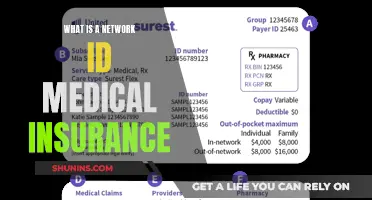

A medical insurance scheme, also known as health insurance, is a financial instrument that protects individuals from the financial burden of medical emergencies. It is a security cover where the insurer bears the insured person's healthcare costs in exchange for regular premium payments. Medical insurance schemes can be purchased for an individual or a family, and they cover expenses such as hospitalisation, surgeries, ambulance charges, ICU charges, doctor's fees, and medication. Governments around the world have also introduced medical insurance schemes to provide affordable healthcare to their citizens, especially those from low-income families. These schemes aim to reduce out-of-pocket expenses, improve access to healthcare, and prevent people from falling into poverty due to high medical costs.

| Characteristics | Values |

|---|---|

| Purpose | To provide financial protection in case of medical emergencies or planned treatments |

| Provider | Governments, insurance companies |

| Cost | Regular premium payments |

| Coverage | Surgeries, hospitalisation, day-care treatments, pre-hospitalisation, post-hospitalisation, ambulance charges, ICU charges, doctor's fees, room rent, medication, medical tests, advanced treatments (e.g. robotic surgeries, chemotherapies) |

| Benefits | Tax savings, cashless treatment, annual health check-ups, customisable benefits |

| Eligibility | Based on income, family size, age, pre-existing conditions |

| Scope | Individual or family plans |

Explore related products

What You'll Learn

![]()

How do medical insurance schemes work?

Medical insurance schemes, also known as health insurance, are a form of financial protection against medical emergencies. They are designed to cover an individual's healthcare costs in exchange for regular premium payments. These schemes can be purchased for oneself or as a family floater plan, covering the medical needs of the entire family.

The functioning of a medical insurance scheme can be broken down into several steps. Firstly, an individual or their employer makes regular premium payments to the insurance company. These payments are typically affordable and can be customised based on the specific plan chosen. In some cases, governments also offer insurance schemes with low premiums to ensure that their citizens have access to quality healthcare.

When an insured person requires medical attention, they can utilise the services of healthcare providers associated with their insurance company. This includes hospitals, clinics, and sometimes even coverage for ambulance services. The insurance policy may cover a range of expenses, including doctor's fees, room rent, ICU charges, medical tests, medication, and even pre and post-hospitalisation costs. In some cases, insurance schemes also offer cashless treatment, where the insured does not have to make any upfront payments and the insurer settles the bills directly with the healthcare provider.

After receiving treatment, the insured person can file a claim with the insurance company to reimburse any expenses incurred. The insurance company will then review the claim and determine the settlement. It is important to note that the coverage provided is usually subject to the policy's terms and conditions, and there may be certain exclusions or limitations. Additionally, some insurance schemes offer annual health check-ups and customisable benefits for their members.

Medical insurance schemes are essential in providing financial security and ensuring access to quality healthcare. They protect individuals from the financial burden of unexpected medical emergencies and help improve overall health outcomes. By spreading the risk across a large number of people, insurance companies can offer comprehensive coverage at affordable prices.

FSA Accounts: Medical Insurance Not Always Needed

You may want to see also

Explore related products

![]()

Who are medical insurance schemes for?

Medical insurance schemes are for anyone who wants to protect their savings in the event of a medical emergency. They are also for people who want to plan for future treatments, including surgeries, hospitalisation, day-care treatments, pre-hospitalisation, post-hospitalisation, ambulance charges, and ICU charges.

In some countries, governments have introduced health insurance schemes to provide good-quality healthcare to their citizens. These schemes are specifically designed to benefit low-income families or poor people by providing them with adequate medical insurance coverage at an affordable price. For example, the Indian government launched the Ayushman Bharat Yojana, also known as the Pradhan Mantri Jan Arogya Yojana (PMJAY), to provide free healthcare services to more than 40% of the country's population. This scheme offers health coverage for medicines, diagnostic expenses, medical treatment, and pre-hospitalisation costs.

Medical insurance schemes can also be designed for specific groups, such as government officials and pensioners, as seen with the Central Government Health Scheme in India. This scheme provides comprehensive healthcare facilities, including reimbursement of hospitalisation expenses, all dispensary-related services, investigations like X-rays and MRIs, and specialist consultations.

In Nigeria, the National Health Insurance Scheme (NHIS) is a social health insurance programme designed to improve access to healthcare for Nigerians, especially civil servants. It offers attractive packages, including outpatient care, medical consumables, drugs, diagnostic tests, and free inpatient care for a limited number of days per year.

Additionally, some medical insurance schemes cater to specific sectors or types of workers. For instance, the Employees' State Insurance Scheme in India provides medical coverage, maternity insurance, sickness benefits, and disability benefits to all workers in certain establishments employing more than 10 employees.

Overall, medical insurance schemes are designed to provide financial protection and peace of mind to individuals and families by ensuring access to quality healthcare services, regardless of their income level or specific group affiliations.

Navigating Medical Insurance After Being Laid Off

You may want to see also

Explore related products

![]()

What do medical insurance schemes cover?

Medical insurance schemes, also known as health insurance, are a form of insurance that provides financial cover for medical treatment and related expenses. These expenses can include doctor's visits, nursing, surgeries, dental work, optometry, medicines, and hospital accommodation.

