Medigap insurance, also known as Medicare Supplement Insurance, is a type of private health insurance policy designed to help cover some of the out-of-pocket costs that Original Medicare (Part A and Part B) doesn’t fully pay for, such as copayments, coinsurance, and deductibles. These policies are standardized by the federal government and offered by private insurance companies, ensuring consistent benefits across plans labeled with letters A through N. Medigap plans work alongside Original Medicare, providing additional financial protection and peace of mind for beneficiaries, though they do not cover services like prescription drugs, which require a separate Medicare Part D plan. It’s important to enroll during the Medigap Open Enrollment Period, which begins when you turn 65 and have Part B, to avoid potential underwriting and higher premiums.

| Characteristics | Values |

|---|---|

| Definition | Medigap insurance, also known as Medicare Supplement Insurance, is a private health insurance policy designed to cover some of the out-of-pocket costs not covered by Original Medicare (Part A and Part B). |

| Purpose | Helps pay for copayments, coinsurance, and deductibles associated with Medicare-covered services. |

| Eligibility | Available to individuals aged 65 and older, or under 65 with certain disabilities, who are enrolled in Medicare Part A and Part B. |

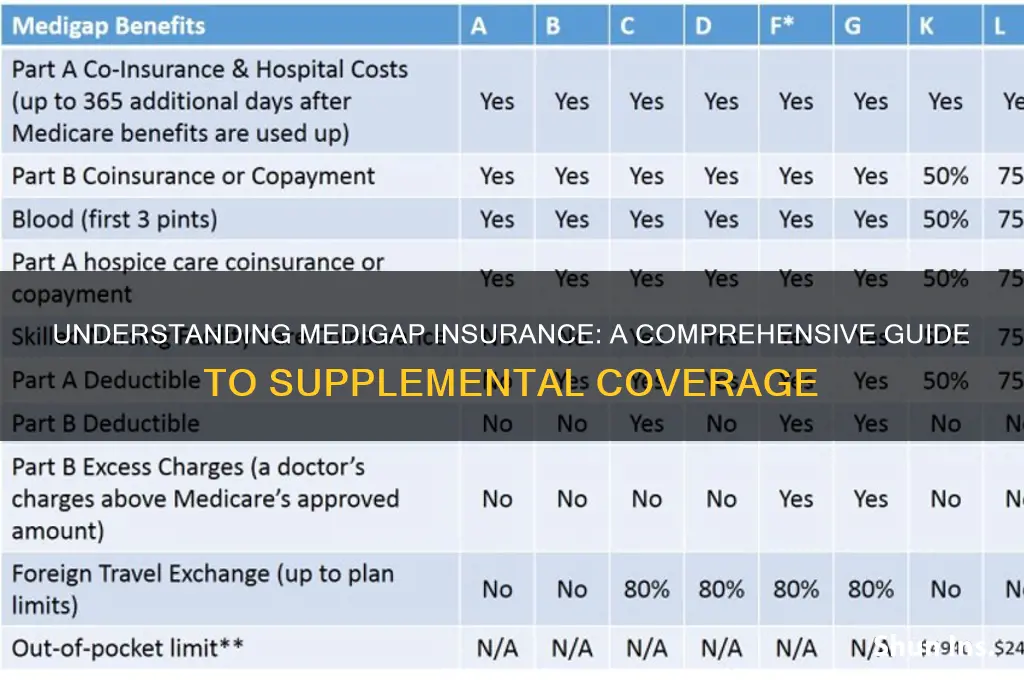

| Plans | Standardized plans labeled A, B, C, D, F, G, K, L, M, and N, each offering different levels of coverage. |

| Coverage | Varies by plan but may include Part A and B deductibles, coinsurance, hospice care, skilled nursing facility coinsurance, and foreign travel emergency care. |

| Premiums | Monthly premiums paid to the private insurance company in addition to Medicare Part B premiums. |

| Open Enrollment | 6-month period starting when you turn 65 and are enrolled in Medicare Part B, during which you can buy any Medigap policy without medical underwriting. |

