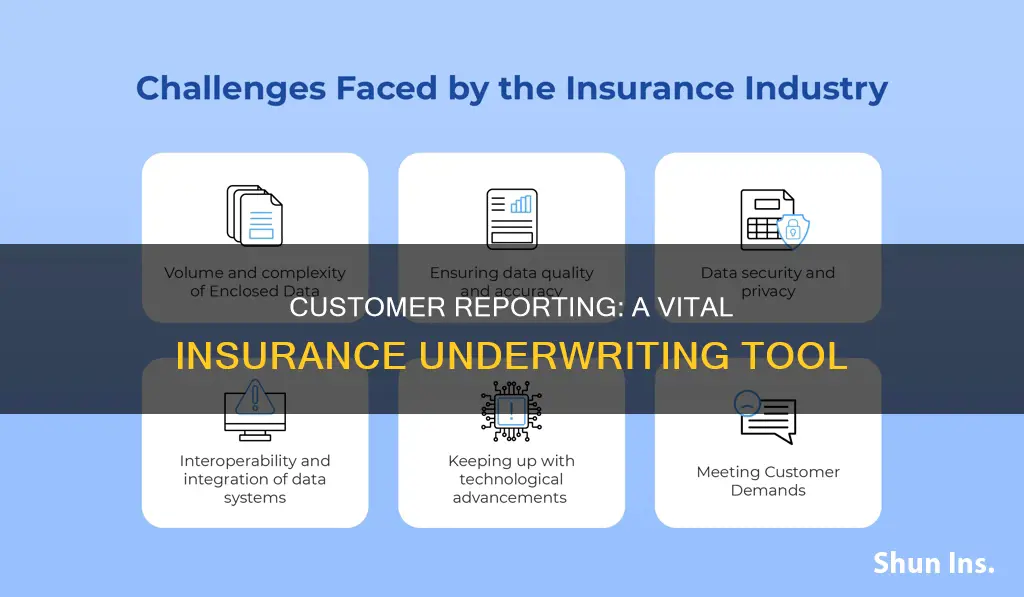

Insurance underwriting is a critical process for insurance companies to maintain a healthy loss ratio and ensure profitability and long-term sustainability. It involves evaluating the risk associated with insuring an individual or entity and determining the appropriate premium cost. Customer reporting is an integral part of the underwriting process, where consumer reports are used to assess an applicant's risk profile. These reports may include information on credit history, medical conditions, driving records, criminal activity, and participation in dangerous sports. When using consumer reports, insurance companies must comply with regulations such as the Fair Credit Reporting Act (FCRA) to protect consumer privacy and ensure accurate reporting. The process of customer reporting in insurance underwriting involves collecting, analyzing, and utilizing customer data to make informed decisions about insurance coverage and pricing.

| Characteristics | Values |

|---|---|

| Purpose | To evaluate risk and determine insurance coverage and pricing |

| Information Sources | Consumer reports, financial statements, actuarial reports, claims history, credit rating, home inspections, etc. |

| Compliance | Fair Credit Reporting Act (FCRA), requiring consumer consent and protection of privacy |

| Adverse Action | Notice required when action (e.g., denial, rate increase) is based on consumer report, including right to dispute |

| Underwriter Role | Assessing and pricing risk, determining monthly premiums, considering profitability and marketing |

| Challenges | Complexity due to unique risk characteristics, need for fast decisions, balancing profitability and risk |

Explore related products

What You'll Learn

![]()

Consumer reports may contain errors

Consumer reports play a critical role in insurance underwriting, helping underwriters assess and price risk accurately. These reports contain information about a person's credit history, medical conditions, driving record, criminal activity, and even their participation in dangerous sports. While consumer reports are essential in the underwriting process, it is important to acknowledge that they may contain errors.

Credit report errors, for instance, can have significant implications for consumers. Common mistakes include accounts or loans that appear unpaid even when they have been settled, individual loans listed multiple times, or debts incorrectly reported as being in collections. Other errors may include misspelled names, wrong addresses, or incorrect birth dates. More serious issues, such as "mixed files," occur when information from someone with a similar name or Social Security number appears in the wrong report, or when fraudulent accounts are listed due to identity theft.

These inaccuracies can lead to lower credit scores, higher interest rates on loans, and even impact employment and housing opportunities. In fact, an investigation by Consumer Reports revealed that over one-third of consumers found errors in their credit reports, with 29% discovering personal information errors and 11% finding account information mistakes.

When consumer reports are used in insurance underwriting, it is crucial to comply with the Fair Credit Reporting Act (FCRA). The FCRA is designed to protect consumer privacy and ensure the accuracy of information provided by consumer reporting agencies (CRAs). If an adverse action is taken based on information in a consumer report, such as denying insurance, increasing rates, or terminating a policy, the FCRA requires providing a notice to the consumer. This notice must include the details of the CRA that supplied the report and inform the consumer of their right to dispute any inaccurate or incomplete information.

To dispute errors in a consumer report, individuals can file a written dispute with the CRA, following their instructions for submission. The CRA then has 30 business days to investigate the claims and make necessary corrections. It is important to note that consumers may have difficulty getting mistakes corrected, and high consumer complaints about dispute investigations persist. Therefore, it is essential to carefully review consumer reports and proactively dispute any identified errors to ensure accuracy and mitigate potential negative consequences.

Reporting Traffic Tickets: New Insurance, New Rules?

You may want to see also

Explore related products

![]()

The Fair Credit Reporting Act (FCRA)

The FCRA regulates the collection, dissemination, and use of consumer information, including consumer credit information. It was originally passed in 1970 and is enforced by the U.S. Federal Trade Commission, the Consumer Financial Protection Bureau, and private litigants. The Act protects information collected by consumer reporting agencies, such as credit bureaus, medical information companies, and tenant screening services.

