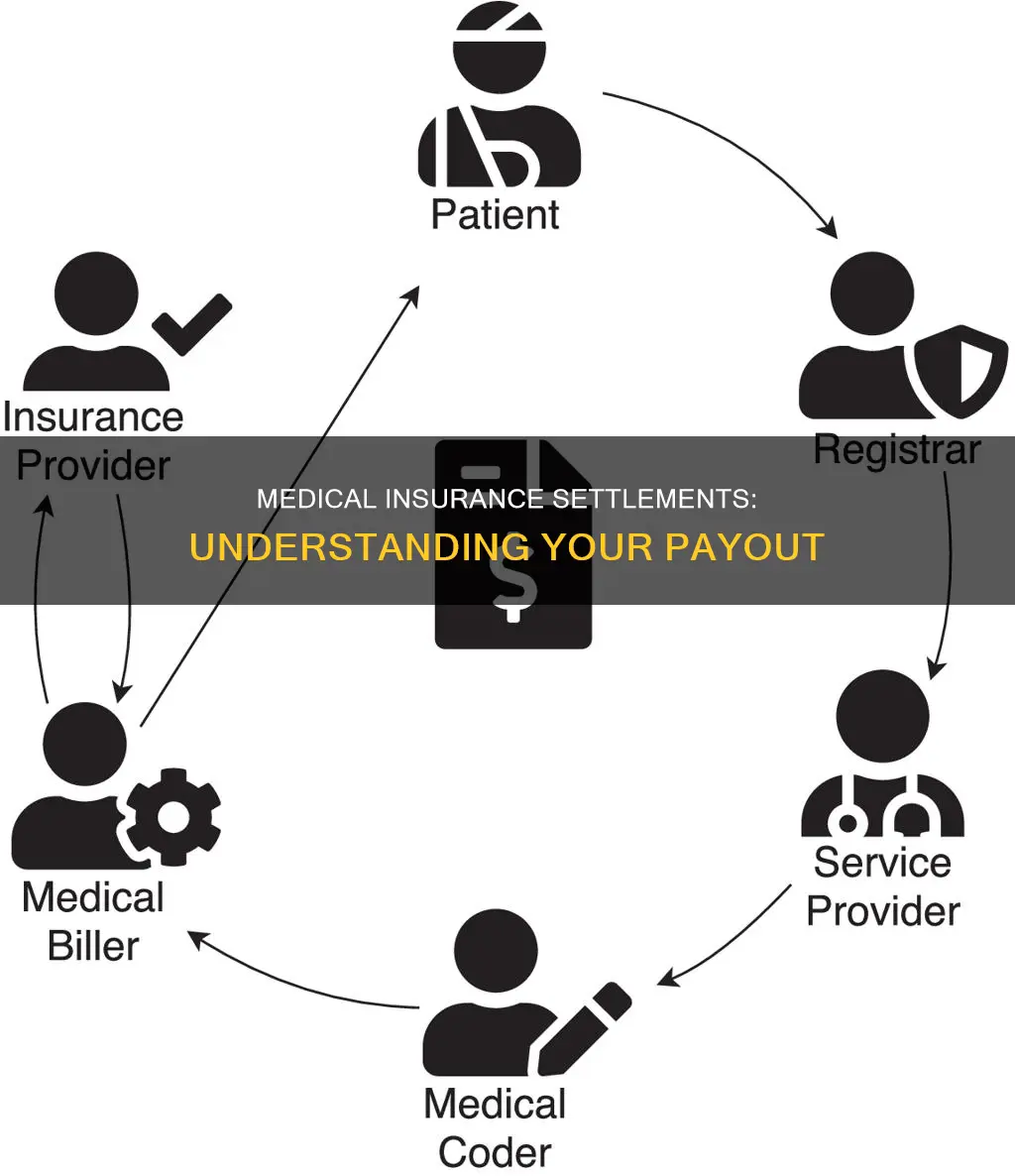

When a person is injured in an accident, they often seek medical treatment. The costs of this treatment are typically covered by their health insurance company, Medicare, or Medicaid. However, after a personal injury settlement is reached, the insurance company may seek reimbursement for the medical expenses they covered. This process is known as subrogation and is based on the idea that the injured person should not benefit from having their medical bills paid twice – once by the insurance company and once by the settlement. The insurance company will send a subrogation claim letter to the injured person's lawyer, stating their entitlement to reimbursement from the settlement. The amount taken from the settlement depends on the nature of the costs covered by the insurance company and the type of health insurance the person has. It is important to work with an attorney familiar with subrogation to navigate this process and ensure accurate deductions from the settlement.