| Guaranteed Issue Rights | Allows you to buy a Medigap policy without being denied or charged more due to health conditions under certain circumstances. |

| Network Restrictions | Typically no network restrictions; you can see any doctor or hospital that accepts Medicare. |

| Prescription Drug Coverage | Does not include prescription drug coverage; a separate Medicare Part D plan is needed for this. |

| Renewability | Guaranteed renewable as long as premiums are paid, regardless of health status. |

| Availability | Offered by private insurance companies approved by Medicare. |

| Cost-Sharing | Some plans (K and L) have out-of-pocket limits, while others cover all costs after Medicare pays its share. |

| Foreign Travel Coverage | Plans C, D, F, G, M, and N cover 80% of emergency care during foreign travel, up to plan limits. |

| Enrollment Periods | Outside of open enrollment, enrollment may be subject to medical underwriting, potentially affecting premiums or eligibility. |

| State Variations | Some states (e.g., Massachusetts, Minnesota, and Wisconsin) offer additional standardized Medigap plans. |

| Replacement for Medicare Advantage | Cannot be used with Medicare Advantage plans; Medigap works only with Original Medicare. |

Explore related products

$14.99

What You'll Learn

- Medigap Basics: Supplemental insurance to cover gaps in Original Medicare (Part A & B) costs

- Plan Types: Standardized plans (A-N) with varying coverage levels for deductibles, copays, etc

- Eligibility: Available to those aged 65+ or under 65 with disabilities, enrolled in Medicare

- Enrollment Periods: Best to enroll during 6-month open enrollment starting at 65

- Costs & Premiums: Monthly premiums vary by plan, insurer, and location; not income-based

![]()

Medigap Basics: Supplemental insurance to cover gaps in Original Medicare (Part A & B) costs

Medigap insurance, also known as Medicare Supplement Insurance, is a type of private health insurance policy designed to work alongside Original Medicare (Part A and Part B) to help cover certain out-of-pocket costs that Medicare doesn’t fully pay. These costs can include copayments, coinsurance, and deductibles, which can add up quickly for beneficiaries. Medigap policies are standardized by the federal government, meaning the benefits for each plan type are consistent across all insurance companies, though premiums may vary. This standardization makes it easier for consumers to compare plans and choose the one that best fits their needs.

Original Medicare covers a significant portion of healthcare expenses, but it doesn’t cover everything. For example, Part A typically covers hospital stays, while Part B covers doctor visits and outpatient services. However, beneficiaries are still responsible for costs like the Part A deductible for hospital stays, 20% coinsurance for Part B services, and the Part B deductible. Medigap policies step in to fill these gaps, providing additional financial protection and predictability in healthcare spending. Without Medigap, beneficiaries might face substantial expenses, especially in the event of a major illness or injury.

There are currently 10 standardized Medigap plans available, labeled Plan A through Plan N (excluding E, H, I, and J, which are no longer sold). Each plan offers a different combination of benefits, with Plan F and Plan G being the most comprehensive. For instance, Plan F covers all gaps in Original Medicare, including the Part B deductible, while Plan G covers everything except the Part B deductible. It’s important to note that starting January 1, 2020, Plan F is no longer available to new Medicare enrollees, though those who enrolled before this date can keep their Plan F coverage.

To be eligible for a Medigap policy, you must already be enrolled in both Medicare Part A and Part B. The best time to purchase a Medigap plan is during your six-month Medigap Open Enrollment Period, which begins the month you turn 65 and are enrolled in Part B. During this period, insurance companies cannot deny you coverage or charge you more based on pre-existing conditions. Outside of this window, you may face medical underwriting, which could result in higher premiums or denial of coverage. Additionally, Medigap policies only cover one person, so couples must purchase separate policies.

It’s crucial to understand that Medigap policies do not cover everything. They do not include benefits for prescription drugs, vision, dental, hearing aids, or private-duty nursing. For prescription drug coverage, beneficiaries need to enroll in a standalone Medicare Part D plan. Medigap is specifically designed to supplement Original Medicare, not replace it or work with Medicare Advantage plans. When choosing a Medigap policy, consider your healthcare needs, budget, and the level of coverage you require to ensure you’re adequately protected against unexpected medical expenses.

