A federal tax credit health insurance, often referred to as the Premium Tax Credit (PTC), is a subsidy provided by the U.S. government to help eligible individuals and families with low to moderate incomes afford health insurance plans purchased through the Health Insurance Marketplace. Established under the Affordable Care Act (ACA), this tax credit is designed to reduce the monthly premiums for qualified health plans, making coverage more accessible and affordable. Eligibility for the credit is based on household income, family size, and the cost of benchmark plans in the applicant’s area. The credit can be applied directly to monthly premiums or claimed as a refund when filing federal taxes, offering flexibility for enrollees to manage their healthcare costs effectively.

| Characteristics | Values |

|---|---|

| Definition | A federal tax credit that helps eligible individuals and families pay for health insurance premiums purchased through the Health Insurance Marketplace. |

| Official Name | Premium Tax Credit (PTC) |

| Eligibility Criteria | - Household income between 100% and 400% of the Federal Poverty Level (FPL). - Not eligible for affordable employer-sponsored insurance or government coverage (e.g., Medicaid). - Enrolled in a health plan through the Marketplace. |

| Income Limits (2023) | - Lower limit: 100% of FPL ($14,580 for individuals, $30,000 for family of 4). - Upper limit: 400% of FPL ($58,320 for individuals, $120,000 for family of 4). |

| Application Process | Apply through the Health Insurance Marketplace during open enrollment or special enrollment periods. |

| Credit Calculation | Based on the difference between the benchmark plan premium and a percentage of the household income. |

| Refundable vs. Non-Refundable | Refundable, meaning if the credit exceeds taxes owed, the excess is refunded. |

| Reconciliation | Taxpayers must reconcile advance payments of the credit on their tax return (Form 8962). |

| Impact on Premiums | Reduces monthly health insurance premiums for eligible individuals. |

| Availability | Available in all states using the federal Marketplace (Healthcare.gov). |

| Recent Changes (2023) | Enhanced subsidies extended through 2025 under the Inflation Reduction Act. |

| Key Benefit | Makes health insurance more affordable for low- to moderate-income individuals and families. |

Explore related products

What You'll Learn

![]()

Eligibility requirements for federal tax credit health insurance

Federal tax credits for health insurance, specifically the Premium Tax Credit (PTC), are designed to make health coverage more affordable for individuals and families. However, not everyone qualifies. Eligibility hinges on a combination of income, household size, and other specific criteria. Understanding these requirements is crucial for anyone seeking to reduce their health insurance costs through this program.

Income Thresholds: The Cornerstone of Eligibility

The primary eligibility factor for the Premium Tax Credit is income. Your household income must fall within a specific range, expressed as a percentage of the federal poverty level (FPL). For 2023, individuals earning between 100% and 400% of the FPL generally qualify. For a family of four, this translates to an income range of approximately $28,000 to $112,000. It's important to note that these figures are subject to annual adjustments.

Utilize online calculators or consult with a tax professional to determine your eligibility based on your specific circumstances.

Household Size and Composition: A Crucial Factor

The size of your household directly impacts your eligibility. The FPL thresholds are adjusted based on the number of individuals in your household. For example, a single individual will have a lower income threshold than a family of four. Additionally, the relationship between household members matters. Spouses, dependents, and certain other relatives are typically included in the household size calculation.

Ensure you accurately report all household members when applying for the tax credit.

Other Eligibility Considerations: Beyond Income and Household

While income and household size are primary factors, other eligibility requirements exist. You must:

- Not be eligible for affordable employer-sponsored health insurance: If your employer offers health insurance that meets certain affordability and coverage standards, you generally won't qualify for the PTC.

- Not be eligible for government-sponsored coverage: Individuals eligible for Medicare, Medicaid, or other government health programs are typically ineligible for the PTC.

- File taxes as a U.S. citizen or lawful resident: Citizenship or legal residency status is a prerequisite for receiving the tax credit.

- Enroll in a qualified health plan through the Health Insurance Marketplace: The PTC can only be applied to plans purchased through the Marketplace.

Navigating the Application Process: Tips for Success

Applying for the Premium Tax Credit involves providing detailed information about your income, household, and health insurance status. Here are some tips:

- Gather necessary documentation: Have tax returns, pay stubs, and proof of household composition readily available.

- Use the Health Insurance Marketplace: The Marketplace website provides a user-friendly platform for applying and comparing plans.

- Seek assistance if needed: Navigators and certified application counselors are available to provide free assistance with the application process.

