A fully insured medical plan is a traditional type of insurance option sponsored by an employer. The employer pays a fixed premium to an insurance company, which covers their employees' medical claims. The premium rates are fixed annually based on the number of enrolled employees and will only change if the number of employees changes. The insurance company pays medical claims based on the benefit outline, and employees must pay any deductibles or copays required for covered healthcare services under the policy. This type of plan offers financial predictability but potentially higher costs. It also eliminates the administrative duties and expenses related to a self-insured health plan.

| Characteristics | Values |

|---|---|

| Type of insurance option | Sponsored by an employer |

| Payment of premium | Employers pay a fixed premium to an insurance company for employee coverage |

| Payment of claims | The insurance company pays the health care claims |

| Financial risk | Lower for employers as the insurance company assumes all responsibility for providing health coverage |

| Premium rates | Fixed annually based on the number of enrolled employees |

| Customization | Limited customization options |

| Administrative burden | Lower for employers as the insurance carrier takes the lead in providing administrative services |

| Compliance | Subject to state and federal insurance regulations |

| Cost | Can be more expensive for employers |

| Cost savings | No cost savings as there is no refund for money not spent on claims |

| Taxes | Lower taxes for employers |

Explore related products

What You'll Learn

- How it works: Employers pay a fixed premium to an insurer for their employees' medical expenses?

- Financial predictability: premium rates are annually fixed, offering predictability for employers

- Reduced financial risk: the insurance company assumes responsibility for providing health coverage, protecting employers from large claims

- Administrative relief: the insurance carrier takes the lead in providing administrative services, reducing the burden on employers

- Compliance: fully insured plans are subject to state and federal insurance regulations, and employers can outsource compliance requirements to the carrier

![]()

How it works: Employers pay a fixed premium to an insurer for their employees' medical expenses

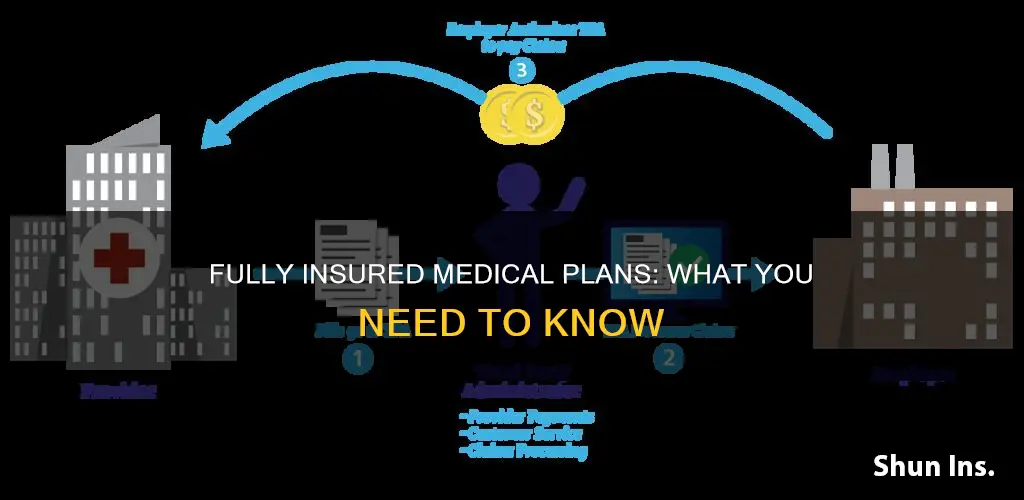

A fully insured health plan is a traditional approach to employee benefits. It involves employers paying a fixed premium to an insurance company to cover their employees' medical expenses. The premium rates are annually fixed and based on the number of enrolled employees in the plan each month. This number can change, and so too can the premium. The insurance company then pays the medical claims based on the benefit outline in the policy.

The employer will pay a monthly premium to the insurance carrier, which covers the medical claims of the enrolled employees. This offers financial predictability, as the employer knows what to expect regarding healthcare costs, and can budget accordingly. This type of plan also reduces the financial risk to the employer, as the insurance company assumes responsibility for providing health coverage, including the cost.

The insurance company takes on the administrative burden, providing services such as enrolment and claims processing. This can be beneficial for smaller employers who do not have the staff, resources, or expertise to manage healthcare benefits themselves. A fully insured plan may be a good choice for employers who want to offer quality health benefits to their employees, but do not have the time or personnel to manage the process.

While this type of plan offers financial predictability and reduces risk, it may result in higher costs. Employers do not receive refunds for money that isn't spent on claims, and the insurance company can use this money however they choose. Fully insured plans can also be rigid, as they are not fully customisable.

Warby Parker and Medicaid: What's the Deal?

You may want to see also

Explore related products

![]()

Financial predictability: premium rates are annually fixed, offering predictability for employers

A fully insured medical plan is a traditional type of insurance option sponsored by an employer. It involves employers paying a fixed premium to a health insurance carrier for their employees' medical expenses. This offers financial predictability but potentially higher costs. The insurance company assumes all responsibility for providing health coverage, including the cost, and employers are protected from the burden of large medical bills.

The premium rates in a fully insured plan are annually fixed, based on the number of enrolled employees each month. This offers predictability for employers, as they know what to expect in terms of their healthcare costs and can budget accordingly. The fixed premium rate also allows companies to stay on budget, as the cost remains the same unless the number of employees changes. This type of plan eliminates administrative duties and expenses for the employer, as the insurance carrier takes the lead in providing administrative services and dealing with all employee claims.

The employer and insurance carrier negotiate a set monthly premium at the beginning of the plan year, which is based on the employer's unique workforce and the insurer's fees. This premium then remains constant throughout the year, providing stability and predictability for the employer. The insurance company pays medical claims based on the benefit outline, and employees must pay any deductibles or copays required for covered healthcare services under the policy.

