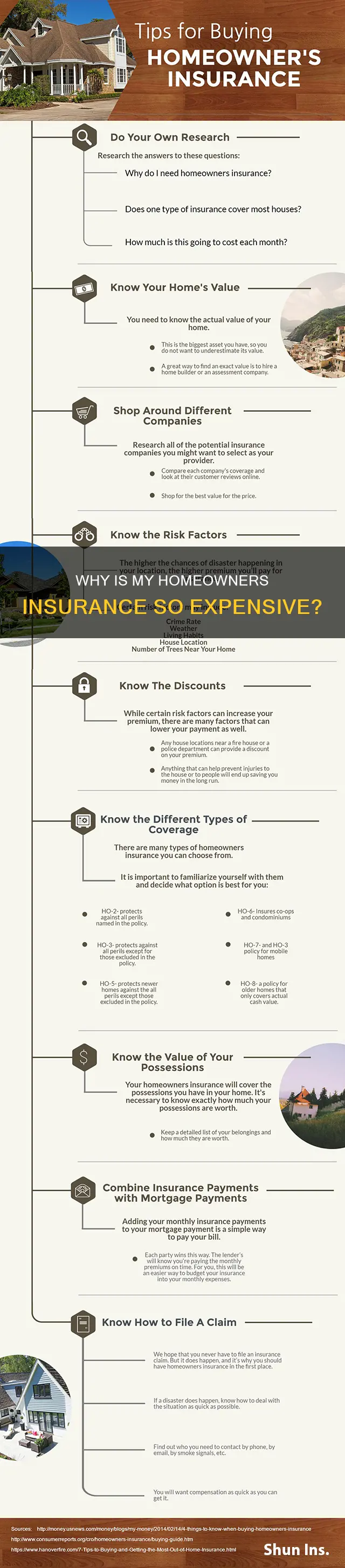

There are a variety of factors that can cause high homeowners insurance. Firstly, insurance rates are influenced by the likelihood of a claim and the potential risks involved, such as natural disasters like hurricanes, floods, wildfires, and other severe weather events. Additionally, the cost of repairs and rebuilding homes has increased due to rising construction costs and labour shortages, and higher prices for building materials. Credit scores also play a role in determining insurance rates, with higher scores potentially leading to lower premiums. Furthermore, insurance companies may consider certain home features, such as swimming pools or valuable belongings, as additional risks that can increase premiums. Comparing rates, choosing higher deductibles, and taking advantage of discounts can help mitigate high insurance costs.

| Characteristics | Values |

|---|---|

| Natural disasters | Hurricanes, floods, droughts, wildfires, storms, tornadoes, hail, windstorms |

| Inflation | Higher material and labor costs, increased shipping costs and delays |

| Supply chain issues | Lack of skilled construction workers, unfilled jobs |

| Increased risk of accidents or damage | Features of the home such as swimming pools, trampolines, wood-burning stoves |

| High-value belongings | Expensive personal belongings or valuable collectibles |

| Credit score | Poor credit scores |

| Crime | Theft-related claims |

| Location | California, Florida, Louisiana, and Ohio have the highest rates |

| Market conditions | Reinsurance costs |

| Consumer demands | Upscale homes and renovations |

Explore related products

What You'll Learn

![]()

Natural disasters and weather-related damage

Natural disasters and severe weather events have a significant impact on the cost of homeowners insurance. As the frequency and severity of these events increase due to climate change, insurers are facing larger and more uncertain financial losses. This has led to a rise in reinsurance rates, which are then passed on to policyholders in the form of higher premiums.

Homeowners in high-risk areas prone to natural disasters, such as hurricanes, wildfires, tornadoes, flooding, earthquakes, and severe storms, typically pay higher insurance rates. The impact of natural disasters on insurance rates can vary across locations, with some states experiencing more significant increases than others. For example, Florida, Louisiana, and California have seen some of the most substantial changes in insurance premiums due to their vulnerability to weather-related damage.

The relationship between disaster risk and insurance premiums has strengthened over time. As the incidence of natural disasters continues to rise, premiums are expected to follow suit. This trend is particularly evident in ZIP codes with the highest disaster risk, where insurance costs have increased the most. For instance, between 2018 and 2023, inflation-adjusted premiums in coastal counties in northeast Florida rose by about $1,000, while nearby counties in coastal Georgia experienced increases of less than $500.

The increase in insurance rates can also be attributed to the rising cost of building materials and labour, as well as supply chain issues. As the cost of repairing or rebuilding homes damaged by natural disasters increases, insurance companies adjust their rates accordingly. This is further exacerbated by the shortage of skilled construction workers, leading to higher labour costs and contributing to the overall rise in homeowners insurance premiums.

