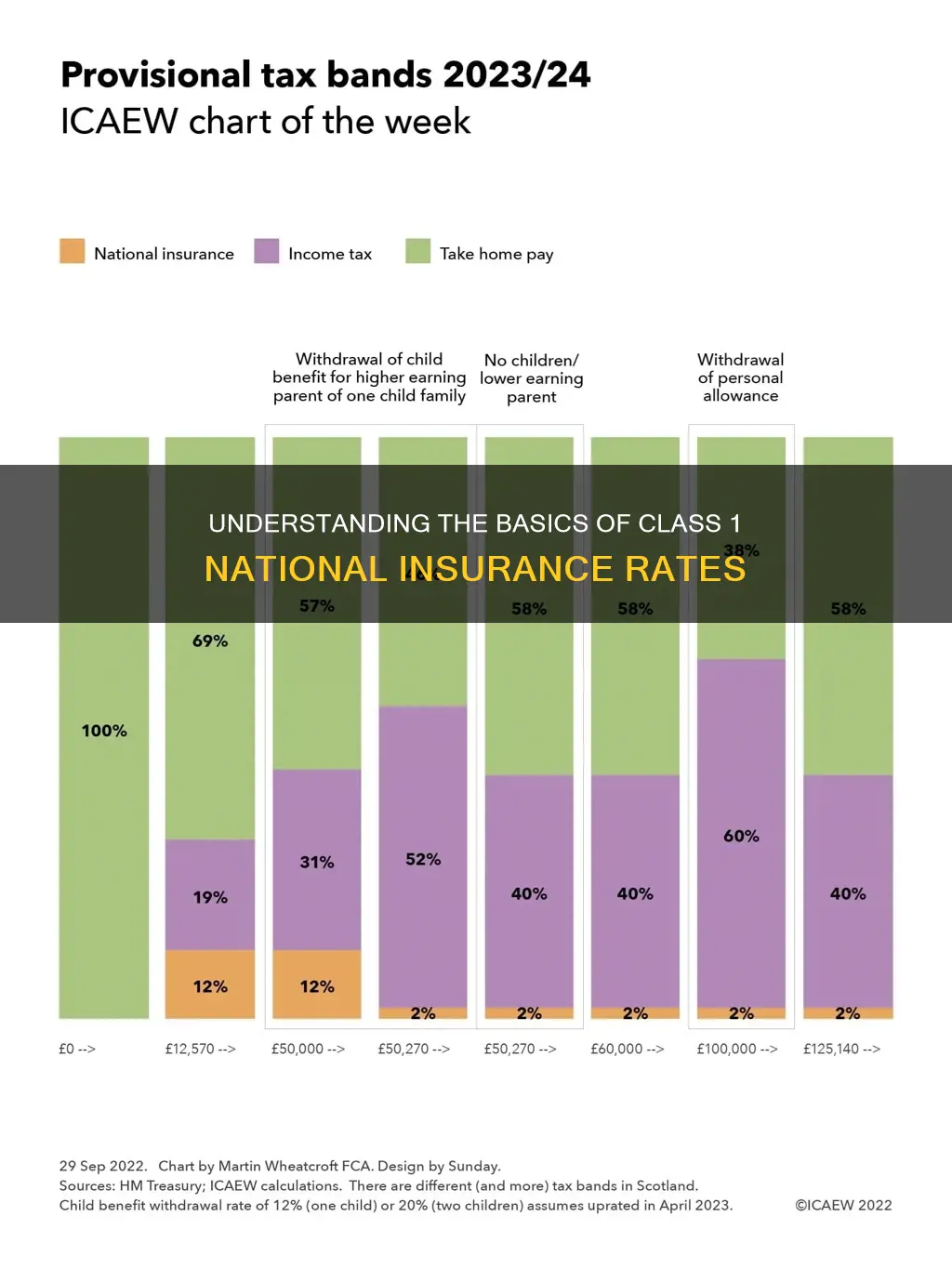

National Insurance is a tax paid by employees, employers, and the self-employed to HMRC. Class 1 National Insurance (NI) contributions are deducted from salary payments by the employer and are only applicable to employees who receive a salary. Those who are self-employed may pay Class 2 and Class 4 National Insurance instead. The rates at which most employees pay National Insurance contributions are 8% from the Primary Threshold to the Upper Earnings Limit and 2% thereafter. For the 2025/26 tax year, if you earn less than £125 per week or £542 per month, you pay no Class 1 NIC. If you have earnings above this lower earnings limit but below the primary threshold, you are treated as having paid NICs without actually making a payment. From 6 April 2025, the Employers' National Insurance Contributions will rise by 1.2% to 15%.

