Loss ratios are used to evaluate the financial health and profitability of insurance companies. They represent the ratio of losses to premiums earned, with losses including paid insurance claims and adjustment expenses. A good loss ratio for an insurance company is one that is low, as this indicates higher profitability. For example, a loss ratio of 60% or above is considered bad, 30-60% is average, and 0-30% is great. In the context of medical insurance companies, the Affordable Care Act (ACA) has established minimum medical loss ratio (MLR) standards, requiring health insurers to spend at least 80% or 85% of premium revenues on clinical care and quality improvements, with the aim of restraining premium growth and limiting profits and administrative costs.

| Characteristics | Values |

|---|---|

| Loss ratio calculation | ((insurance claims paid + loss adjustment expenses)/premium earned) x 100 |

| Loss ratio interpretation | A lower ratio indicates higher profitability for the insurance company |

| Good loss ratio | 0-30% is considered a great loss ratio |

| Break-even loss ratio | 60% is typically the carrier's break-even point for losses |

| Bad loss ratio | 60% and above is considered a bad loss ratio |

| Medical Loss Ratio (MLR) minimum | 75% for Group insurance and 65% for Individual insurance |

| MLR minimum under Affordable Care Act (ACA) | 80% for individual and small group markets, 85% for large group markets |

Explore related products

What You'll Learn

![]()

Loss ratio calculation

Loss ratios are used in the insurance industry to assess the financial health and profitability of an insurance company. It is calculated by dividing the sum of insurance claims paid and adjustment expenses by the total earned premiums. Adjustment expenses refer to the expenses needed to validate the claims.

For example, if a company pays out $80 in claims for every $160 in collected premiums, the loss ratio would be 50%. Loss ratios above 100% indicate that the insurance company has paid out more in claims than they have earned in premiums. A high loss ratio may be a sign of financial distress, especially for property or casualty insurance companies.

The Affordable Care Act (ACA) mandates that health insurance carriers allocate a significant share of premiums to clinical services and the improvement of healthcare quality. Health insurance providers are required to divert 80% of premiums to claims and activities that improve the quality of care. If they fail to do so, they must issue rebates to their policyholders. The minimum Medical Loss Ratio (MLR) for Medicare Supplement (Medigap) insurance differs, with commercial for-profit insurers requiring a minimum MLR of 75% for group insurance and 65% for individual insurance.

Benefit-expense ratios are related to loss ratios, comparing an insurer's expenses for acquiring, underwriting, and servicing a policy with the net premium charged. Expenses can include employee wages, agent and broker commissions, advertising, legal fees, and other general and administrative expenses. Insurers will also calculate their combined ratios, which include the loss ratio and the expense ratio, to measure total cash outflows associated with their operating activities.

Adding Sick Father to My Medical Insurance: Is it Possible?

You may want to see also

Explore related products

![]()

Loss ratio and profitability

Loss ratios are used in the insurance industry to assess the financial health and profitability of a company. It is calculated by dividing the total paid in insurance claims and adjustment expenses by the total earned premiums. Loss ratios are represented as a percentage. For example, if a company pays out $80 in claims for every $160 in collected premiums, the loss ratio would be 50%.

A high loss ratio can indicate financial distress, especially for property or casualty insurance companies. Conversely, a low loss ratio indicates higher profitability. A loss ratio of 60% is typically the break-even point for insurance carriers, with 30-60% being average to slightly above average, and 0-30% being excellent. When the loss ratio exceeds 100%, the insurance company has paid out more in claims than they have earned in premiums, and they may decide to increase premiums or cancel the policy.

In the context of medical insurance companies, the loss ratio is referred to as the Medical Loss Ratio (MLR). The Affordable Care Act (ACA) established minimum MLR standards for private market health plans and insurers, requiring them to spend at least 80% or 85% of premium revenues on medical care and quality improvements, depending on the market. Commercial for-profit insurers must meet a minimum MLR of 75% for group insurance and 65% for individual insurance.