Understanding the eligibility requirements for federal tax credit health insurance is the first step towards accessing this valuable financial assistance. By carefully reviewing the criteria and following the application process, individuals and families can potentially significantly reduce their health insurance costs.

UCSF Accepted Insurance Providers: A Comprehensive Guide to Coverage Options

You may want to see also

Explore related products

![]()

How to claim health insurance tax credits

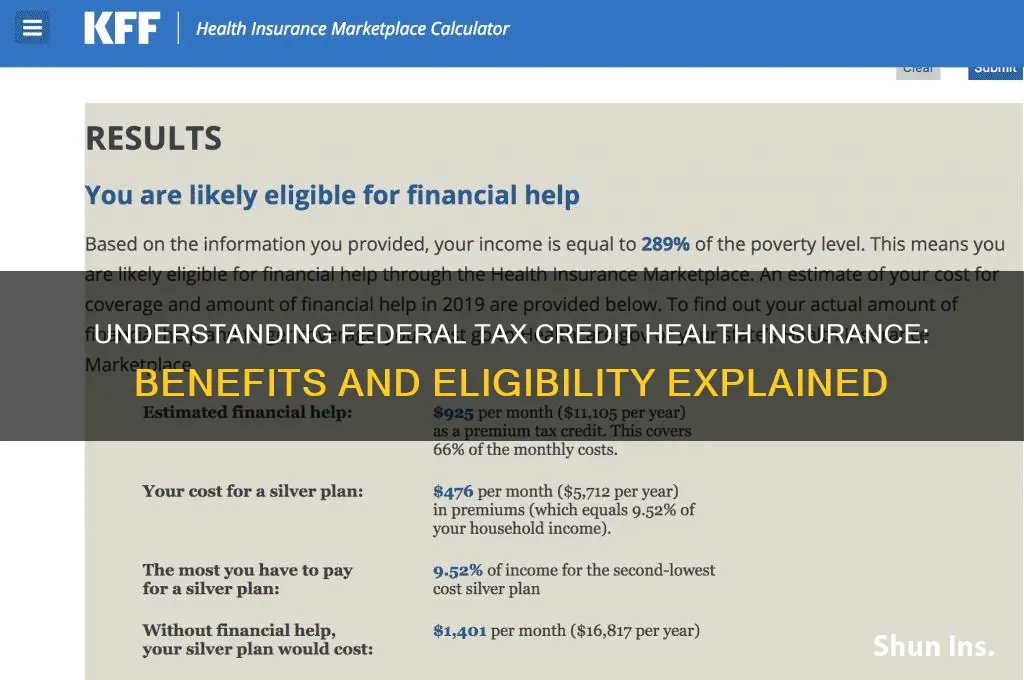

Federal tax credits for health insurance, specifically the Premium Tax Credit (PTC), are designed to make health coverage more affordable for individuals and families with moderate incomes. To claim these credits, understanding the eligibility criteria is the first step. You must purchase health insurance through the Health Insurance Marketplace, have a household income between 100% and 400% of the federal poverty level, and not be eligible for other qualifying coverage like Medicaid or an employer-sponsored plan. For instance, in 2023, a family of four earning between $28,000 and $112,000 annually could qualify, though exact figures vary by household size and location.

Once eligibility is confirmed, the claiming process begins during enrollment in a Marketplace plan. You can choose to receive the tax credit in advance, directly reducing your monthly premiums, or claim the full amount when filing your federal taxes. To apply for advance payments, complete Form 8962 alongside your tax return, providing details about your income and coverage. Accuracy is critical here—overestimating your income may result in repaying excess credits, while underestimating could mean missing out on benefits. For example, if your income fluctuates during the year, promptly update your Marketplace account to adjust your credit amount.

A common pitfall is misunderstanding the reconciliation process during tax filing. If you received advance credits, you must file Form 8962 to reconcile the amount paid with your actual income. This step ensures you neither owe additional taxes nor leave money unclaimed. For instance, if your income was lower than expected, you might qualify for a larger credit, increasing your refund. Conversely, if your income rose, you may need to repay a portion of the advance credits, capped based on your income level to prevent excessive financial burden.

Practical tips can streamline the process. Keep detailed records of your income, premium payments, and any changes in household circumstances throughout the year. Use the Marketplace’s tax credit calculator to estimate your eligibility and potential savings. If self-employed or with variable income, consider consulting a tax professional to navigate complexities. Finally, stay informed about policy changes—recent expansions under the American Rescue Plan, for example, increased credit amounts and removed the income cap temporarily, making more individuals eligible for substantial savings. By staying proactive and informed, claiming health insurance tax credits becomes a manageable, rewarding task.

