Home insurance is a necessary cost that can add hundreds of dollars to your budget each month. The cost of homeowners insurance is highly individualized, and many factors go into calculating your rates. These include the location of your home, the coverage you are purchasing, and the deductible you choose. To get a good estimate of the cost of homeowners insurance, you can use online tools and calculators that take into account factors such as your address, ZIP code, credit score, dwelling coverage, and deductible preference. Comparing quotes from multiple companies will help you find the most competitive rates and affordable coverage for your needs.

| Characteristics | Values |

|---|---|

| Average annual cost | $1,678 |

| Average monthly cost | $198 |

| Average annual cost (with $350,000 in dwelling coverage, $175,000 for personal property coverage and $100,000 in liability coverage) | $2,377 |

| Personal property coverage | Pays to repair or replace belongings |

| Dwelling coverage | Pays to rebuild or repair your house |

| Liability coverage | Provides financial protection in case of injury or property damage |

| Factors affecting cost | Location, credit score, deductible, claims history, construction year, liability concerns, natural disaster history |

| Discounts | Bundling insurance, multiple insurance types |

Explore related products

What You'll Learn

![]()

Home insurance calculators

Location is a significant factor in determining home insurance premiums. Insurance companies consider the natural disaster history of an area, as well as the proximity of a home to emergency services, when calculating rates. For example, homeowners in high-risk areas for climate-related perils may pay significantly more in premiums than those in lower-risk regions.

Credit score is another important consideration. In most states, an insurer can use an individual's credit history when setting their insurance rate. A higher credit score generally translates to a better insurance credit tier and a lower premium.

Dwelling coverage, or Coverage A, is crucial as it determines how much it would cost to completely rebuild a home in the event of a total loss. Insurance companies often calculate other coverage limits as a percentage of dwelling coverage. For instance, personal property coverage, or Coverage C, is usually set at a percentage of dwelling coverage, insuring belongings in the event of damage or destruction.

The deductible is the amount a policyholder agrees to cover out of pocket in the event of a claim. A higher deductible can lead to a lower premium, while a lower deductible may result in a higher premium but lower out-of-pocket expenses in the case of a claim.

Claims history is also a factor in determining insurance rates. A property with a history of recurring issues may be deemed higher risk and therefore more expensive to insure.

It is worth noting that home insurance calculators provide estimates, and actual insurance quotes may differ. It is recommended to compare quotes from multiple carriers to find the most competitive rate and ensure adequate coverage without overpaying.

Home Insurance: How Much Coverage Do You Need?

You may want to see also

Explore related products

![]()