Life Insurance and Jeff Bezos: Does He Need It?

You may want to see also

Explore related products

![]()

Plan Types: Standardized plans (A-N) with varying coverage levels for deductibles, copays, etc

Medigap insurance, also known as Medicare Supplement Insurance, is designed to help cover the out-of-pocket costs that Original Medicare (Part A and Part B) doesn’t fully pay for, such as deductibles, copayments, and coinsurance. To simplify the selection process for beneficiaries, Medigap plans are standardized and labeled with letters A through N. Each plan type offers a different combination of benefits, allowing individuals to choose coverage that aligns with their healthcare needs and budget. Understanding these standardized plans is crucial for making an informed decision.

Standardized Medigap Plans (A-N) provide varying levels of coverage for deductibles, copays, and other costs. Plan A is the most basic, covering Medicare Part A and Part B coinsurance, hospice care coinsurance, and the first three pints of blood. While it offers essential coverage, it does not include benefits like the Part A deductible or skilled nursing facility coinsurance. On the other hand, Plan F is one of the most comprehensive, covering all the gaps in Original Medicare, including the Part B deductible. However, Plan F is no longer available to new Medicare beneficiaries as of 2020, though those who enrolled before this date can keep their coverage.

Plans B through N fill the gap between the basic and comprehensive options, each offering a unique set of benefits. For example, Plan G is a popular choice for new enrollees, as it covers nearly everything Plan F does, except the Part B deductible. Plan K and Plan L are high-deductible plans that cover a percentage of costs (50% for Plan K and 75% for Plan L) after the deductible is met. These plans are ideal for those who want lower premiums but are willing to pay more out of pocket if they need significant medical care. Plan N is another cost-effective option, covering most gaps except for the Part B deductible and excess charges, and it requires small copayments for doctor visits and emergency room trips.

When selecting a Medigap plan, it’s important to consider your healthcare needs and financial situation. For instance, if you frequently visit the doctor or anticipate needing specialized care, a plan with higher coverage for copays and deductibles might be beneficial. Conversely, if you rarely use medical services, a lower-cost plan with fewer benefits could suffice. Additionally, premiums for the same plan letter can vary by insurance company, so it’s advisable to compare prices and reputations of providers.

Lastly, it’s worth noting that not all Medigap plans are available in every state, and some states offer additional standardized plans beyond the federal options. For example, Massachusetts, Minnesota, and Wisconsin have their own standardized plans with different labeling systems. Regardless of location, all Medigap policies must be clearly identified with their corresponding letter, making it easier for beneficiaries to compare plans across insurers. By understanding the differences between Plan A and Plan N, individuals can select the Medigap policy that best meets their healthcare and financial needs.

Bedridden and Seeking Life Insurance: What Are Your Options?

You may want to see also

Explore related products

![]()

Eligibility: Available to those aged 65+ or under 65 with disabilities, enrolled in Medicare

Medigap insurance, also known as Medicare Supplement Insurance, is a type of private health insurance policy designed to cover some of the out-of-pocket costs that Original Medicare (Part A and Part B) doesn’t pay. These costs can include copayments, coinsurance, and deductibles. To be eligible for a Medigap policy, individuals must first be enrolled in both Medicare Part A and Part B. This foundational requirement ensures that Medigap can effectively supplement the coverage provided by Original Medicare. Without active enrollment in both parts, a Medigap policy cannot be purchased or utilized.

The primary eligibility criterion for Medigap insurance is age, with the majority of policies available to individuals aged 65 and older. This age threshold aligns with the typical eligibility age for Medicare itself, as most people become eligible for Medicare when they turn 65. Once enrolled in Medicare, individuals in this age group can explore Medigap options to enhance their healthcare coverage. It’s important to note that the best time to enroll in a Medigap policy is during the six-month Medigap Open Enrollment Period, which begins on the first day of the month in which you turn 65 and are enrolled in Medicare Part B. During this period, insurers cannot deny coverage or charge higher premiums based on pre-existing conditions.

