Guaranteed issue rights are protections for Medicare enrollees in certain situations, allowing them to obtain Medicare Supplement Insurance plans, also known as Medigap plans, without facing medical underwriting or coverage denials based on health conditions. These rights are typically triggered during specific periods, such as the initial six-month Medigap Open Enrollment Period when individuals turn 65 and enroll in Medicare Part B. During this time, insurance companies are required to offer Medigap policies at their best available rates, regardless of the individual's health status. Outside of this enrollment period, individuals may be subject to medical underwriting, higher premiums, or even rejection based on their health history and pre-existing conditions. Therefore, understanding guaranteed issue rights is crucial for individuals to effectively navigate Medicare and secure comprehensive healthcare coverage.

| Characteristics | Values |

|---|---|

| Definition | Guaranteed-issue rights are protections for Medicare enrollees in certain situations. |

| Protection | Guaranteed-issue rights prevent insurance companies from denying enrollment in certain Medigap policies when beneficiaries meet specific criteria. |

| Medical underwriting | Guaranteed-issue rights may protect you from medical underwriting. Health insurance companies often use your health history and data on pre-existing conditions to make determinations about whether or not they will cover you and how much they will charge you for coverage. |

| Eligibility | Eligibility for Medicare Supplement Insurance plans is granted during specific circumstances, providing individuals with the opportunity to enroll without facing medical underwriting or coverage rejections. |

| Enrollment period | The six-month Medigap Open Enrollment Period starts when you turn 65 and are enrolled in Medicare Part B. |

| Timeframe | Each situation has a defined timeframe, and missing these windows might lead to the loss of guaranteed issue rights. |

| Examples | Losing employer-sponsored health coverage, moving out of your coverage area, or losing a Medicare Advantage plan. |

Explore related products

What You'll Learn

- Guaranteed issue rights protect you from medical underwriting

- You can enrol in any Medigap policy during the Medigap Open Enrollment Period

- Guaranteed issue rights are triggered by specific events or changes in health coverage

- Guaranteed issue rights are similar to SEPs, ensuring access to certain Medicare plans

- Guaranteed issue rights are also known as Medigap protections

![]()

Guaranteed issue rights protect you from medical underwriting

Guaranteed issue rights are an essential protection for individuals seeking Medicare Supplement Insurance plans, also known as Medigap plans. These rights ensure that during specific periods, individuals can obtain Medigap policies without undergoing medical underwriting or facing coverage denials based on their health status. Understanding how guaranteed issue rights protect you from medical underwriting is crucial for effectively securing healthcare coverage.

Medical underwriting is a process used by health insurance companies to assess your health history, current health, and pre-existing conditions to determine coverage eligibility and premium costs. During medical underwriting, insurers may deny coverage or charge higher premiums to individuals deemed to have higher health risks. However, guaranteed issue rights provide a safety net, allowing individuals to make necessary coverage adjustments without worrying about medical underwriting.

There are two primary scenarios that grant individuals guaranteed issue rights and protect them from medical underwriting. The first is the Medigap Open Enrollment Period, which lasts for six months and begins when an individual turns 65 and enrols in Medicare Part B. During this period, insurance companies must offer Medigap policies without considering health status or charging higher premiums based on health. This ensures that individuals can obtain coverage regardless of their medical history.

The second scenario involves specific events or changes in health coverage that trigger guaranteed issue rights. These events include losing employer-sponsored health coverage, moving out of your coverage area, or experiencing the loss of your previous Medicare supplement coverage due to circumstances beyond your control. In these situations, individuals gain the right to purchase a Medicare supplement plan without undergoing medical underwriting. It is important to note that these rights are typically associated with defined timeframes, and missing these windows may result in the loss of guaranteed issue rights.

Additionally, guaranteed issue rights provide protections beyond avoiding medical underwriting. When individuals enrol during their guaranteed issue right period, insurance companies cannot deny coverage or charge higher premiums based on pre-existing health conditions. This ensures that individuals with pre-existing health issues are not discriminated against and can obtain the coverage they need.

In conclusion, guaranteed issue rights play a vital role in protecting individuals from medical underwriting when applying for Medicare Supplement Insurance plans. By understanding and utilizing these rights, individuals can secure coverage without worrying about their health history or pre-existing conditions impacting their eligibility or premium costs. These protections ensure that healthcare remains accessible and affordable for those who need it, providing peace of mind during crucial life moments.

Retiree Medical Insurance: What's the Plan for Young Retirees?

You may want to see also

Explore related products

![]()

You can enrol in any Medigap policy during the Medigap Open Enrollment Period

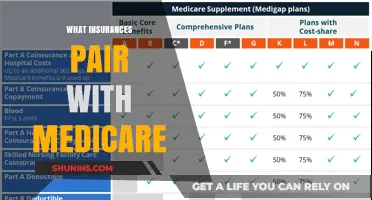

Understanding the enrolment process for Medicare Supplement Insurance plans, also known as Medigap plans, is crucial to ensure you have the best coverage for your healthcare needs. One of the primary eligibility scenarios for enrolling in a Medigap plan is during the Medigap Open Enrollment Period (OEP). This period offers a valuable opportunity for individuals to secure comprehensive coverage while minimising barriers related to health status.