Under the FCRA, users of information for credit, insurance, or employment purposes (including background checks) have specific responsibilities. They can only obtain consumer reports for permissible purposes under the FCRA and must notify the consumer when an adverse action is taken based on such reports. Users must also identify the company that provided the report so that the consumer can verify or contest its accuracy and completeness.

In addition, companies that provide information to consumer reporting agencies have specific legal obligations, including the duty to investigate disputed information. Creditors who furnish consumer information to CRAs must provide complete and accurate information, investigate consumer disputes, correct or delete inaccurate information within 30 days, and inform consumers about negative information placed on their credit reports within one month.

The FCRA also allows consumers to recover punitive damages if their rights under the Act are violated willfully. Consumers can request a free copy of their consumer report from each credit reporting agency once a year through telephone, mail, or a government-authorized website.

Trees: House Insurance Savings?

You may want to see also

Explore related products

![]()

CLUE (Comprehensive Loss Underwriting Exchange)

An insurer may request a CLUE report when an individual applies for coverage or requests a quote. The insurer uses the individual's claims history to decide whether to offer coverage and how much to charge. Studies show a relationship between past claims and future claims. Individuals can check for inaccurate or unrelated information that could result in higher premiums. LexisNexis will provide one free report every 12 months if requested.

CLUE reports contain vital information about the driver, vehicles, policy, and reported claims. They can help consumers receive more accurate auto insurance quotes. For example, when a new driver is added to a policy, such as a teenager who has just received their license, it is critical to have a view of the entire household of drivers.

LexisNexis also collects and reports driving behaviour data ("Telematics OnDemand") for auto insurance pricing. This data may contain errors, as public records and commercially available data sources are sometimes reported or entered inaccurately.

Insuring Your Home: Choosing the Right Cover

You may want to see also

Explore related products

![]()

Evaluating risk

Underwriters consider numerous variables when evaluating risk. For example, in homeowners' insurance, underwriters must consider hazards that may trigger liability claims, such as accidental drownings due to unfenced swimming pools or slip and fall injuries from cracked sidewalks. They employ an algorithmic rating method, taking into account factors such as an applicant's credit rating. Underwriters also assess the group's risk as a whole, calculating an appropriate premium level and aggregate claims limit.

Consumer reports are commonly used by underwriters to gather information for risk evaluation. These reports may include details about a person's credit history, medical conditions, driving record, criminal activity, and participation in dangerous sports. When using consumer reports, underwriters must comply with the Fair Credit Reporting Act (FCRA), which protects the privacy of consumer information and ensures its accuracy. Obtaining consumer consent is also crucial, especially when dealing with medical information.

The underwriting process is crucial for insurance companies to maintain a healthy loss ratio and achieve profitability. It involves a complex assessment of unique risks, requiring underwriters to balance portfolio growth, profitability, and product marketing. Fast underwriting is essential in the small and medium-sized enterprise (SME) sector due to the small premiums associated with each account. Underwriters must also be mindful of the competition and avoid being too conservative in their approach to remain competitive in the market.

Overall, evaluating risk is a fundamental aspect of insurance underwriting, requiring expertise, data analysis, and a comprehensive understanding of the insured's unique characteristics. By assessing risks effectively, underwriters can determine appropriate coverage and pricing, ensuring the long-term sustainability and profitability of the insurance company.

Farmers Insurance Office in Utah: A Guide to Finding Their Location

You may want to see also

Explore related products

![]()

Underwriter approval

Underwriting is a critical process for any insurance company to maintain a healthy loss ratio. It is the core of the business and the primary driver of its financial performance. Underwriters are specialists who assess the risks of providing coverage for individuals or assets and determine the appropriate cost of that coverage. They assume the risk involved in a contract with an individual or entity in return for a premium or monthly payment.

To obtain underwriter approval, it is essential to provide all the required information with the initial submission. This includes relevant information regarding the risk being insured. For example, a D&O insurance application may include financial statements, actuarial reports, ownership charts, information on board composition, company registration, and a list of directors and officers applying for coverage. Providing comprehensive information upfront helps avoid delays and ensures a smoother underwriting process.

In some cases, the underwriter may need to meet with the insurance broker or the applicant directly to verify the information provided in the application. This verification step is particularly important for large accounts, where the potential risks and financial implications are significant.

Underwriters also need to evaluate the group's risk as a whole and calculate an appropriate premium level. They consider various factors, such as an applicant's credit rating, medical history, driving record, criminal activity, and participation in dangerous sports. By assessing these factors, underwriters can determine the likelihood of a covered event occurring and set the monthly premium cost accordingly.

Obtaining underwriter approval is a meticulous process that requires a thorough evaluation of risks and careful consideration of relevant information. It is a critical step in the insurance underwriting process, ensuring that insurance companies offer coverage at a price that balances profitability and competitiveness in the market.

Report Insurance SSI: A Step-by-Step Guide

You may want to see also

Frequently asked questions

Customer reporting in insurance underwriting is a critical process for insurance companies to maintain a healthy loss ratio. It involves evaluating a customer's risk profile by considering various factors, such as credit history, medical conditions, driving record, criminal activity, and claims history, to determine whether to offer coverage and calculate premium costs.

The key components include obtaining consumer reports or consumer-reporting agency (CRA) reports, such as CLUE (Comprehensive Loss Underwriting Exchange) reports, which provide claims history. Underwriters assess these reports to identify risks and determine coverage and pricing.

Customer reporting plays a pivotal role in insurance underwriting decisions. It helps underwriters assess the likelihood of a covered event occurring and calculate the financial impact on the insurer. This information is crucial for setting premium costs and ensuring the insurer's profitability and long-term sustainability.