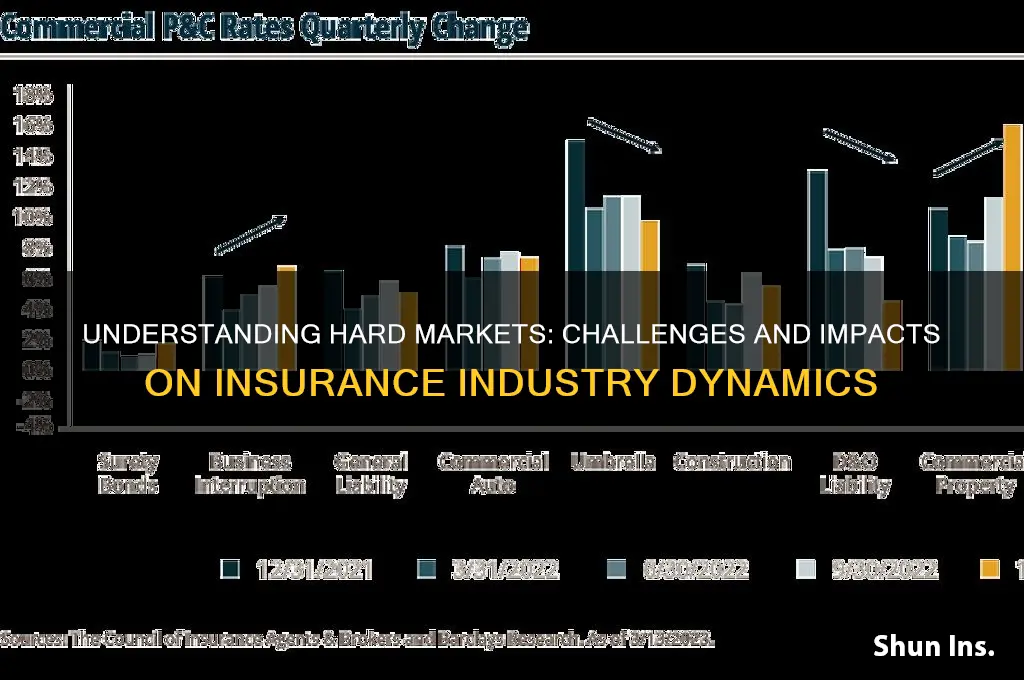

A hard market in insurance refers to a period characterized by higher premiums, stricter underwriting standards, and reduced availability of coverage, often driven by increased claims, rising costs, or economic uncertainties. During such times, insurers face challenges like catastrophic losses, inflation, or reinsurance constraints, prompting them to limit risk exposure and adjust pricing to maintain profitability. For policyholders, this translates to more expensive policies, fewer options, and potentially higher deductibles, making it essential to understand market dynamics and explore strategies to mitigate the impact of these conditions.

| Characteristics | Values |

|---|---|

| Definition | A hard market in insurance refers to a period when underwriting criteria tighten, premiums increase, and capacity (available coverage) decreases, making it more challenging for policyholders to obtain or renew insurance. |

| Premium Increases | Significant rises in insurance premiums across various lines of business (e.g., property, casualty, liability). |

| Underwriting Tightening | Stricter underwriting standards, including more rigorous risk assessments and exclusions. |

| Capacity Constraints | Reduced availability of coverage as insurers limit the amount of risk they are willing to take on. |

| Policy Non-Renewals | Higher instances of insurers declining to renew policies, especially for high-risk accounts. |

| Market Hardening Drivers | Increased claims frequency and severity, catastrophic losses (e.g., natural disasters), rising reinsurance costs, and low investment returns. |

| Duration | Typically lasts for multiple years, depending on market conditions and corrective actions by insurers. |

| Impact on Policyholders | Higher costs, reduced coverage options, and increased difficulty in securing insurance. |

| Recent Examples | The global insurance market has experienced hard market conditions since 2019, exacerbated by the COVID-19 pandemic, inflation, and climate-related losses. |

| Response Strategies | Risk mitigation, loss prevention, and working closely with brokers to find competitive coverage options. |

Explore related products

$15.95

$9.99 $19.99

What You'll Learn

- Definition: Hard market refers to a period of high premiums, strict underwriting, and limited capacity

- Causes: Driven by increased claims, catastrophic losses, or economic instability in the insurance sector

- Impact on Insureds: Higher costs, reduced coverage options, and stricter policy conditions for policyholders

- Duration: Typically cyclical, lasting 3-5 years before market conditions soften again

- Strategies for Insurers: Focus on risk selection, rate adequacy, and operational efficiency to remain profitable

![]()

Definition: Hard market refers to a period of high premiums, strict underwriting, and limited capacity

A hard market in insurance is a cyclical phase characterized by high premiums, strict underwriting, and limited capacity. During this period, insurers face increased costs and risks, prompting them to adopt more conservative approaches to policy issuance. Premiums rise significantly as insurers seek to offset higher claims payouts, reinsurance costs, or investment losses. Policyholders, particularly those in high-risk sectors or with poor loss histories, often experience substantial rate increases, making coverage more expensive and harder to obtain. This phase contrasts sharply with a soft market, where premiums are lower, underwriting is more lenient, and capacity is abundant.