While age 65 is the most common eligibility threshold, Medigap insurance is also available to individuals under 65 who qualify for Medicare due to disabilities or certain medical conditions. These individuals must be enrolled in both Medicare Part A and Part B to purchase a Medigap policy. However, unlike those aged 65 and older, individuals under 65 may face different rules and limitations when it comes to Medigap eligibility and pricing. Some states require insurers to offer Medigap policies to Medicare beneficiaries under 65, but these policies may come with higher premiums or fewer options. It’s essential for this group to research state-specific regulations to understand their Medigap options fully.

Enrollment in Medicare is a non-negotiable requirement for Medigap eligibility, regardless of age. This means that individuals must have both Part A (Hospital Insurance) and Part B (Medical Insurance) in place before they can purchase a Medigap policy. Medigap is specifically designed to work alongside Original Medicare, not with other types of health coverage like Medicare Advantage plans. Attempting to pair Medigap with a Medicare Advantage plan is not allowed and could result in the cancellation of the Medigap policy. Therefore, beneficiaries must carefully consider their Medicare choices to ensure compatibility with Medigap.

Finally, it’s worth noting that eligibility for Medigap does not depend on income, health status, or medical history during the Open Enrollment Period for those aged 65 and older. However, outside of this period, insurers may use medical underwriting to determine eligibility and premiums, which could result in higher costs or denial of coverage for individuals with pre-existing conditions. For those under 65 with disabilities, eligibility and pricing may vary significantly by state and insurer. Prospective Medigap policyholders should consult with insurance providers or state insurance departments to understand their specific eligibility requirements and available options.

Understanding Life Insurance Trust: Gross Income Explained

You may want to see also

Explore related products

![]()

Enrollment Periods: Best to enroll during 6-month open enrollment starting at 65

Medigap insurance, also known as Medicare Supplement Insurance, is a type of private insurance policy designed to cover the gaps in Original Medicare (Part A and Part B). These gaps include copayments, coinsurance, and deductibles, which can add up quickly for beneficiaries. Understanding the enrollment periods for Medigap is crucial, as it directly impacts your ability to secure a policy with guaranteed issue rights, meaning insurers cannot deny you coverage or charge you more based on pre-existing conditions.

The best time to enroll in Medigap insurance is during the 6-month open enrollment period that begins the month you turn 65 and are enrolled in Medicare Part B. This period is a golden opportunity because, during these six months, insurance companies are required by federal law to sell you any Medigap policy they offer, regardless of your health status. This guaranteed issue right ensures you can choose the plan that best fits your needs without facing higher premiums or exclusions for pre-existing conditions. Missing this window can complicate the process and potentially limit your options.

If you miss the 6-month open enrollment period, you may still be able to purchase a Medigap policy, but you could face medical underwriting. This means insurers can charge you more or deny coverage based on your health history. While some states have additional open enrollment periods or guaranteed issue rights, these vary widely, and relying on them is risky. Therefore, enrolling during the initial 6-month window is the most straightforward and secure approach to obtaining Medigap coverage.

It’s important to note that this 6-month open enrollment period is different from the Annual Enrollment Period (AEP) for Medicare Advantage or Part D prescription drug plans. The Medigap open enrollment period is a one-time opportunity tied to your 65th birthday and Part B enrollment. If you delay enrolling in Part B because you’re still covered by an employer’s group health plan, your Medigap open enrollment period will start when you eventually sign up for Part B, not when you first become eligible for Medicare.

To make the most of this enrollment period, research Medigap plans in advance to understand the differences between Plan A, B, C, D, G, K, L, M, and N. Plan G and Plan N are currently the most popular due to their comprehensive coverage and cost-effectiveness. Consulting with a licensed insurance agent can also help you navigate your options and ensure you enroll in the plan that best meets your healthcare needs and budget.