In exchange for a monthly contribution or premium, medical insurance schemes help to pay for healthcare needs, protecting your savings by covering your medical expenses. This means that you can avail of the required treatment without worrying about the financial burden.

There are two types of medical schemes: open and closed (restricted). Anyone can join an open scheme, whereas closed schemes are for employees of specific employer groups or members of a particular profession, industry, association, or union.

The coverage provided by medical insurance schemes varies, but generally, they cover expenses incurred during hospitalisation, including room rent, doctor's fees, and medication. Some schemes also cover medical expenses incurred before hospitalisation and follow-up treatments after discharge. Additionally, they may cover advanced medical treatments, such as robotic surgeries and chemotherapies.

In the case of an emergency, some insurance providers offer a ''Cashless Everywhere' facility, allowing policyholders to obtain cashless treatment at any hospital, not just network hospitals. This eliminates the worry of arranging money to pay hospital bills, as the insurer settles the expenses directly.

Maternity Coverage: Understanding Your Medical Insurance Benefits

You may want to see also

Explore related products

![]()

Benefits of medical insurance schemes

Medical insurance schemes, also known as health insurance, are a type of financial instrument that protects individuals and families from the burden of medical costs. They are often structured with an upper ceiling limit on an annual or per-family basis. In India, for example, the National Health Authority (NHA) has implemented the Ayushman Bharat Yojana scheme, also known as Pradhan Mantri Jan Arogya Yojana (PMJAY), which provides free healthcare services to over 40% of the country's population, with a health cover of ₹500,000 per family per year.

The benefits of medical insurance schemes are extensive and include:

Financial Security

Health insurance provides financial security and peace of mind by covering medical costs, which can be significant in the event of hospitalisation, surgery, or critical illness treatment. It safeguards your savings and helps maintain financial stability, allowing individuals to focus on their health and recovery without the added stress of financial strain.

Access to Quality Healthcare

Medical insurance schemes ensure access to quality healthcare services without the worry of affordability. This includes coverage for hospitalisation expenses, doctor's fees, medication, diagnostics, and post-hospitalisation recovery care. Some schemes also offer access to advanced medical treatments, such as robotic surgeries and chemotherapy.

Pre- and Post-Hospitalisation Coverage

Most health insurance policies cover expenses incurred before and after hospitalisation. This includes pre-hospitalisation diagnostics and consultations, as well as post-hospitalisation recovery expenses. This comprehensive coverage ensures that individuals can receive the necessary care without financial barriers.

Critical Illness Cover

Many insurers offer critical illness cover as an add-on benefit, providing financial protection for critical illnesses such as stroke, kidney failure, heart attack, or cancer. This type of coverage can be crucial in managing the financial impact of serious health conditions.

Tax Benefits

Health insurance policies often offer tax advantages. In India, for example, individuals can claim deductions on the premium paid for health insurance policies under Section 80D of the Income Tax Act. This provides additional financial relief to policyholders.

Family Coverage

Family health insurance plans offer comprehensive coverage for the entire family under a single policy. This includes spouses, children, and dependent parents. Family plans often provide cost-effective premiums, higher sum insured amounts, and access to quality healthcare for all family members, ensuring financial protection against medical emergencies.

Your Medical Insurance Claims: Privacy from Your Spouse

You may want to see also

Explore related products

![]()

Drawbacks of medical insurance schemes

Medical insurance schemes offer financial protection against medical expenses. Individuals make regular premium payments to receive medical cost coverage. However, there are several drawbacks to medical insurance schemes.

Firstly, high premium costs can be a burden, especially for those with lower incomes or multiple dependents. The cost of insurance premiums may increase with age, further straining the financial resources of older individuals.

Secondly, medical insurance schemes often have restrictive coverage options. Policies usually only pay out for specific health-related events, and there may be exclusions or limitations on certain medical expenses. For example, a hospitalisation policy may not cover all medical expenses, and there could be waiting periods imposed before coverage begins.

Thirdly, medical insurance schemes can have complicated administrative requirements. The variety of guidelines and rules across different insurance schemes can confuse both providers and patients, leading to increased administrative costs. Physicians and their staff may need to spend more time preparing multiple lists to comply with different insurance schemes, and pharmacists may need to consult multiple fee lists to determine drug prices.

Additionally, the fragmentation of health insurance schemes can create challenges. Each insurance scheme may behave differently, following distinct health policies and interpretations of guidelines. This fragmentation can make it easier for medical fraud to occur, as providers' medical profiles are not centralized in a single database, allowing someone to misuse an insurance scheme without immediate detection.

Lastly, dissatisfaction may arise among population groups with generous basic benefits packages if insurance funds are merged, potentially leading to social unrest or increased demand for private insurance options.

Starbucks Medical Insurance: What's the Alternative?

You may want to see also

Frequently asked questions

A medical insurance scheme, also known as a health insurance scheme, is a financial instrument that protects your savings in the case of medical emergencies. The insurer bears the insured person's healthcare costs in exchange for regular premium payments.

Medical insurance schemes cover various medical expenses, including surgeries, hospitalisation, day-care treatments, pre-hospitalisation, post-hospitalisation, ambulance charges, ICU charges, doctor's consultations, medical tests, and medication.

Some examples of medical insurance schemes include the National Health Insurance Scheme (NHIS) in Nigeria, the Central Government Health Scheme in India, and the Pradhan Mantri Jan Arogya Yojana (PMJAY) in India.

When choosing a medical insurance scheme, it is important to evaluate the healthcare needs, age, and current health status of each family member. Consider the different benefits offered by various schemes and select one that best suits your needs.