| Characteristics | Values |

|---|---|

| Employee rate | 8% |

| Upper rate | 2% |

| Employer rate | 13.8% |

| Lower earnings limit | £125 per week or £542 per month |

| Primary threshold | £242 per week or £1,048 per month |

| Upper earnings limit | N/A |

| Year of changes | 2025 |

| Applicable for | Employees, employers, and the self-employed |

Explore related products

![Manual of Compensation and Liability Insurance ; Rules and Rates. (1916) [Leather Bound]](https://m.media-amazon.com/images/I/61FbOFgXaEL._AC_UY218_.jpg)

What You'll Learn

![]()

Employee thresholds and rates

National Insurance is a payment made to HMRC by employees, employers, and the self-employed. Class 1 National Insurance contributions are only paid by employees who receive a salary; self-employed individuals do not pay Class 1 National Insurance but may pay Class 2 and Class 4 National Insurance. As an employee, Class 1 National Insurance contributions will be deducted from your salary by your employer every time payroll is run.

For the 2025/26 tax year, the employee rate of National Insurance Contributions is 8% from the primary threshold to the Upper Earnings Limit and 2% thereafter. If you are employed part-time and work only a few hours a week, you may not earn enough to pay any Class 1 National Insurance contributions. If you earn less than £125 per week or £542 per month (the lower earnings limit for 2025/26), you pay no Class 1 NIC. If you have earnings above the lower earnings limit but below the primary threshold (£242 per week or £1,048 per month for 2025/26), you are treated as having paid NICs without actually making a payment. This means your National Insurance record is registered with contributions at no cost to you.

If you have two jobs and expect to pay Class 1 NIC on weekly earnings of at least £967 throughout the 2025/26 tax year in one of the jobs, you can ask to defer payment of NIC in the other job. If you are paid monthly, you must expect to pay Class 1 NIC on monthly earnings of at least £4,189 throughout the whole tax year in one of the jobs. You can make an application for deferment of Class 1 NIC using form CA72A.

It is important to note that National Insurance rates and thresholds can change over time. For example, the main employee NIC rate was 12% from 6 April 2023 to 5 January 2024, after which it was reduced to 10%.

Subaru or Jeep: Which Brand Offers Better Insurance Rates?

You may want to see also

Explore related products

![]()

Employer rates

Employers pay Class 1 National Insurance contributions (NIC) on behalf of their employees. These contributions are deducted from the employees' salaries every time payroll is run. The rate of Class 1 NIC that an employer must pay depends on the employee's salary and whether the employee works full-time or part-time.

For the 2025/26 tax year, if an employee earns less than £125 per week (£542 per month), they are exempt from paying Class 1 NIC. If an employee's earnings are above this lower threshold but below the primary threshold of £242 per week (£1,048 per month), they are treated as having paid NICs without actually having to make a payment. This means that their National Insurance record is registered with contributions, but at no cost to them.

On the other hand, if an employee works part-time and only a few hours a week, they may not earn enough to pay any Class 1 NIC. In this case, their employer would not be required to deduct any Class 1 NIC from their salary.

It's important to note that Class 1 NIC rates and thresholds can change over time. For example, from 6 April 2025, the Employers' National Insurance Contributions will rise by 1.2% to 15%. Additionally, the employers' secondary threshold will reduce from £9,100 to £5,000 per annum, further increasing the NIC payable by employers.

Understanding Comprehensive Coverage with Auto Insurance

You may want to see also

Explore related products

![]()

Employee status and eligibility

In terms of employment status, an individual must be employed to be eligible for Class 1 NI. This encompasses full-time and part-time employees, as well as company directors. Self-employed individuals are not required to pay Class 1 NI; instead, they may be liable for Class 2 and Class 4 NI contributions. Additionally, those with multiple jobs, including a primary job and a side gig, may be subject to both Class 1 NI and potentially Class 4 NI, depending on their overall income.

Income levels also play a pivotal role in determining eligibility for Class 1 NI. For the 2025/2026 tax year, the Primary Threshold (PT) for Class 1 NI is set at £242 per week, £1,048 per month, or £12,570 per year. Employees whose earnings surpass this threshold become liable to pay Class 1 NI contributions. It is worth noting that individuals earning below the PT may voluntarily choose to pay Class 3 NI contributions to ensure they don't miss out on certain benefits.

The rate at which Class 1 NI contributions are calculated is also tied to income levels. Once an employee's income exceeds the PT, they are subject to an 8% contribution rate up to the Upper Earnings Limit (UEL). Beyond the UEL, which stands at £50,270 annually, the contribution rate drops to 2%. Individuals whose earnings exceed the UEL are considered Higher Rate earners.