Fully insured plans offer financial protection and are subject to state and federal insurance regulations. They are a good choice for employers who want to provide quality health benefits to their employees but may not have the time or resources to manage the process themselves. These plans allow employers to outsource the responsibility of meeting legal requirements and handling administrative tasks to the insurance carrier.

While fully insured plans offer financial predictability and stability, they may also come with higher costs. Employers should carefully consider their options and choose the best type of plan for their specific needs and circumstances.

Meeting Medical Deductibles: Strategies to Reduce Out-of-Pocket Expenses

You may want to see also

Explore related products

![]()

Reduced financial risk: the insurance company assumes responsibility for providing health coverage, protecting employers from large claims

A fully insured plan is a group health plan where employers purchase coverage directly from an insurance company. This is the traditional approach to employee benefits, where employers pay a fixed premium to a health insurance carrier for their employees' medical expenses. The premium rates are fixed annually based on the number of enrolled employees and will only change if the number of employees changes. This offers financial predictability and helps companies stay on budget.

In a fully insured plan, the insurance company assumes responsibility for providing health coverage, protecting employers from large claims. This means that when employees use their benefits and have health care claims, the carrier pays for them, instead of the employer. The fiscal responsibility and risk are on the carrier, and they also manage the administrative burden and compliance requirements. This reduces the financial risk for employers, as they are protected from the risk of large and catastrophic claims.

The insurance company pays medical claims based on the benefit outline, and employees must pay any deductibles or copays required for covered healthcare services under the policy. While this option may be more expensive, it is popular among small businesses as it eliminates the administrative duties and expenses related to a self-insured health plan. It also offers predictability and allows companies to stay on budget.

With a fully insured plan, employers can choose from a variety of off-the-shelf benefits packages and hand off the administrative burden to the carrier. This is especially useful for small businesses that are busy managing day-to-day operations and may not have the time or personnel to manage the process themselves.

Overall, a fully insured health plan can provide reduced financial risk for employers by transferring the responsibility of claims payments to the insurance carrier.

Top PPO Medical Insurance Plans: Best Options for You

You may want to see also

Explore related products

$8

![]()

Administrative relief: the insurance carrier takes the lead in providing administrative services, reducing the burden on employers

A fully insured medical plan is a traditional approach to employee benefits. Employers pay a fixed premium to a health insurance carrier for their employees' medical expenses. This premium is based on the number of enrolled employees and will only change if the number of employees changes. The insurance company then pays the medical claims, and the employees must pay any deductibles or copays required for covered healthcare services.

The insurance carrier takes the lead in providing administrative services, reducing the burden on employers. This means that the carrier manages the administrative burden and compliance requirements, in addition to claims' payments. Services include open enrollment and claims processing. This allows employers to stay on budget, as the cost remains the same unless the number of employees or other factors change. It also eliminates the administrative duties and expenses related to a self-insured health plan, as the health insurance company deals with all claims of employees.

For example, with a fully insured plan, employers can choose from a variety of off-the-shelf benefits packages, offer them to their employees, and hand off the administrative burden to the carrier. This is in contrast to a self-insured plan, in which the employer collects premiums from enrollees and pays the claims, with an insurance company simply administering the coverage.

A fully insured plan may be a good choice if employers don't have the staff, resources, or expertise to manage healthcare benefits on their own. This is especially the case for small businesses, which may be busy managing day-to-day operations and may not have the time to work with a broker or carrier on customising a health plan, let alone administer it effectively.

Appealing Insurance Claims: A Medical Office Guide

You may want to see also

Explore related products

![]()

Compliance: fully insured plans are subject to state and federal insurance regulations, and employers can outsource compliance requirements to the carrier

A fully insured medical plan is a traditional approach to employee benefits, where employers pay a fixed premium to a health insurance carrier for their employees' medical expenses. The insurance company assumes all responsibility for providing health coverage, including the cost, and the employer is protected from any large medical bills. This provides financial predictability for employers, as they pay a fixed premium price based on the number of enrolled employees, which only changes if the number of employees changes.

Compliance is a significant advantage of fully insured plans. These plans are subject to state and federal insurance regulations, and employers can outsource compliance requirements to the carrier. This means that the insurance carrier takes on the responsibility of meeting federal and state legal requirements, which can be a complex and time-consuming task for employers, especially small businesses that may not have the necessary staff, resources, or expertise to manage health care benefits on their own.

By outsourcing compliance, employers can ensure they are adhering to the relevant laws and regulations without having to navigate the complexities of insurance compliance themselves. This can provide peace of mind and reduce the risk of non-compliance, which could result in legal and financial consequences.

Additionally, fully insured plans offer protection from financial risk. In this model, the insurance company bears the fiscal responsibility and risk, paying for employees' health care claims instead of the employer. This shields employers from potentially catastrophic claims that could result in enormous medical bills.

While fully insured plans offer compliance benefits and financial predictability, they may also come with higher costs. Employers should carefully consider their specific circumstances, including their risk tolerance and resources, when deciding between a fully insured plan and other options, such as self-insured plans.

Malpractice Insurance: Are You Covered for Past Claims?

You may want to see also

Frequently asked questions

A fully insured medical plan is a traditional type of insurance option sponsored by an employer. The employer pays a fixed premium to an insurance company, which covers their employees' medical claims.

A fully insured medical plan offers financial predictability and lowers financial risk for the employer as the insurance company assumes responsibility for providing health coverage and dealing with claims. It also eliminates the administrative burden for the employer.

Fully insured medical plans can be more expensive and rigid due to a lack of customization options. The insurance company also keeps any leftover money from premiums that aren't spent on claims.