Does PPO Health Insurance Cover Cosmetic Surgeries? What You Need to Know

You may want to see also

Explore related products

$19.9 $19.9

![]()

Income limits for premium tax credits

Premium tax credits, a cornerstone of the Affordable Care Act, are designed to make health insurance more affordable for individuals and families with moderate incomes. However, eligibility for these credits hinges on income limits that are carefully calibrated each year. For 2023, the income range for qualifying is generally between 100% and 400% of the Federal Poverty Level (FPL). For a single individual, this translates to an annual income between $13,590 and $54,360, while a family of four must fall between $27,750 and $111,000. These figures are not static; they are adjusted annually to account for inflation and economic shifts, ensuring that the credits remain accessible to those who need them most.

Understanding these income limits requires a nuanced approach, as they are not just about the raw numbers. For instance, if your income falls below 100% of the FPL, you may qualify for Medicaid instead of premium tax credits, depending on your state’s Medicaid expansion status. Conversely, if your income exceeds 400% of the FPL, you are generally ineligible for premium tax credits but may still purchase health insurance through the marketplace at full price. A practical tip is to use the HealthCare.gov subsidy calculator to estimate your eligibility based on your household size and income, ensuring you don’t miss out on potential savings.

The income limits also account for household size, which can significantly impact eligibility. For example, a family of six with an income of $138,600 (400% of the FPL for that household size) would qualify for premium tax credits, whereas a single individual earning the same amount would not. This tiered system ensures that larger families, who often face higher living expenses, are not disproportionately excluded from assistance. It’s crucial to report accurate household size and income when applying, as discrepancies can lead to incorrect credit amounts or even repayment of excess credits at tax time.

One common misconception is that income limits are rigid and unforgiving. In reality, the system allows for some flexibility, particularly in cases of income fluctuations. If your income changes during the year—due to a job loss, raise, or other circumstances—you can update your information through the marketplace to adjust your credit amount. This ensures that your premiums remain affordable despite shifts in your financial situation. However, failing to report changes promptly can result in overpayment or underpayment of credits, so staying proactive is key.

Finally, it’s worth noting that income limits for premium tax credits are just one piece of the affordability puzzle. Other factors, such as the cost of available plans in your area and the size of your household, also play a role in determining your final premium after credits. For instance, in areas with higher insurance costs, the credits may cover a larger portion of the premium, making coverage more attainable. By understanding these limits and how they interact with other variables, you can navigate the health insurance marketplace with greater confidence and secure the best possible deal for your situation.

Top Health Insurance Options for College Students: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Marketplace vs. private insurance tax credits

Federal tax credits for health insurance are designed to make coverage more affordable, but the rules differ significantly depending on whether you purchase insurance through the Health Insurance Marketplace or directly from a private insurer. Understanding these differences is crucial for maximizing your savings and ensuring compliance with tax regulations.

Eligibility and Income Thresholds: The Marketplace Advantage

The Premium Tax Credit (PTC) is exclusively available to individuals and families who enroll in health plans through the Marketplace. To qualify, your household income must fall between 100% and 400% of the federal poverty level (FPL). For example, in 2023, a family of four earning between $27,750 and $111,000 would be eligible. Private insurance plans, on the other hand, do not offer federal tax credits based on income. Instead, policyholders may qualify for other deductions, such as those for self-employed individuals, but these are not tied to premium costs or income thresholds.

Calculation and Application: How Credits Differ

Marketplace tax credits are advanceable, meaning you can apply them directly to your monthly premiums, reducing out-of-pocket costs immediately. The credit amount is calculated based on the cost of the second-lowest Silver plan in your area and your income. For instance, if the benchmark plan costs $1,000 per month and your expected contribution is $200, the credit covers the remaining $800. Private insurance does not offer this advance payment option; instead, tax benefits are claimed during filing, often as itemized deductions or adjustments to income, which may not provide immediate financial relief.

Plan Flexibility vs. Credit Accessibility

Private insurance offers greater flexibility in plan choice, including access to networks and providers not available on the Marketplace. However, this flexibility comes at the cost of tax credit ineligibility. Marketplace plans, while more limited in variety, are the only avenue for accessing federal premium tax credits. For example, a Bronze plan on the Marketplace might have higher out-of-pocket costs but could be nearly free after applying the tax credit, whereas a similar private plan would require full premium payment upfront.

