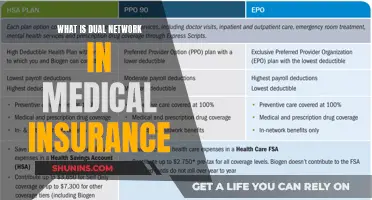

CYD, or Calendar Year Deductible, is an important term in health insurance. It refers to the amount of money that an insured person must pay towards their medical expenses before their health insurance policy starts contributing. The CYD runs from January 1st to December 31st and resets to $0 every January 1st. It applies to services such as x-rays, lab tests, hospitalisations, and doctor visits. The deductible amount varies between health insurance plans and impacts the financial responsibilities and overall healthcare costs of the insured individual.

| Characteristics | Values |

|---|---|

| Full Form | Calendar Year Deductible |

| Definition | Amount of money that you must spare from your income or other sources to cover your medical expenses before the health insurance you have taken can start contributing towards the costs |

| Timeframe | January 1 to December 31 |

| Reset Date | January 1 |

| Applicability | All the services that are subject to deductible, including x-rays, lab tests, hospitalizations, doctor visits, etc. |

| Impact | Out-of-pocket costs, insurance shopping decisions, and overall healthcare expenses |

| Coinsurance | Percentage of covered expenses that insured individuals must pay after meeting their deductible |

Explore related products

What You'll Learn

![]()

CYD meaning

CYD stands for Calendar Year Deductible. It refers to the amount of money that an individual must pay out-of-pocket towards their medical expenses for the year, before their health insurance provider starts contributing towards the costs. The CYD runs from January 1st to December 31st and resets to $0 every January 1st.

The amount of the CYD varies between different health insurance plans and can impact an individual's financial responsibilities and overall healthcare costs. For example, a plan with a high CYD will typically have lower premiums, but the individual must pay more upfront for medical costs. Conversely, a plan with a lower CYD will have higher premiums, but the insurance provider will start contributing towards costs sooner.

The CYD applies to all services that are subject to deductible, including x-rays, lab tests, hospitalizations, and doctor visits. It is important for individuals to carefully review and compare deductible amounts when selecting a health insurance plan to ensure it aligns with their healthcare needs and financial situation.

In addition to the CYD, there may also be coinsurance, which refers to the percentage of covered expenses that an individual must pay after meeting their deductible. For example, "30% coinsurance after CYD" means that the individual is responsible for paying 30% of the covered expenses after meeting their deductible.

Wisdom Teeth Removal: Dental or Medical Insurance Coverage?

You may want to see also

Explore related products

![]()

CYD and out-of-pocket costs

CYD, or Calendar Year Deductible, is an important concept in health insurance. It refers to the amount of money that an individual must pay out-of-pocket towards their medical expenses before their health insurance starts contributing towards the costs. In other words, it is the amount the insured must pay before their insurer covers a larger portion of their medical bills.

The CYD applies to all services that are subject to deductible, including x-rays, lab tests, hospitalisations, doctor visits, and prescription drugs. It is important to note that the CYD runs from January 1st to December 31st and resets to $0 every January.

Out-of-pocket costs refer to the total amount an individual must pay for a covered loss, including any deductibles, copays, or coinsurance that may apply. In the context of health insurance, out-of-pocket costs can include deductibles, copays for doctor visits and prescription drugs, and coinsurance for hospital stays. These costs can add up quickly, especially if an individual has a high-deductible health plan or incurs significant medical expenses.

Understanding the difference between CYD and out-of-pocket costs is crucial when selecting a health insurance policy. While the CYD represents the initial amount an individual must pay before their insurance coverage kicks in, out-of-pocket costs represent the total financial burden an individual may face when seeking medical care. By comparing different policies' CYDs and out-of-pocket maximums, individuals can make informed decisions about their healthcare coverage and choose a plan that best suits their needs and budget.

Additionally, it is worth noting that the relationship between deductibles and premiums is inversely proportional. A higher deductible typically leads to lower premiums, as the policyholder takes on more of the financial risk. Conversely, a lower deductible results in higher premiums, as the insurance company assumes a larger portion of the risk. Therefore, when considering a health insurance plan, it is essential to weigh the benefits of lower monthly payments against the potential for higher out-of-pocket costs in the event of medical treatment.