It is important to emphasize that employers play a crucial role in facilitating their employees' Class 1 NI contributions. Employers are responsible for deducting the appropriate amount from their employees' salaries through the Pay As You Earn (PAYE) system. This is done automatically, ensuring employees' contributions are made each month.

Unbuckling Auto Insurance and Lender Loopholes

You may want to see also

Explore related products

![]()

Multiple jobs

National Insurance is a contribution paid by UK employers, employees, and the self-employed that counts toward certain benefits. These benefits include the State Pension, maternity allowance, and bereavement support payments. The right to these benefits depends on an individual's National Insurance class.

Class 1 National Insurance (or Class 1 NIC) is paid by both the employer and the employee. The employee's contribution to Class 1 NIC is known as the "primary contribution," while the employer's contribution is known as the "secondary contribution." The amount of Class 1 NIC paid depends on the individual's age and income.

If you have multiple jobs, there are separate thresholds for each job as long as they are with different employers. For the 2025/26 tax year, if you have two jobs and expect to pay Class 1 NIC on weekly earnings of at least £967 throughout the tax year in one of the jobs, you can ask to defer payment of NIC in the other job. If you are paid monthly, you must expect to pay Class 1 NIC on monthly earnings of at least £4,189 throughout the tax year in one of the jobs. You can apply for deferment of Class 1 NIC using form CA72A.

It is important to note that if you are a woman who married before April 1977, you may have elected by May 1977 to pay a reduced rate of Class 1 NIC. Additionally, if you earn less than the Lower Earnings Limit of £125 per week for 2025/26, you do not pay any Class 1 NIC, nor are you treated as paying any NIC, so you do not get any contributions registered on your NIC record.

Multi-State Auto Insurance: Double Coverage?

You may want to see also

Explore related products

$25.64 $26.99

![H&R Block Tax Software Deluxe + State 2024 with Refund Bonus Offer (Amazon Exclusive) Win/Mac [PC/Mac Online Code]](https://m.media-amazon.com/images/I/51+fonAXhPL._AC_UY218_.jpg)

$12.49 $21.99

![[OLD VERSION] TurboTax Deluxe 2024 Tax Software, Federal & State Tax Return [PC/MAC Download]](https://m.media-amazon.com/images/I/71UbHaUeeUL._AC_UY218_.jpg)

![]()

Employee entitlements

National Insurance Contributions (NICs) are the UK's second-largest tax, raising around £170 billion in 2024-25. They are paid by employees, the self-employed, and employers. Employees typically pay Class 1 National Insurance, with the amount depending on their earnings. This is calculated each time an employee is paid, so the amount may vary if their pay changes. Employees are normally paid through the Pay As You Earn (PAYE) system, so their NICs are automatically deducted from their salary.

Employees earning at least the lower earnings limit (LEL) are treated as having paid NICs, even if they earn below the primary threshold and do not actually pay NICs. For 2024-25, the LEL is £123 per week. People who are not in paid work, including those who are unemployed, sick, disabled, or caring for a child under 12 or someone with a disability, can receive National Insurance credits towards their benefit entitlements.

Employees can also make voluntary contributions to fill gaps in their record and boost their pension entitlement. This is typically done by UK citizens living abroad to maintain their entitlement to benefits when they return.

NICs are linked to various contributory benefits, including the State Pension, Maternity Allowance, 'new-style' Jobseeker's Allowance, and 'new-style' Employment and Support Allowance. To receive the full new State Pension, individuals need 35 qualifying years of contributions or credits. With fewer than 35 years, the pension amount is reduced, and with fewer than 10 qualifying years, no pension is paid.

Statutory maternity pay is also linked to NICs. While it is not necessary to have paid NICs in the UK to claim maternity allowance, any payments made will increase the entitlement.

Broken Finger: Can You Still Drive and Stay Insured?

You may want to see also

Frequently asked questions

The rate for most employees is 8% from the Primary Threshold to the Upper Earnings Limit and 2% thereafter.

Employees, employers and the self-employed pay Class 1 National Insurance. Employees who are limited company directors also pay Class 1 National Insurance.

If you are an employee, your Class 1 National Insurance contributions will be deducted from your salary by your employer.

Yes, if you have more than one job with different employers, you will need to pay Class 1 National Insurance for each job.

If you earn less than £125 a week (£542 a month), you don't have to pay any Class 1 National Insurance.

![[OLD VERSION] TurboTax Home & Business 2024 Tax Software, Federal & State Tax Return [PC/MAC Download]](https://m.media-amazon.com/images/I/71b5aAzdXOL._AC_UY218_.jpg)