| Characteristics | Values |

|---|---|

| Who is involved | Injured person, at-fault person, insurance companies, hospitals, doctors, lawyers, government healthcare |

| What is involved | Medical bills, medical reimbursements, case expenses, attorney's fees, co-pay obligations, liens, settlements |

| How it works | Injured person's medical bills are paid by their insurance company, which then seeks reimbursement from the settlement |

| Why it happens | To prevent the injured person from benefitting twice: once from insurance and once from the settlement |

| What to watch out for | Balance billing, where hospitals bill more than agreed with the insurance company, leading to higher out-of-pocket expenses |

| How to protect yourself | Consult an experienced attorney, understand your insurance policy and state laws, negotiate settlements |

Explore related products

What You'll Learn

![]()

Medical reimbursements

When a person is injured in an accident, their health insurance may cover the costs of their medical treatment. However, once a settlement is reached with the at-fault party's insurance company, the injured person's insurance company may seek reimbursement from the settlement funds through a process known as subrogation. This means that the portion of the injured person's medical expenses that their health insurance company covered may need to be paid back out of their settlement.

Subrogation is the legal mechanism that allows insurance companies to recover costs from the responsible party after paying out a claim to their policyholder. In the context of personal injury settlements, subrogation allows health insurance companies to be reimbursed for the medical expenses they covered for their insured. This prevents the insured from having their medical bills paid twice—once by their health insurer and once by the settlement or judgment in the accident case.

The subrogation process can be complex and depends on various factors, including the type of health insurance and the state in which the injury occurred. For example, in some states like Alabama, Florida, and Tennessee, the "`common fund`" doctrine requires the third party to pay a share of the attorney's fees. It is important to work with an attorney who is familiar with subrogation to navigate the process effectively and ensure accurate deductions from the settlement.

In addition to subrogation, there are other factors that can impact the net amount an injured person receives from a settlement. For instance, hospitals may engage in a practice known as balance billing, where they bill the patient for the difference between the standard charge for a service and the amount agreed upon with the insurance company. This can result in unexpected out-of-pocket expenses for the patient. Understanding the intricacies of deductibles and co-pays is crucial, as these expenses can add up and affect the final settlement amount.

To protect their interests, individuals should seek legal advice and carefully review their hospital and insurance bills. By working with a personal injury lawyer and maintaining detailed records of their injuries, treatments, and expenses, individuals can strengthen their position during settlement negotiations and ensure they receive the compensation they deserve.

Get a Medical Insurance Card in Boston: A Guide

You may want to see also

Explore related products

![]()

Subrogation

When a person is injured in an accident, their health insurance company may pay for their medical expenses. However, under the principle of subrogation, the insurer has the right to recover the amount they paid from any settlement or judgment obtained by the injured party. This process ensures that the at-fault party or their insurance carrier bears the responsibility for the costs incurred due to the accident.

The subrogation process is meant to protect insured individuals. It helps keep their insurance rates low by ensuring that the at-fault party bears the financial burden of their actions. However, subrogation can also affect the compensation received by the injured party. If the insurance company recovers part of the settlement, the injured person may receive less money.

The subrogation process can be complex, and it may take anywhere from a few weeks to several years to resolve. It is important to understand the specific laws and regulations that apply to subrogation, as they can vary by state and type of insurance. Working with an experienced attorney who is knowledgeable about subrogation can help individuals navigate this process and ensure that their rights are protected.

To summarise, subrogation is the legal mechanism that allows insurance companies to recover costs from the responsible party after paying out a claim to their policyholder. It ensures that the at-fault party bears the financial responsibility for the accident while also protecting the insured individual's interests. However, it can impact the compensation received by the injured party, and seeking legal assistance can help navigate this complex process effectively.

Medical Insurance Costs: Teachers' Expensive Necessity

You may want to see also

Explore related products

![]()

Liens

When a person is injured in an accident, they may hire a personal injury lawyer to negotiate a settlement with the other party's insurance company. The settlement amount agreed upon by the insurance company is used to pay for medical reimbursement, case expenses, attorney's fees, and other expenses. The money remaining after these expenses are paid is given to the client.

In the case of health insurance, the company will often seek reimbursement for the medical expenses it covered. This practice is called subrogation. The idea behind subrogation is that the injured party should not benefit from having their medical bills paid twice—once by their health insurer and once by a settlement or judgment in an accident liability case. Thus, the injured party would have to reimburse their insurer for part of their medical expenses. This reimbursement is typically done through a subrogation lien or claim letter.

A medical lien is a legal contract that allows an injured person to receive treatment without medical insurance before receiving their settlement. Medical liens are beneficial because they allow for prompt treatment, which can help achieve a quicker resolution of the injury. They are also useful because it can be difficult to bring a personal injury case to court until after treatment has been performed. However, it is important to note that a medical lien is not a long-term loan, and it will not be forgiven if the expected settlement does not come through. If the lien is not paid, both the injured party and their attorney may be held financially responsible.