The MLR is important because it is used to assess the reasonableness of premiums and to ensure that insurers are not overcharging customers. Regulators may require insurers to refund policyholders if the MLR falls below the minimum standard. A good loss ratio can help reduce future insurance premiums, as it gives the insured individual or entity more negotiating power.

Understanding Private Medical Insurance Tax Implications

You may want to see also

Explore related products

![]()

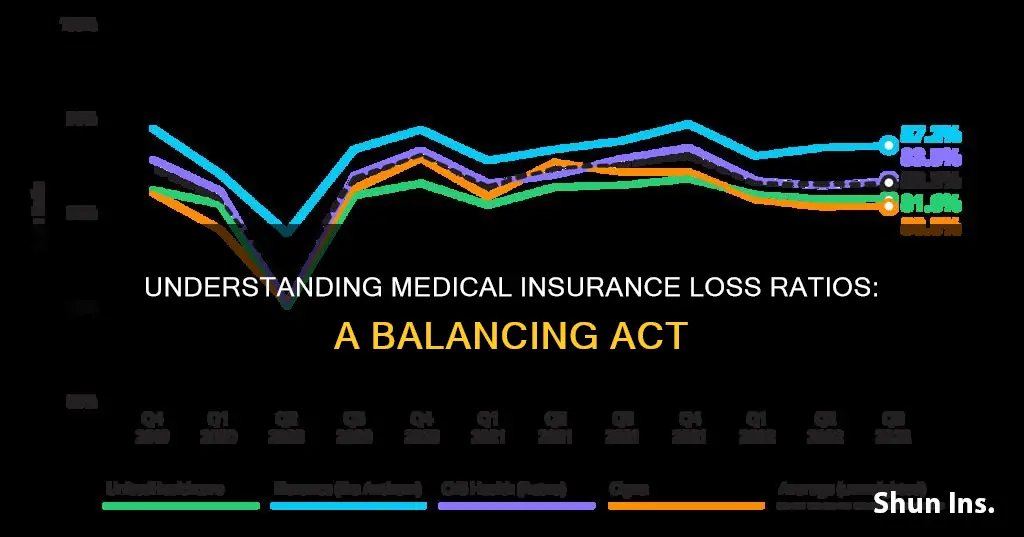

Loss ratio and the Affordable Care Act

The Affordable Care Act (ACA) has introduced several provisions that change the way private health insurance is regulated, with the aim of providing better value to consumers and increasing transparency. One of these provisions is the Medical Loss Ratio (MLR) requirement, which limits the proportion of premium income that health insurers can spend on administration, marketing, and profits. This ratio is calculated by dividing the insurance claims paid and adjustment expenses by the total earned premiums.

The MLR requirement under the ACA mandates that insurance companies spend a minimum of 80% of their premium income on healthcare claims and quality improvement, leaving the remaining 20% for administration, marketing, and profit. This is also known as the 80/20 rule. The threshold is higher for large group plans, which must allocate at least 85% of premium dollars to healthcare and quality improvement. This provision ensures that a significant portion of the premium income is directed towards clinical services, improving healthcare quality, and offering more value to plan participants.

Prior to the ACA, many states had varying medical loss ratio requirements and reporting standards in place. The ACA's MLR provision introduced a standardised and more stringent requirement across the nation. This provision promotes transparency by requiring health insurers to publicly disclose the portion of premium dollars spent on healthcare, quality improvement, and other activities in each state they operate. This information helps consumers understand how their premium payments are utilised and allows them to assess the value and reasonableness of premiums.

The ACA also introduced rebates to consumers if insurers fail to meet the applicable MLR standards. Beginning in 2012, health insurance issuers have been mandated to issue rebates to enrollees if the percentage of premium revenues spent on clinical services and quality improvement does not meet the minimum standards set by the ACA. This ensures that insurance companies remain accountable and prioritises consumer protection.

The MLR provision of the ACA has had varying levels of compliance across different markets. While the majority of insurers with credible claims experience would have met or exceeded the MLR rebate standard if it had been in effect earlier, less than half of the insurers in the individual market met the standard in 2010, compared to 70% in the small group market and 77% in the large group market.