How location affects insurance costs

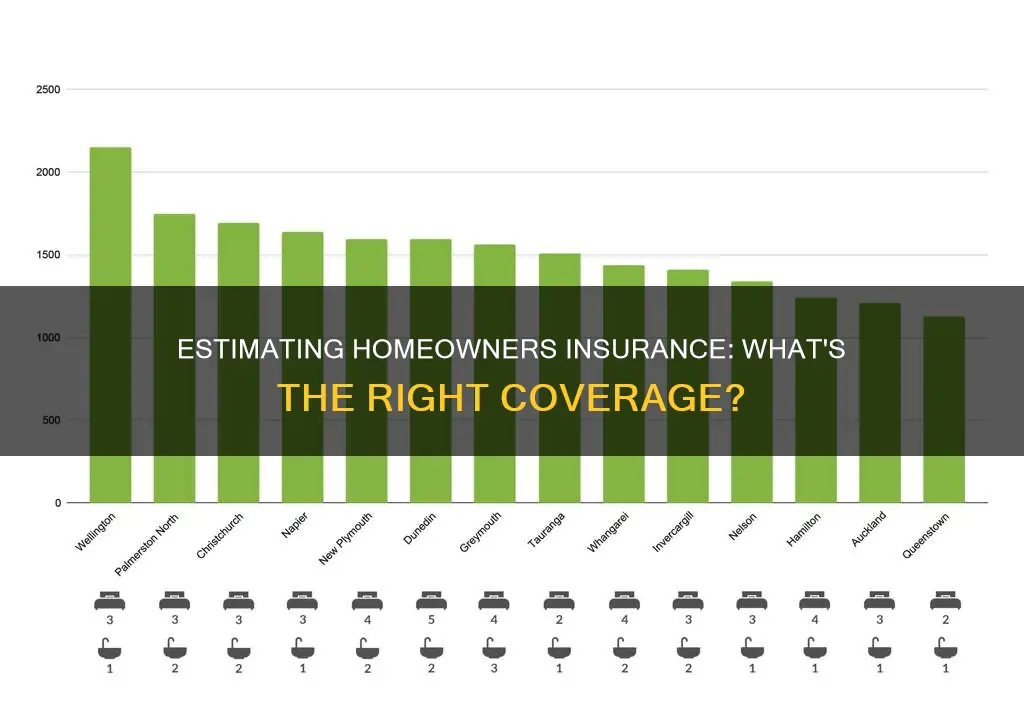

The location of your home is one of the biggest factors that insurers use to determine homeowners insurance premiums. If you live in an area that is prone to natural disasters like hurricanes, tornadoes, or wildfires, you will pay more for homeowners insurance since the risk of insuring your home is higher. For example, the average cost of home insurance in Oklahoma, which is prone to tornadoes, is $4,623 per year, while the average cost in Alaska, which had one recorded tornado in 2024, is $942 for the same amount of dwelling coverage. Policy rates also tend to be higher in cities than in suburban or rural areas, as homes typically cost more to build in densely populated areas.

Insurers will also consider your ZIP code and proximity to fire stations or fire hydrants. If your home is more than five miles away from a fire station, you may pay more for insurance. On the other hand, if your home is within 100 feet of a fire hydrant, you may receive lower rates.

Location also affects insurance costs in terms of property crime rates in your ZIP code. If your neighborhood experiences frequent home break-ins, vandalism, or theft, you will likely pay higher rates.

The cost of rebuilding your home, or replacement cost, is another important factor that is influenced by location. This is because construction costs, including labor and materials, may vary depending on the region. For example, the cost of rebuilding a home in an area with high local building costs will be higher, which will be reflected in higher insurance premiums.

Finally, location can also impact insurance costs through factors such as the age and construction materials of your home. Older homes may have outdated electrical, plumbing, and heating systems that are more prone to issues and may need updating, driving up insurance costs. Additionally, homes built with certain materials, such as fire-resistant materials, may have lower premiums than those constructed with more flammable materials.

San Jose Homeowners Insurance: What's the Cost?

You may want to see also

Explore related products

![]()

Discounts and how to reduce costs

The cost of homeowners insurance is influenced by factors such as location, age of the home, and coverage limits. While these factors are beyond one's control, there are several strategies to reduce premiums and make coverage more affordable. Firstly, it is essential to understand your current policy's coverage and exclusions to avoid paying for unnecessary insurance. Review the declarations page, which summarises your coverage, and the exclusions page to identify any gaps.

Next, consider the cost of repairs or issues that would lead to a claim. Increasing your deductible, the amount you pay when making a claim, can lower your premium. For instance, if your deductible is $1,000, increasing it to $2,500 could save you an average of 12% annually. However, ensure your deductible doesn't exceed what you can afford out of pocket.

Additionally, establish a solid credit history by paying bills on time, maintaining low credit balances, and regularly checking your credit record for accuracy. Poor credit can significantly increase insurance costs.

You can also reduce costs by bundling policies. Purchase multiple types of insurance, such as home and auto, from a single carrier, or buy multiple policies from companies offering homeowners, auto, and liability coverage. Long-term policyholders may also receive discounts from their insurers.

Finally, consider making your home more resistant to natural disasters. Adding storm shutters, reinforcing your roof, or investing in stronger roofing materials can lead to savings on premiums. Modernising heating, plumbing, and electrical systems can also reduce the risk of fire and water damage, making your home less risky and costly to insure.

Pest Damage to Ducts: Is Homeowner's Insurance Your Savior?