The Medigap Open Enrollment Period is a six-month window that begins when you turn 65 and enrol in Medicare Part B. During this time, you are guaranteed the right to enrol in any Medigap policy of your choosing, without undergoing medical underwriting or facing coverage denials based on health conditions. Medical underwriting refers to the process where insurance companies evaluate your medical history, current health, and other factors to determine coverage eligibility and premium costs. By law, during the Medigap Open Enrollment Period, insurance companies must offer Medigap policies at their best available rates, without considering your health status, past or present.

It is important to note that the Medigap Open Enrollment Period is a one-time opportunity and does not repeat annually like the Medicare Open Enrollment Period. Therefore, it is crucial to take advantage of this window to enrol in the Medigap policy that best suits your needs. During this period, you can expect better prices and more choices among policies, as insurance companies cannot deny you coverage or charge higher premiums based on pre-existing health conditions.

Additionally, it is worth mentioning that some states have further guaranteed issue protections beyond the federal minimum rules. For example, in certain states, individuals who lose Medicaid due to changes in their financial situation have a guaranteed issue right to buy a Medicare supplement policy without underwriting. Therefore, it is advisable to check with your State Insurance Department to understand your specific rights and protections regarding Medigap enrolment outside of the standard Medigap Open Enrollment Period.

In summary, the Medigap Open Enrollment Period provides a crucial window during which you can enrol in any Medigap policy of your choice without facing medical underwriting or coverage rejections. This period ensures that individuals have access to comprehensive healthcare coverage, regardless of their health status or history. By understanding the eligibility criteria and taking advantage of this enrolment period, you can secure the Medigap plan that best meets your healthcare needs.

Retirement Medical Insurance: Understanding Post-Retirement Insurance Costs

You may want to see also

Explore related products

![Medicare and Social Security: [5 in 1] Maximize Your Retirement Benefits, Secure Medical Coverage and Quality Healthcare | Proven Strategies to Protect Your Financial Future Avoiding Costly Mistakes](https://m.media-amazon.com/images/I/71sRJGiWeQL._AC_UL320_.jpg)

![]()

Guaranteed issue rights are triggered by specific events or changes in health coverage

Guaranteed issue rights are a crucial protection for Medicare enrollees, ensuring they can obtain specific Medicare plans, like Medigap policies, without facing medical underwriting or coverage denials based on their health status. These rights are triggered by specific events or changes in health coverage, providing a safety net during crucial life moments. Understanding these rights is essential for effectively navigating Medicare and securing appropriate healthcare coverage.

One common trigger for guaranteed issue rights is the loss of health insurance through no fault of your own, such as the loss of employer-sponsored coverage or the termination of your previous insurance provider's certification to sell their plan. If you lose your health insurance due to circumstances beyond your control, you may be eligible for guaranteed issue rights, allowing you to purchase a Medicare supplement plan without underwriting. This ensures that you can secure new coverage without being penalized for pre-existing health conditions.

Moving out of your coverage area can also trigger guaranteed issue rights. Medicare Advantage plans, for example, are specific to your residential area, so if you move outside of the plan's service area, you will lose that coverage. In such cases, you are granted guaranteed issue rights to purchase a Medicare supplement plan in your new area without undergoing medical underwriting. This allows for a seamless transition to a new healthcare plan, regardless of your health history.

Additionally, guaranteed issue rights may be triggered by certain trial rights associated with Medicare Advantage plans. If you enroll in a Medicare Advantage plan when you first become eligible for Medicare at 65, you have the right to change your mind within 12 months. During this trial period, you can return to Original Medicare and purchase a Medicare supplement plan, and the insurance company cannot deny you coverage. Similar trial rights exist if you switch from Original Medicare and a Medigap plan to a Medicare Advantage plan for the first time.

It is important to note that guaranteed issue rights are time-sensitive, and missing the designated windows may result in the loss of these rights. Therefore, it is crucial to be aware of the specific circumstances that trigger guaranteed issue rights and to act promptly to secure the necessary coverage adjustments. By understanding and utilizing guaranteed issue rights effectively, individuals can ensure they have the best coverage to meet their healthcare needs.

Covid Test Kits: Are They Covered by Medical Insurance?

You may want to see also

Explore related products

![]()

Guaranteed issue rights are similar to SEPs, ensuring access to certain Medicare plans

Guaranteed issue rights are periods during which individuals can obtain certain Medicare plans, such as Medigap policies, without facing medical underwriting or coverage denials based on health conditions. These rights are triggered by specific events or circumstances, such as losing employer-sponsored health coverage, moving out of your coverage area, or having original Medicare and a Medigap plan and then switching to a Medicare Advantage plan.