Strict underwriting is a hallmark of a hard market. Insurers scrutinize risks more rigorously, applying tighter criteria to determine policy eligibility. This may include rejecting applications outright, excluding certain coverages, or imposing higher deductibles and lower limits. Underwriters focus on minimizing exposure to potential losses, often requiring additional risk mitigation measures from policyholders. For businesses and individuals, this means a more challenging application process and fewer options for customizing policies to meet their needs. The emphasis on risk reduction reflects insurers' efforts to protect their financial stability during uncertain economic or environmental conditions.

Limited capacity further defines a hard market, as insurers reduce the amount of risk they are willing to assume. This constraint can stem from factors such as catastrophic losses, regulatory changes, or economic downturns that strain insurers' resources. As a result, some insurers may exit certain lines of business entirely, while others may restrict the number of policies they issue. This reduction in available coverage options intensifies competition among policyholders, often leading to delayed renewals or rejections. Brokers and agents play a critical role in navigating this environment, helping clients find viable coverage solutions despite the constraints.

The causes of a hard market are multifaceted, often driven by external factors such as natural disasters, inflation, or legal trends that increase claims costs. For example, a series of hurricanes or wildfires can deplete insurers' reserves, prompting them to raise rates and tighten underwriting standards. Similarly, rising construction or medical costs can inflate the value of claims, further pressuring insurers' profitability. Economic conditions, such as high inflation or low investment returns, can also contribute to a hard market by reducing insurers' ability to offset losses through other revenue streams.

For policyholders, surviving a hard market requires proactive risk management and strategic planning. Businesses and individuals should focus on improving their risk profiles by implementing safety measures, maintaining accurate records, and demonstrating a commitment to loss prevention. Working closely with experienced brokers can help identify insurers still offering competitive terms and navigate the stricter underwriting process. Additionally, policyholders may need to explore alternative risk financing options, such as captive insurance or risk retention groups, to secure adequate coverage. While challenging, a hard market ultimately underscores the importance of resilience and adaptability in managing insurance needs.

Life Insurance Fraud: Time Limit on Legal Action

You may want to see also

Explore related products

![]()

Causes: Driven by increased claims, catastrophic losses, or economic instability in the insurance sector

A hard market in insurance is characterized by higher premiums, stricter underwriting standards, reduced capacity, and limited availability of coverage. One of the primary drivers of a hard market is increased claims frequency and severity. When insurers experience a surge in claims, their loss ratios rise, eroding profitability. This can occur due to various factors, such as an uptick in natural disasters, accidents, or litigation trends. For example, regions prone to hurricanes or wildfires may see insurers facing substantial payouts, prompting them to adjust rates and terms to mitigate future losses. Similarly, industries with rising liability claims, like healthcare or construction, can contribute to this trend, forcing insurers to reevaluate their risk appetite.

Catastrophic losses play a significant role in hardening insurance markets. Events like hurricanes, earthquakes, floods, or pandemics can result in massive financial losses for insurers, often exceeding their reserves or reinsurance coverage. For instance, the aftermath of Hurricane Katrina or the COVID-19 pandemic led to billions in insured losses, straining the industry's financial health. In response, insurers may withdraw from high-risk areas, increase deductibles, or impose coverage exclusions to protect their balance sheets. Reinsurers, who provide backup coverage to primary insurers, may also raise rates or reduce capacity, further tightening market conditions.

Economic instability is another critical factor contributing to hard markets in insurance. During periods of recession, inflation, or supply chain disruptions, insurers face heightened risks. Inflation, for example, drives up the cost of claims settlements, as repair and replacement costs soar. Similarly, economic downturns can lead to increased claims as businesses and individuals file more claims to offset financial losses. Insurers may also face investment income volatility, as low interest rates or market downturns reduce returns on their portfolios. To offset these pressures, insurers often raise premiums, reduce coverage limits, or exit unprofitable lines of business, creating a harder market for policyholders.

The interplay between increased claims, catastrophic losses, and economic instability often creates a feedback loop that exacerbates hard market conditions. For instance, a series of catastrophic events can deplete insurers' capital, making them more risk-averse and less willing to underwrite certain exposures. Simultaneously, economic instability may limit policyholders' ability to absorb higher premiums, leading to reduced demand for coverage. However, as insurers continue to tighten underwriting standards and raise rates, the market becomes increasingly challenging for businesses and individuals seeking affordable insurance. This dynamic underscores the cyclical nature of hard markets and the need for insurers to balance risk management with market sustainability.