You may want to see also

Explore related products

$7.2 $8

![]()

What is covered and what is not

Homeowners insurance covers your home's physical structure and contents, safeguarding against perils like falling objects, fire or theft. It also offers liability protection in case someone gets injured on your property. The coverage specifics, however, can vary depending on the policy.

What is covered

Homeowners insurance typically covers a broad range of possible damages to your home and other structures on the property, such as a garage, fence, driveway, or shed. It also covers personal belongings and liability protection in case someone gets injured on your property or their property is damaged. Trees, plants, and shrubs are also generally covered, with a limit of about $500 per item. Liability covers you against lawsuits for bodily injury or property damage caused by you, your family members, or your pets. It pays for both the cost of defending you in court and any court awards, with liability limits generally starting at about $100,000.

Your policy may also include coverage for smoke damage, damage caused by falling items, or severe winds. If your home is damaged by a covered peril, such as fire, theft, or severe weather, homeowners insurance can help cover the costs of repairs or replacement. If your home is damaged by a covered peril and you cannot live there while it is being repaired or rebuilt, your policy may also cover additional living expenses such as hotel stays, rentals, dining out, laundry services, and transportation costs.

What is not covered

Homeowners insurance does not cover damage caused by floods, earthquakes, or other natural movements of the earth. It also does not cover war, nuclear accidents, or any willful loss or damage caused by you or your family members. Basic maintenance and wear and tear are also typically not covered. Certain high-value items, such as jewelry or artwork, may have limited coverage, and you may need additional coverage for these assets. Homeowners insurance also does not typically cover a separate structure on your property used for running a business.

Smart Watch Insurance: Is It Worth It?

You may want to see also

Explore related products

![]()

Liability and risk factors

Home insurance rates are a calculation of risk. If your insurance company deems you likely to file a claim or experience a loss due to a covered peril, you will likely pay more than average. The location of your home is one of the biggest factors in determining your home insurance premiums. If you live in an area prone to natural disasters like hurricanes, tornadoes, or wildfires, you will pay more for homeowners insurance since the risk of insuring your home is higher. Policy rates tend to be higher in cities than in suburban or rural areas, as homes typically cost more to build in densely populated areas. When it comes to location, insurers will also consider your ZIP code and proximity to fire stations or fire hydrants. If your home is less than 100 feet from either, you may receive lower rates. Property crime rates in your ZIP code can also influence your rates. If your neighbourhood experiences frequent home break-ins, that could result in higher rates.

The replacement cost of your home is the biggest factor in calculating home insurance rates. It is based on the cost to rebuild your home, including the construction type of your home and the cost of construction materials and labour. The age of your home is also a factor, as older homes are more likely to have outdated safety features, plumbing, and electrical systems. The age and condition of your roof can also significantly impact your policy premiums. A newer roof has a greater likelihood of protecting your home against the elements than an older roof.

Risk factors specific to your home or the area around it can increase your home insurance rates. These include a swimming pool, playground equipment, a trampoline, a diving board, a wood stove, or certain dog breeds. These features are considered "attractive nuisances" or liability risks. You may be required to install secure barriers, such as an automatic locking gate around your swimming pool or a fence of a certain height to decrease your liability risk.

Personal factors about you as a homeowner can also affect your rates. Your credit history, for example, is a factor that insurance companies use to calculate your rates. While your insurance company can offer you discounts, you cannot haggle on the rate, as home insurance rates are regulated by the state.

Domestic and General Insurance: Worth the Cost?

You may want to see also

Frequently asked questions

Home insurance calculators can provide an estimate of your insurance costs. You can use these by entering your address, or ZIP code, and making adjustments to the property details for a more precise result.

The cost of insurance is influenced by the location of your home, the level of coverage you require, and the level of risk. For example, homeowners in the top 20% of ZIP codes at the highest risk of climate-related perils pay 82% more in premiums compared to those in the lowest-risk areas. Other factors include the construction year of your home, your credit history (except in California, Maryland, and Massachusetts), and your deductible.

You can reduce costs by raising your deductible, although this means you will pay more out of pocket in the event of a claim. You can also save money by bundling your home and auto insurance, and shopping around for quotes from multiple companies.