During these designated periods, individuals can be confident that they can make necessary coverage adjustments without worrying about medical underwriting. This process, known as medical underwriting, involves health insurance companies using an individual's health history and data on pre-existing conditions to determine coverage eligibility and premium costs. By avoiding medical underwriting, guaranteed issue rights ensure that individuals cannot be denied coverage or charged higher premiums based on their health status.

Similar to guaranteed issue rights, Special Enrollment Periods (SEPs) also allow individuals to obtain certain Medicare plans without facing medical underwriting. These periods are triggered by specific events, such as losing health insurance through no fault of your own or moving out of your coverage area. Understanding the synergy between SEPs and guaranteed issue rights is crucial for effectively navigating Medicare and securing appropriate healthcare coverage.

Both SEPs and guaranteed issue rights provide a comprehensive safety net, ensuring access to specific Medicare plans regardless of health status or timing. These rights and protections are essential for individuals who need to make necessary coverage adjustments during crucial life moments. By recognizing and utilizing these rights, individuals can navigate the complex world of Medicare with greater confidence and security.

In conclusion, guaranteed issue rights and SEPs play a crucial role in ensuring that individuals have access to the healthcare coverage they need. By providing protection from medical underwriting and coverage denials, these rights offer a safety net that empowers individuals to make informed choices about their healthcare options during significant life changes. Understanding and effectively utilizing these rights are key steps towards securing comprehensive healthcare coverage through Medicare.

Medicaid and Irrevocable Life Insurance: What's the Deal?

You may want to see also

Explore related products

![The Medicare Bible for Beginners: [3 in 1] Unlock Medical Benefits and Quality Healthcare | Super Easy Insider Strategies to Navigate Medicare While Avoiding Costly Mistakes](https://m.media-amazon.com/images/I/71tm-tSiWnL._AC_UL320_.jpg)

![]()

Guaranteed issue rights are also known as Medigap protections

Guaranteed issue rights, also known as Medigap protections, are a set of rights that ensure individuals can obtain certain Medicare plans, such as Medigap policies, without facing medical underwriting or coverage denials based on health conditions. This means that during designated periods, individuals can be confident that they can make necessary coverage adjustments without worrying about their health status or timing. Understanding these rights is crucial for effectively navigating Medicare and securing appropriate healthcare coverage.

Medicare Supplement Insurance plans, or Medigap plans, are designed to fill in the gaps left by Original Medicare by paying for coinsurance, copayments, and some deductibles that Original Medicare does not cover. They also provide extended benefits in many cases. During specific circumstances, individuals are granted eligibility for Medigap plans, ensuring access regardless of health status. The primary eligibility scenarios include the Medigap Open Enrollment Period, which begins when an individual turns 65 and enrols in Medicare Part B, and specific events or changes in health coverage that trigger guaranteed issue rights.

The Medigap Open Enrollment Period is a six-month period during which individuals can enrol in any Medigap policy sold in their state. Insurance companies are required to offer these policies at their best available rates, without considering the individual's health status, past or present. This means that individuals cannot be charged higher premiums or denied coverage based on pre-existing health conditions during this period. It is important to note that the Medigap Open Enrollment Period is a one-time opportunity and does not repeat annually like the Medicare Open Enrollment Period.

Guaranteed issue rights are triggered by specific events or changes in health coverage. These can include losing employer-sponsored health coverage, moving out of the coverage area, or experiencing an involuntary loss of health insurance through no fault of the individual. In some cases, guaranteed issue rights can also be triggered by exercising a trial right or switching between different Medicare plans. It is important to be aware of the defined timeframes associated with these situations, as missing these windows may result in the loss of guaranteed issue rights.

Understanding the eligibility criteria and gathering the necessary documentation, such as a Medicare card, identification, and correspondence related to Medicare enrollment or existing health coverage, are crucial steps in navigating the process of enrolling in a Medicare Supplement Insurance plan with guaranteed issue rights. By familiarizing oneself with the available Medigap plans in their state and the differences in coverage, benefits, and costs, individuals can make informed decisions about their healthcare coverage.

Divorce and Medical Insurance: When Does Coverage End?

You may want to see also

Frequently asked questions

A guaranteed issue period for Medicare Supplement Insurance, also known as Medigap, is a period during which individuals can obtain certain Medicare plans without facing medical underwriting or coverage denials based on health conditions.

The guaranteed issue period for Medicare Supplement Insurance starts when you turn 65 and enroll in Medicare Part B. This period lasts for six months.

There are several situations that grant guaranteed issue rights for Medicare Supplement Insurance, including:

- Losing employer-sponsored health coverage

- Moving out of your coverage area

- Your previous insurance provider went bankrupt

- Your previous insurance provider was misleading or fraudulent