Lastly, regulatory and legal environments can amplify the effects of these drivers. In regions with favorable plaintiff litigation trends or stringent regulatory requirements, insurers may face higher claims costs and compliance expenses. This adds another layer of pressure, forcing insurers to adopt more conservative underwriting practices and pass costs onto policyholders. Ultimately, the convergence of increased claims, catastrophic losses, economic instability, and external factors creates the conditions for a hard market, where insurers prioritize financial stability over growth, and policyholders face higher costs and reduced options.

Understanding CDW Insurance: Coverage, Benefits, and Why It Matters

You may want to see also

Explore related products

![]()

Impact on Insureds: Higher costs, reduced coverage options, and stricter policy conditions for policyholders

In a hard market, insureds face significant financial strain due to higher premiums, often the most immediate and noticeable impact. Insurers raise rates to offset their own increased costs and manage risk more conservatively. For policyholders, this means paying more for the same level of coverage they previously held. Small businesses and individuals with limited budgets may struggle to afford these increased costs, forcing them to reevaluate their insurance needs or seek alternatives. For example, a homeowner might see their annual premium rise by 20% or more, while a commercial policyholder could face even steeper increases, particularly in high-risk industries like construction or healthcare.

Alongside premium hikes, insureds often encounter reduced coverage options as insurers tighten their offerings. Non-essential or high-risk coverages may be eliminated or restricted, leaving policyholders with fewer choices to tailor policies to their specific needs. For instance, a business might find that certain liability extensions or add-ons are no longer available, or that coverage limits are lowered. This reduction in options can leave insureds underprotected, as they may be forced to go without critical coverages due to their unavailability or unaffordability. Individuals and businesses must then reassess their risk exposure and decide whether to accept higher self-insurance levels or seek alternative solutions.

Stricter policy conditions further compound the challenges for insureds in a hard market. Insurers impose more rigorous underwriting standards, requiring additional documentation, inspections, or risk mitigation measures before issuing or renewing policies. For example, a homeowner might need to install a new roof or upgrade electrical systems to qualify for coverage, while a business might be required to implement specific safety protocols or training programs. These conditions increase the administrative burden and costs for policyholders, who must invest time and resources to meet insurer demands. Failure to comply can result in denied coverage or policy cancellations, leaving insureds vulnerable to financial losses in the event of a claim.

The combination of higher costs, reduced coverage options, and stricter conditions forces insureds to make difficult decisions. Some may opt to reduce coverage limits or drop certain protections to keep premiums manageable, exposing themselves to greater financial risk. Others might shop around for more affordable alternatives, though finding comparable coverage in a hard market can be challenging. For businesses, these pressures can impact operational planning and profitability, as insurance costs become a larger portion of their budget. Individuals may need to cut back on other expenses to afford necessary coverage, affecting their overall financial stability.

Ultimately, the hard market creates a shift in the balance of power from insureds to insurers, as policyholders have fewer options and less negotiating leverage. Insureds must become more proactive in managing their risk and insurance needs, such as by improving risk management practices, bundling policies, or working closely with brokers to find the best available terms. While these strategies can help mitigate some of the impacts, the overall environment remains challenging, requiring insureds to adapt to a new reality of higher costs, limited choices, and stricter requirements.

Weed and Life Insurance: What UK Smokers Need to Know

You may want to see also

Explore related products

![]()

Duration: Typically cyclical, lasting 3-5 years before market conditions soften again

In the insurance industry, a hard market is characterized by its cyclical nature, with distinct phases of tightening and softening conditions. The duration of a hard market is a critical aspect to understand, as it directly impacts insurers, brokers, and policyholders alike. Typically, a hard market phase lasts between 3 to 5 years before market conditions begin to soften again. This cycle is driven by a combination of factors, including economic conditions, claims trends, regulatory changes, and natural disasters, which collectively create an environment of increased risk and reduced capacity. During this period, insurers often adopt a more conservative underwriting approach, leading to higher premiums, stricter policy terms, and reduced availability of coverage.

The 3-5 year timeframe of a hard market is not arbitrary but is rooted in the time it takes for the industry to adjust to and recover from the challenges that precipitated the hard market. For instance, after a series of catastrophic events or a surge in claims, insurers may experience significant financial strain. It takes time for them to rebuild capital reserves, reassess risk models, and implement new strategies to mitigate future losses. This adjustment period is a key reason why hard markets do not resolve quickly. Additionally, external factors such as inflation, supply chain disruptions, or changes in reinsurance costs can prolong the hard market phase, further extending the cycle.