The lien holder (Medicare, Medicaid, or private insurance company) has a legal right to recover the money they paid for treatment from the personal injury settlement. For example, if the settlement is $9,000 and the net recovery after attorney's fees is $6,000, the injured party needs to reimburse the health insurance lien from their $6,000. A lien can only be asserted on expenses directly paid by a health insurance provider to cover treatment for injuries that the client is compensated for in a personal injury settlement. If the personal injury case is unsuccessful, the injured party does not owe anything to the insurance company beyond their regular premium and deductible expenses.

The subrogation process can be time-consuming and frustrating, and it is important to work with an attorney who can help navigate the complexities of the process.

Understanding OO in Medical Insurance: What Does It Mean?

You may want to see also

Explore related products

![]()

Outstanding medical balances

When it comes to "outstanding medical balances" in the context of a settlement with medical insurance, there are several key points to consider:

Firstly, it's important to understand that any outstanding medical balances refer to unpaid medical bills that an individual may have incurred due to injuries or treatment related to the incident for which the settlement is being sought. These outstanding balances can accumulate quickly, especially in cases where extensive medical services are required.

Insurance Company Reimbursement

Insurance companies often seek reimbursement for the medical expenses they have covered on behalf of the injured individual. This is known as subrogation, and it applies to private health insurance companies, government healthcare programs like Medicaid and Medicare, and other entities that paid for medical treatment. The insurance company will send a letter or claim, known as a subrogation lien, requesting reimbursement for the amounts they paid for the individual's medical treatment. This is based on the contract signed with the insurance company, stating that they are entitled to repayment if a third party is found to be at fault.

Balance Billing

In some cases, hospitals or medical providers may engage in a practice known as balance billing, where they bill the patient at their regular rates instead of the discounted rates agreed upon with the insurance company. This can result in the patient being charged additional amounts on top of what the insurance company has already paid. Balance billing may be illegal in certain states, and it is important to review hospital bills thoroughly, especially in emergency situations.

Negotiating Outstanding Balances

Attorneys play a crucial role in negotiating outstanding medical balances at settlement. They work with healthcare providers and insurance companies to reduce the total amount of medical bills and liens to ensure more of the settlement goes to the injured individual. This can be done through a Petition for Equitable Distribution, where a judge decides on the disbursement of funds, or by negotiating directly with the medical providers to reduce the balances to fit within the available settlement funds.

Personal Injury Settlements

In the case of personal injury settlements, the injured party often hires a personal injury lawyer to negotiate a lump-sum settlement with the at-fault party's insurance company. This settlement amount is intended to cover medical reimbursement, case expenses, attorney's fees, and other damages. It is important to understand that any medical bills paid by the injured party's insurance company will typically need to be reimbursed from this settlement, leaving the remaining balance for the client's compensation.

Medicaid Insurance: Understanding Duration and Coverage Limits

You may want to see also

Explore related products

![]()

Medical malpractice

There is no standard formula for calculating medical malpractice settlements. The value of a settlement depends on the amount of damages, which can be economic or non-economic. Economic damages include medical expenses incurred due to malpractice, such as past medical bills and future costs like surgeries, therapy, and medications. If the patient's injuries result in lost wages or diminished earning capacity, these may also be considered economic damages. Non-economic damages include intangible losses such as pain, suffering, mental anguish, and disfigurement, which can be challenging to quantify. The age and life expectancy of the patient can also influence settlement amounts, with younger patients potentially receiving more for future losses.

The average medical malpractice settlement in the US is $348,065, according to the National Practitioner Data Bank. However, individual cases can vary significantly, and it is recommended to consult with an experienced medical malpractice lawyer to determine the value of a specific case. These lawyers typically work on a contingency-fee basis, collecting a percentage of any monetary damages awarded. When navigating a wrongful death claim due to medical malpractice, it is essential to consider factors such as the age, health, and earning capacity of the deceased, as well as the extent of negligence by the healthcare provider.

Obamacare's Impact: Millions Gain Medical Insurance Coverage

You may want to see also

Frequently asked questions

A settlement with medical insurance is a payment made by an insurance company to cover medical expenses incurred due to an injury or accident. This is typically negotiated and paid as a lump sum after all medical treatment is completed.

In cases where the medical bills exceed the settlement amount, your attorney will contact the medical providers and request that they accept a pro-rata share of the settlement as full and final payment. If some providers refuse, a Petition for Equitable Distribution will be filed, and a judge will decide on the disbursement of funds.

Yes, in certain circumstances. For example, in the state of Indiana, liens cannot be filed against someone receiving Medicare or Medicaid benefits. Additionally, if you have an attorney, the amount to be repaid for a health insurance lien may be reduced based on the attorney's fees and costs. It is best to consult with an experienced attorney to understand your specific situation.