Additionally, population growth in severe weather-prone areas and inadequate building codes further contribute to the increasing cost of natural disasters. As more people choose to live in high-risk locations, the potential for catastrophic losses expands, prompting insurers to adjust their practices and rates.

Loss of Use: What Home Insurance Covers

You may want to see also

Explore related products

![]()

Inflation and high construction costs

Labor costs have also increased, with construction wages rising by nearly 5% following the pandemic due to labor shortages. The construction industry faces a skilled labor challenge, resulting in added expenses related to wages, supply chain problems, and other construction issues. This has resulted in a significant increase in the cost of home repairs and replacements, which is reflected in the premiums charged by insurance companies.

The impact of inflation and high construction costs on homeowners' insurance is particularly significant when considering the replacement cost of a home. The replacement cost is the amount required to rebuild a home from scratch and is often the largest coverage limit in a homeowners' insurance policy. As construction costs increase, the replacement cost of a home also increases, and insurance companies adjust their rates accordingly.

To account for rising construction costs, some homeowners' insurance companies offer an ""inflation guard" option, which automatically adjusts the insured value of a home to reflect the increased cost of rebuilding. However, this option is not always automatic and may need to be selected by the policyholder.

The combination of inflation and high construction costs has resulted in higher homeowners' insurance rates, as insurance companies pass on the increased costs of rebuilding and repairing homes to their customers.

Earthquake Insurance in Oregon: Worth the Cost?

You may want to see also

Explore related products

![]()

Credit score and history

Home insurance companies tend to view your home insurance premium as a measure of risk. If they consider you more likely to file a claim, you will likely pay more for your policy. Conversely, if you are seen as lower risk, you will probably pay less for your coverage.

In most states, your credit history and credit-based insurance score can impact whether you are offered a homeowners insurance policy and how much you pay in premiums. While an insurance company might not be allowed to deny your application or renewal based solely on your credit, good credit could help you get approved and pay less for homeowners insurance.

Credit checks are usually soft credit pulls that do not impact your credit score. When you shop for insurance in most states, an insurance company will do a soft inquiry, which does not affect your credit score. This is different from a hard inquiry, a more thorough review of your credit that can take your score down by a few points.

You can check your credit reports for free at annualcreditreport.com regularly to identify errors and have them corrected. If your rates are higher because of your credit history, the insurer should tell you the source of the report so that you can review it. Focusing on improving your credit history could help you save money on insurance.

Contents Coverage: Estimating Homeowners Insurance Needs

You may want to see also

Explore related products

![]()

Crime rates and theft

Theft-related claims can also influence insurance rates. If there is an increase in theft-related claims in your ZIP code or neighbourhood, it could indicate a rise in local crime rates, leading to higher insurance rates for the entire area. Additionally, if you have a history of filing multiple claims, including theft claims, insurers may view you as a higher-risk client, resulting in increased premiums for your policy.

To mitigate the impact of crime rates and theft on your insurance costs, you can consider adjusting your policy's deductible. A higher deductible will likely reduce your premium, but ensure you have sufficient savings to cover the higher deductible in case of a claim. You can also explore other cost-saving strategies, such as bundling your homeowners and auto insurance policies or taking advantage of available discounts.

While crime rates and theft are essential factors in determining insurance costs, other considerations, such as your home's location, reconstruction cost, and your credit history, also play a role in calculating your final insurance premium.

Home Insurance for a 4-Plex: What's the Cost?

You may want to see also

Explore related products

$28.97 $32.97

![]()

High-risk home features

Home insurance rates are influenced by a variety of factors, including the likelihood of a claim being made and the potential risks involved. Some of these factors are beyond an individual's control, such as severe weather events, inflation, and supply chain issues. However, certain features of your home can also contribute to higher insurance rates.

The location of your home also plays a significant role in insurance rates. If your home is situated in an area prone to natural disasters, such as hurricanes, windstorms, or tornadoes, insurance companies may view it as a higher risk. As a result, they may charge higher premiums to account for the increased likelihood of claims being made. This is particularly true for states like Florida, Louisiana, and California, which have experienced a significant increase in weather-related damage in recent years.

In addition to natural disasters, the crime rate in your neighborhood can impact insurance rates. An increase in theft-related claims may indicate a higher crime rate, leading to higher insurance premiums for that specific area. Insurance companies consider the claims history of a particular ZIP code when determining rates, as certain risks may be specific to that region.

It's important to note that insurance rates can also be influenced by market conditions and consumer trends. For instance, the rise in upscale home renovations and luxury home products has led to higher replacement costs when damages occur. This, in turn, can result in increased insurance premiums. Additionally, labor shortages and the increased cost of skilled labor have contributed to higher construction costs, which are reflected in rising insurance rates.

Homeowners Insurance: Sump Pump Installation Covered?

You may want to see also