Policyholders and businesses must plan for the 3-5 year duration of a hard market, as it directly affects their insurance costs and coverage options. During this period, premiums may rise sharply, and certain types of coverage may become harder to obtain. For example, industries with higher risk profiles, such as construction or healthcare, may face particularly stringent underwriting requirements. Understanding the cyclical nature of the market helps stakeholders manage expectations and develop strategies to navigate the challenges. This might include risk mitigation measures, alternative risk financing, or working closely with brokers to find the best available options.

The transition from a hard market to a soft market typically occurs as insurers regain financial stability, competition increases, and claims trends stabilize. However, the exact timing within the 3-5 year window can vary based on regional and industry-specific factors. For instance, a hard market in property insurance might soften sooner if there is a period of low catastrophic activity, while liability insurance may take longer due to ongoing litigation trends. Monitoring industry indicators and staying informed about market conditions is essential for anticipating when the shift to a softer market will occur.

In summary, the duration of a hard market in insurance is typically 3 to 5 years, reflecting the time needed for the industry to respond to and recover from adverse conditions. This cyclical pattern is a fundamental aspect of the insurance market, influencing underwriting practices, pricing, and availability of coverage. For all stakeholders, recognizing and preparing for this timeframe is crucial to effectively managing risks and costs during a hard market phase.

Lincoln National Life Insurance: Size and Scope Explored

You may want to see also

Explore related products

![]()

Strategies for Insurers: Focus on risk selection, rate adequacy, and operational efficiency to remain profitable

In a hard market, insurers face significant challenges due to increased claims, rising costs, and reduced capacity, making profitability a top concern. To navigate these conditions successfully, insurers must adopt strategic measures that focus on risk selection, rate adequacy, and operational efficiency. These three pillars are critical to ensuring financial stability and long-term viability during tough market cycles. By prioritizing these areas, insurers can mitigate losses, optimize pricing, and streamline operations to maintain profitability.

Risk selection becomes paramount in a hard market, as insurers must carefully evaluate and underwrite risks to avoid exposure to high-severity or frequent claims. This involves leveraging advanced analytics and data-driven insights to identify and segment risks more accurately. Insurers should focus on retaining low-risk, profitable business while avoiding or pricing appropriately for higher-risk policies. Implementing stricter underwriting guidelines, enhancing risk assessment tools, and utilizing predictive modeling can help insurers make informed decisions. Additionally, diversifying the portfolio across different lines of business and geographies can reduce concentration risk and improve overall resilience.

Rate adequacy is another critical strategy for insurers operating in a hard market. As claims costs and reinsurance premiums rise, insurers must ensure that premiums reflect the true cost of risk. This requires regular reviews and adjustments to pricing models, incorporating inflationary trends, loss trends, and changing risk landscapes. Insurers should also engage in transparent communication with regulators to secure approval for necessary rate increases. Implementing usage-based pricing, dynamic pricing models, and tiered pricing structures can further enhance rate adequacy by aligning premiums more closely with individual risk profiles.

Operational efficiency is essential to reducing costs and improving profitability in a hard market. Insurers must streamline processes, eliminate redundancies, and leverage technology to enhance productivity. Automation of routine tasks, such as claims processing and policy administration, can significantly reduce operational expenses. Investing in digital transformation initiatives, including artificial intelligence and machine learning, can improve decision-making, customer experience, and overall efficiency. Additionally, insurers should focus on talent management, ensuring that employees are equipped with the skills needed to thrive in a rapidly evolving industry.

Finally, insurers must adopt a proactive and agile approach to remain competitive in a hard market. This includes monitoring market trends, staying ahead of regulatory changes, and fostering strong relationships with brokers, reinsurers, and policyholders. By focusing on risk selection, rate adequacy, and operational efficiency, insurers can not only survive but also thrive in challenging market conditions. These strategies, when implemented effectively, enable insurers to maintain profitability, strengthen their market position, and build resilience for future cycles.

Beat a Life Insurance Blood Test: Strategies for Success

You may want to see also

Frequently asked questions

A hard market in insurance refers to a period when insurance premiums rise, underwriting standards become stricter, and coverage options are more limited. It occurs due to increased claims, higher loss ratios, or economic factors that reduce insurer profitability.

A hard market is typically caused by factors such as catastrophic events (e.g., hurricanes, wildfires), rising claims costs, increased reinsurance costs, low investment returns, or regulatory changes that impact insurer profitability.

During a hard market, policyholders may experience higher premiums, reduced coverage limits, stricter policy conditions, or difficulty finding insurers willing to underwrite certain risks. It can also lead to policy cancellations or non-renewals.

The duration of a hard market varies but generally lasts 3 to 5 years. It depends on how quickly insurers can restore profitability through rate increases, improved underwriting, or changes in market conditions.

The opposite of a hard market is a soft market, characterized by lower premiums, more lenient underwriting standards, and increased competition among insurers to attract policyholders. Soft markets often follow periods of insurer profitability and stable conditions.