Reconciliation and Tax Implications

At tax time, Marketplace enrollees must reconcile their advance premium tax credits using Form 8962. If your income was higher than estimated, you may owe a portion of the credit back to the IRS. Conversely, if your income was lower, you could receive a refund. Private insurance policyholders do not face this reconciliation process, as their tax benefits are typically fixed and claimed directly on their return. This simplicity can be advantageous but lacks the potential for substantial upfront savings offered by Marketplace credits.

Practical Tips for Maximizing Benefits

To determine the best option, compare your projected income to the FPL and evaluate the total cost of plans after applying potential credits. If you qualify for Marketplace subsidies, enrolling through Healthcare.gov can yield significant monthly savings. For those with incomes above 400% FPL or seeking specific plan features, private insurance may be preferable, despite the absence of federal tax credits. Always consult a tax professional or use online calculators to estimate your eligibility and potential savings accurately.

Maximize Your Coverage: Tips for Better Health Insurance Plans

You may want to see also

Explore related products

![]()

Impact of tax credits on insurance premiums

Federal tax credits for health insurance, such as those provided through the Affordable Care Act (ACA), directly influence insurance premiums by reducing the out-of-pocket costs for eligible individuals and families. These credits, formally known as the Premium Tax Credit (PTC), are designed to make health insurance more affordable for those with moderate incomes. For instance, a family of four earning up to $106,000 annually in 2023 may qualify for a PTC, which is applied directly to their monthly premiums, effectively lowering their insurance costs. This mechanism ensures that health coverage remains accessible to a broader population, even as premiums continue to rise.

The impact of tax credits on premiums is most evident in the ACA’s Marketplace plans. Without these credits, many individuals would face premiums that consume a significant portion of their income. For example, a 40-year-old earning $40,000 annually might see their monthly premium drop from $450 to $150 after applying the PTC. This reduction not only makes insurance more affordable but also encourages enrollment, as individuals are less likely to forgo coverage due to cost concerns. However, the effectiveness of this system depends on accurate income reporting, as credits are reconciled during tax season, potentially leading to repayment if income estimates are too low.

From a comparative perspective, tax credits create a stark contrast between the premiums paid by eligible and ineligible individuals. Those earning above the eligibility threshold (e.g., 400% of the federal poverty level) often face the full brunt of premium increases, while those below the threshold benefit from substantial subsidies. This disparity highlights the role of tax credits in mitigating the financial burden of insurance, particularly for middle-income households. For instance, in states with high insurance costs, such as Alaska or Wyoming, the PTC can reduce premiums by 50% or more for qualifying individuals, making coverage feasible where it might otherwise be prohibitive.

To maximize the benefits of tax credits, individuals should take proactive steps during enrollment. First, accurately estimate your annual income to avoid discrepancies during tax reconciliation. Second, compare plans on the Marketplace, as the PTC adjusts based on the second-lowest-cost Silver plan in your area, but you can apply it to any metal tier. Third, consider consulting a navigator or broker to ensure you’re taking full advantage of available credits. For example, temporary expansions under the American Rescue Plan Act (ARPA) increased PTC eligibility and reduced premiums further, but these changes require careful navigation to optimize savings.

In conclusion, federal tax credits serve as a critical tool in reducing insurance premiums for millions of Americans. By subsidizing costs based on income, these credits make health coverage more attainable, particularly for those in the middle-income bracket. However, their effectiveness relies on accurate income reporting and informed plan selection. As premiums continue to rise, understanding and leveraging these credits remains essential for anyone seeking affordable health insurance. Practical steps, such as precise income estimation and plan comparison, can further enhance the impact of these subsidies on individual and family budgets.

How to Print Proof of Medicaid Insurance in NY

You may want to see also

Frequently asked questions

A federal tax credit for health insurance, often referred to as the Premium Tax Credit, is a subsidy provided by the federal government to help eligible individuals and families afford health insurance plans purchased through the Health Insurance Marketplace. It reduces the monthly premium cost of your insurance plan.

Eligibility for the federal tax credit depends on your household income and size. Generally, individuals and families with incomes between 100% and 400% of the federal poverty level (FPL) may qualify. You must also not have access to affordable employer-sponsored insurance or government coverage like Medicare.

To apply for the federal tax credit, you need to enroll in a health insurance plan through the Health Insurance Marketplace during the Open Enrollment Period or a Special Enrollment Period if you qualify. When completing your application, provide accurate income and household information to determine your eligibility for the tax credit.