In summary, enrolling in Medigap insurance during the 6-month open enrollment period starting at age 65 is the optimal strategy to secure coverage without facing penalties or denials due to pre-existing conditions. This period is a critical window that ensures you have access to the full range of Medigap plans available in your area. Planning ahead and acting promptly during this time can provide long-term peace of mind and financial protection against unexpected healthcare costs.

Social Insurance: Institutional or Residual?

You may want to see also

Explore related products

![]()

Costs & Premiums: Monthly premiums vary by plan, insurer, and location; not income-based

Medigap insurance, also known as Medicare Supplement Insurance, is a type of policy designed to cover the gaps in Original Medicare (Part A and Part B). These gaps include copayments, coinsurance, and deductibles, which can add up quickly for beneficiaries. When considering Medigap insurance, one of the most critical aspects to understand is the cost structure, particularly the monthly premiums. Unlike some government-subsidized programs, Medigap premiums are not based on income. Instead, they vary depending on several key factors: the specific plan chosen, the insurance company providing the policy, and the geographic location of the policyholder.

The plan type is a primary determinant of Medigap premiums. There are standardized Medigap plans labeled A through N, each offering different levels of coverage. For example, Plan F, which covers all Medicare-approved expenses, typically has higher premiums than Plan G or Plan N, which offer slightly less coverage. Beneficiaries must carefully evaluate their healthcare needs and budget to determine which plan aligns best with their financial situation. It’s important to note that while Plan F is the most comprehensive, it is no longer available to new Medicare enrollees as of 2020, leaving Plan G as the next best option for comprehensive coverage.

The insurance company also plays a significant role in determining Medigap premiums. Even for the same plan type, premiums can vary widely between insurers. This is because each company uses its own pricing structure, which may be influenced by factors such as administrative costs, profit margins, and claims experience. Beneficiaries are encouraged to shop around and compare quotes from multiple insurers to find the most competitive rates. Additionally, some insurers may offer discounts for factors like paying annually instead of monthly or being a non-smoker.

Geographic location is another critical factor affecting Medigap premiums. Costs can differ significantly from one state to another, and even within the same state, premiums may vary based on local healthcare costs and market competition. For instance, urban areas with higher living costs may have higher premiums compared to rural areas. Beneficiaries should research local pricing trends and consider how their location impacts the overall cost of Medigap insurance.

It’s essential to emphasize that income does not influence Medigap premiums. Unlike Medicare Advantage plans or prescription drug coverage (Part D), which may offer income-based subsidies, Medigap premiums are determined solely by the factors mentioned above. This means that regardless of their income level, beneficiaries will pay the same premium for the same plan from the same insurer in the same location. However, beneficiaries with limited incomes may still qualify for state-based assistance programs that help cover Medigap costs, though these programs vary by state and are not universally available.

In summary, understanding the costs and premiums of Medigap insurance requires careful consideration of the plan type, insurer, and location. By evaluating these factors and comparing options, beneficiaries can make informed decisions to ensure they have the coverage they need at a price they can afford. Since premiums are not income-based, it’s crucial to focus on these variables to find the best value for individual healthcare needs.

Understanding Variable Insurance: Benefits, Risks, and How It Works

You may want to see also

Frequently asked questions

Medigap insurance, also known as Medicare Supplement Insurance, is a type of private insurance policy designed to cover some of the out-of-pocket costs that Original Medicare (Parts A and B) doesn’t pay, such as copayments, coinsurance, and deductibles.

Individuals who are 65 or older and enrolled in Medicare Part A and Part B are eligible to purchase Medigap insurance. Some states also offer Medigap plans to people under 65 with certain disabilities or medical conditions.

The best time to buy a Medigap policy is during your Medigap Open Enrollment Period, which starts the first month you are 65 or older and enrolled in Medicare Part B. During this 6-month period, you have a guaranteed right to buy any Medigap policy sold in your state, regardless of your health.

Medigap plans are standardized by the federal government, meaning Plan A, B, C, etc., offer the same basic benefits across all insurance companies. However, the monthly premiums and additional services may vary by provider, so it’s important to compare plans and costs.