VA Medical Benefits: Can Your Partner Be Covered?

You may want to see also

Explore related products

![]()

Loss ratio and premium increases

Loss ratios are used in the insurance industry to assess the financial health and profitability of an insurance company. It is calculated by dividing the total incurred losses by the total collected insurance premiums. The lower the ratio, the more profitable the insurance company, and vice versa. A high loss ratio can be an indicator of financial distress, especially for a property or casualty insurance company.

The loss ratio formula is insurance claims paid plus adjustment expenses divided by total earned premiums. For example, if a company pays $80 in claims for every $160 in collected premiums, the loss ratio would be 50%.

In the context of medical insurance companies, the loss ratio is referred to as the Medical Loss Ratio (MLR) or medical cost ratio (MCR). The Affordable Care Act (ACA) requires health insurance issuers to submit data on the proportion of premium revenues spent on clinical services and quality improvement (i.e. the MLR). The ACA mandates that health insurance carriers allocate a significant share of the premium to these areas. Specifically, health insurance providers are required to divert 80% of premiums to claims and activities that improve the quality of care. If they fail to do so, they will have to issue a rebate to their policyholders.

The MLR is important because it is used as a measure of the reasonableness of premiums. If the MLR is below the minimum standard, the relevant department may have the authority to order corrective action, including refunds to policyholders.

If loss ratios associated with a policy become excessive, an insurance provider may raise premiums or choose not to renew a policy. Carriers may review claims history and loss ratios for the past five years to determine if and by how much a premium increase is warranted. However, it is important to note that the loss ratio is not the only factor used to determine whether a proposed premium is reasonable.

Insurance Records and Medical Copy Fees: What's the Link?

You may want to see also

Explore related products

![]()

Loss ratio and refunds

Loss ratios are used in the insurance industry to assess the health and profitability of an insurance company. The ratio represents the ratio of losses to premiums earned. Losses include paid insurance claims and adjustment expenses. A high loss ratio may indicate that a business is in financial distress.

The Affordable Care Act (ACA) established the first minimum medical loss ratio (MLR) standard for many private market health plans and insurers. The MLR is a comparison of how much of a premium goes towards paying medical claims versus how much the insurer pays for administrative costs and profits. For example, an 82% MLR means that 82% of the premiums paid by policyholders go towards paying claims, while the remaining 18% is kept by the insurer for administrative expenses and profits.

The ACA requires health insurance issuers to submit data on the proportion of premium revenues spent on clinical services and quality improvement, also known as the MLR. The ACA also mandates that insurance companies spend at least 80% or 85% of premium dollars on medical care. For the large group market, the MLR requirement is 85%, while for commercial for-profit insurers, the minimum MLR for Medicare Supplement (Medigap) insurance is 75% for Group insurance and 65% for Individual insurance.

If the MLR is below the minimum standard, insurance companies are required to issue rebates to enrollees. This is done to restrain premium growth by limiting the profits and administrative costs of health insurers. The rebates provide refunds to policyholders and ensure that a significant share of the premium is allocated to clinical services and the improvement of healthcare quality.

Tooth Extraction: Is Medical Insurance Coverage Guaranteed?

You may want to see also

Frequently asked questions

Loss ratio is a metric used to evaluate the financial health and profitability of an insurance company. It represents the ratio of losses to premiums earned. Losses include paid insurance claims and adjustment expenses. A high loss ratio can indicate financial distress, especially for property or casualty insurance companies.

Generally, a lower loss ratio indicates higher profitability for an insurance company. For medical insurance companies specifically, a loss ratio of 60% or above is considered bad, 30-60% is average to slightly above average, and 0-30% is great. The Affordable Care Act (ACA) mandates that health insurance carriers allocate a significant portion of premiums to clinical services and quality improvement, with a minimum loss ratio requirement of 80% for individual and small group markets and 85% for the large group market.

A good loss ratio is essential for obtaining lower insurance premiums. If the loss ratio is high, indicating financial distress, insurance providers may increase premiums or choose not to renew policies. Conversely, a low loss ratio gives more negotiating power to the policyholder.