health management.

Consider the cholesterol test, a cornerstone of these screenings. It measures total cholesterol, LDL (bad cholesterol), HDL (good cholesterol), and triglycerides. Optimal levels—total cholesterol below 200 mg/dL, LDL under 100 mg/dL, HDL above 60 mg/dL, and triglycerides below 150 mg/dL—are associated with lower cardiovascular risk. However, nearly 94 million U.S. adults have cholesterol levels above recommended ranges, often without symptoms. This silent threat underscores the importance of regular screenings, especially for individuals over 35 or those with a family history of heart disease. Practical tips include fasting for 9–12 hours before the test and avoiding fatty meals the night prior to ensure accurate results.

BMI (Body Mass Index) is another critical component, calculated by dividing weight in kilograms by height in meters squared. While a BMI between 18.5 and 24.9 is considered healthy, over 40% of adults in the U.S. fall into the obese category (BMI ≥ 30). This metric, though imperfect—it doesn’t differentiate muscle from fat—serves as a quick, cost-effective tool for assessing obesity-related risks. Pairing BMI with waist circumference measurements (ideal: <40 inches for men, <35 inches for women) provides a more comprehensive view of metabolic health. For those with elevated BMI, actionable steps include tracking daily steps, reducing portion sizes, and incorporating strength training to build muscle mass.

Lifestyle questions, often overlooked, are equally vital. These inquiries delve into habits like smoking, alcohol consumption, physical activity, and diet. For example, smoking just one cigarette per day increases cardiovascular risk by 50%, while moderate exercise (150 minutes weekly) can lower blood pressure by 5–8 mmHg. Insurers use these responses to tailor wellness programs, offering incentives like premium discounts for participants who quit smoking or adopt healthier habits. Honesty in these assessments is key, as they directly influence personalized health improvement plans.

In summary, biometric screenings are not just bureaucratic hurdles for insurance enrollment; they are powerful tools for early detection and intervention. By understanding the significance of blood pressure, cholesterol, glucose, BMI, and lifestyle questions, individuals can take proactive steps to mitigate health risks. Whether it’s adjusting dietary intake to lower LDL cholesterol or increasing physical activity to manage glucose levels, the insights gained from these tests empower informed decision-making. Treat your next screening not as a chore, but as a roadmap to a healthier future.

Travel Medical Insurance: What You Need to Know

You may want to see also

Explore related products

![]()

Impact on Premiums: Results can influence insurance costs, with healthier outcomes potentially lowering premium rates

Biometric screenings are not just health check-ups; they are financial assessments in disguise. These screenings, often required by health insurance providers, measure key health indicators like blood pressure, cholesterol levels, glucose, and BMI. The results can directly impact your insurance premiums, turning your health metrics into a currency that either costs or saves you money. For instance, a 40-year-old with a BMI of 25 (normal range) and a cholesterol level under 200 mg/dL might see premiums reduced by up to 15%, while someone with a BMI of 35 (obese) and cholesterol over 240 mg/dL could face surcharges of 20% or more.

Consider this a negotiation with your insurer, where your body’s data is the bargaining chip. Healthier results signal lower risk, incentivizing insurers to offer discounts. For example, a non-smoker with a blood pressure reading of 120/80 mmHg and a fasting glucose level below 100 mg/dL is a prime candidate for reduced rates. Conversely, elevated readings—like a glucose level above 125 mg/dL or a systolic blood pressure over 140 mmHg—can trigger higher premiums or even policy exclusions. The takeaway? Biometric screenings aren’t just about health; they’re about dollars and cents.

To maximize savings, approach these screenings strategically. Fast for 8–12 hours before the test to ensure accurate glucose and lipid panel results. Hydrate well but avoid excessive caffeine or alcohol 24 hours prior, as these can skew blood pressure readings. If your BMI is borderline, focus on losing 5–10% of your body weight in the months leading up to the screening—a reduction that can significantly improve your metabolic markers. For those with pre-existing conditions, work with your healthcare provider to stabilize numbers; even small improvements, like lowering LDL cholesterol by 30 mg/dL, can translate to premium reductions.

The comparative advantage here is clear: proactive health management pays off. Insurers often categorize policyholders into risk tiers based on biometric data, with each tier corresponding to a premium rate. For example, Tier 1 (optimal health) might enjoy rates 25% below average, while Tier 4 (high-risk) could pay 50% more. This tiered system underscores the importance of treating biometric screenings as actionable feedback rather than a passive requirement. By understanding how each metric influences premiums, you can target specific areas for improvement, effectively turning your health into a cost-saving tool.

Finally, don’t underestimate the long-term impact of these screenings. Consistent healthy results over multiple years can lead to cumulative premium reductions, while deteriorating health can result in escalating costs. Think of it as a health investment account: deposits of good habits yield dividends in lower insurance expenses. For families, this can mean hundreds or even thousands of dollars saved annually. The key is to view biometric screenings not as a one-time event but as a recurring opportunity to optimize both health and finances. After all, in the world of health insurance, your numbers aren’t just data—they’re dollars.

Meet the CEO of TBA Trucking Insurance Company: Leadership Insights

You may want to see also

Explore related products

![]()

Privacy Concerns: Data protection laws govern how biometric information is stored and shared by insurers

Biometric screenings for health insurance often involve collecting sensitive data like fingerprints, facial recognition, or health metrics, which can reveal intimate details about an individual’s lifestyle and genetic predispositions. This raises significant privacy concerns, as such information, if misused, could lead to discrimination in employment, insurance premiums, or even personal relationships. Data protection laws, such as the General Data Protection Regulation (GDPR) in Europe or the Health Insurance Portability and Accountability Act (HIPAA) in the U.S., mandate strict guidelines for how insurers store and share this data. However, the complexity of these laws and varying global standards create gaps that could expose individuals to risks.

Consider the storage of biometric data: insurers must encrypt this information and limit access to authorized personnel only. For instance, under HIPAA, covered entities must implement safeguards like secure servers and regular audits to prevent data breaches. Yet, the rise of cyberattacks on healthcare systems highlights the vulnerability of even the most protected systems. A single breach could expose millions of records, as seen in the 2015 Anthem data breach, where hackers accessed personal information of nearly 80 million individuals. This underscores the need for insurers to not only comply with laws but also invest in robust cybersecurity measures.

Sharing biometric data introduces another layer of risk. Insurers often collaborate with third-party vendors for data analysis or processing, which requires transferring sensitive information. Data protection laws typically require explicit consent from individuals before sharing their data, but the fine print in insurance policies can obscure this process. For example, some policies may bury consent clauses in lengthy documents, leaving individuals unaware of how their data is being used. This lack of transparency erodes trust and raises ethical questions about informed consent.

To mitigate these risks, individuals should take proactive steps. First, carefully review insurance policies to understand how biometric data is collected, stored, and shared. Second, inquire about the insurer’s compliance with data protection laws and their cybersecurity protocols. Third, consider opting out of biometric screenings if the potential risks outweigh the benefits, though this may affect insurance premiums. Finally, stay informed about updates to data protection laws, as regulations like GDPR continue to evolve in response to technological advancements.

In conclusion, while biometric screenings offer insurers valuable insights into policyholders’ health, they also pose significant privacy risks. Data protection laws provide a framework for safeguarding this information, but their effectiveness depends on rigorous enforcement and individual vigilance. By understanding these laws and taking proactive measures, individuals can better protect their biometric data in an increasingly interconnected world.

Does Private Health Insurance Cover Orthodontics? A Comprehensive Guide

You may want to see also

Explore related products

![]()

Preparation Tips: Fasting, avoiding certain medications, and staying hydrated can ensure accurate test results

Biometric screenings are pivotal for assessing health risks and tailoring insurance plans, but their accuracy hinges on proper preparation. Fasting, for instance, is often required for blood tests measuring glucose and cholesterol levels. Skipping food and beverages (except water) for 9–12 hours before the screening ensures baseline readings, free from the temporary spikes caused by recent meals. This simple step can prevent misleading results that might inflate risk assessments or skew insurance premiums.

Medication management is equally critical, as certain drugs can alter biometric markers. For example, statins lower cholesterol, while blood pressure medications reduce hypertension readings. If possible, consult your healthcare provider about temporarily pausing non-essential medications 24–48 hours before the screening, ensuring the results reflect your natural health state. However, never discontinue prescribed medications without professional advice, especially for chronic conditions like diabetes or heart disease.

Hydration plays a subtle yet significant role in biometric screenings. Dehydration can thicken blood, making it harder to draw samples and potentially skewing results like hematocrit levels. Drinking 8–10 glasses of water in the 24 hours leading up to the test (while adhering to fasting guidelines) maintains optimal hydration. Avoid overhydration, though, as excessive water intake can dilute electrolyte levels, affecting tests like sodium and potassium measurements.

Practical tips can streamline the preparation process. Set an alarm to mark the start of your fasting period, and keep a water bottle handy to stay hydrated without breaking the fast. If you’re unsure about medication adjustments, bring a list of your current prescriptions to the screening for the technician’s review. Finally, schedule the screening for early morning to minimize fasting discomfort and ensure compliance with time-sensitive requirements. These steps collectively safeguard the integrity of your biometric data, providing a clear snapshot of your health for insurance purposes.

Medical Insurance: A Necessary Safety Net for All

You may want to see also

Frequently asked questions

A biometric screening is a health assessment that measures key physical indicators such as blood pressure, cholesterol levels, blood sugar, and body mass index (BMI). It helps insurers evaluate an individual’s health risks and determine appropriate coverage or premiums.

Health insurance companies use biometric screenings to assess an individual’s health status, identify potential risks, and encourage preventive care. This information helps them tailor policies, offer wellness programs, and manage overall healthcare costs.

It depends on the insurance provider and policy. Some insurers may require biometric screenings as part of the application process or for certain plans, while others may offer it as an optional tool for policyholders to monitor their health. Always check with your provider for specific requirements.