Get Life Insurance with Medical Problems: What You Need to Know

You may want to see also

Explore related products

![]()

CYD and insurance shopping decisions

CYD, or Calendar Year Deductible, is a crucial concept in health insurance. It refers to the amount of money an insured person must pay out of pocket towards their medical expenses before their health insurance starts contributing. The CYD runs from January 1st to December 31st and resets to $0 every January 1st.

When shopping for insurance, it is essential to understand the impact of CYD or deductible amounts on overall healthcare expenses and out-of-pocket costs. Insured individuals must carefully review and compare deductible amounts across different insurance plans to ensure they select a plan that aligns with their healthcare needs, budget, and risk tolerance. A higher deductible plan often comes with lower premiums, but the insured party must be able to cover more upfront medical costs. Conversely, a lower deductible plan typically has higher premiums, but the insurance coverage kicks in sooner.

Coinsurance, often expressed as a percentage "after CYD", is another critical factor in insurance shopping decisions. It refers to the percentage of covered expenses that the insured individual must pay after meeting their deductible. For example, "20% coinsurance after CYD" means the insured person is responsible for paying 20% of the covered expenses after reaching their deductible. This percentage of coinsurance directly impacts the overall out-of-pocket costs for the insured.

Additionally, when considering insurance plans, it is worth noting that certain preventive care services, such as annual check-ups, may be covered at no additional cost to the insured. These services are typically outlined in the insurance plan's details and can vary depending on age and gender. Understanding these inclusions can help individuals make informed decisions about their healthcare coverage.

In summary, CYD, or Calendar Year Deductible, plays a significant role in insurance shopping decisions by influencing out-of-pocket costs and overall healthcare expenses. Individuals must carefully review deductible amounts, consider their healthcare needs and budget, and factor in coinsurance percentages to make informed choices about their health insurance coverage.

Understanding Insurance Medical Release Forms

You may want to see also

Explore related products

![]()

CYD and overall healthcare expenses

CYD, or Calendar Year Deductible, is a fundamental aspect of health insurance that insured individuals must understand. It refers to the amount of money that an insured person must pay out of their income or other sources to cover their medical expenses before their health insurance starts contributing towards the costs. The CYD runs from January 1st to December 31st and resets to $0 every January 1st.

The CYD directly influences out-of-pocket costs, insurance shopping decisions, and overall healthcare expenses. For example, if an individual has a $5,000 CYD, they must spend this amount on their medical care before their insurance plan starts contributing. This amount is separate from any premiums or copays that the individual may also be responsible for.

When selecting a health insurance plan, it is crucial to carefully review and compare deductible amounts to ensure they meet one's needs and budget. The deductible amount, or CYD, plays a significant role in insurance shopping decisions. Individuals must consider their healthcare needs, budget, and risk tolerance when choosing between plans with different deductible amounts.

Understanding the impact of deductible amounts on out-of-pocket costs is essential for making informed decisions about health insurance coverage. The CYD determines when an individual's healthcare insurance will start contributing towards their medical costs. Therefore, it is important to set a realistic CYD that one feels they can easily meet.

Additionally, the concept of coinsurance is relevant to CYD. Coinsurance refers to the percentage of covered expenses that an insured individual must pay after meeting their deductible. For example, "20% coinsurance after CYD" means that the individual is responsible for paying 20% of the covered expenses after reaching their CYD. This further impacts the overall healthcare expenses for the insured individual.

Understanding Your Annual Medical Out-of-Pocket Maximum

You may want to see also

Explore related products

![Princess Cyd [DVD]](https://m.media-amazon.com/images/I/61vzjwaufML._AC_UY218_.jpg)

![]()

Coinsurance after CYD

CYD, or Calendar Year Deductible, is the amount of money that an insured person must pay before their healthcare insurance starts contributing to their medical costs. The CYD applies to services such as x-rays, lab tests, hospitalizations, and doctor visits, and it runs from January 1st to December 31st of each year, resetting to $0 on January 1st.

Now, let's discuss coinsurance after CYD:

Coinsurance is a type of out-of-pocket cost for healthcare that applies after you have met your deductible for the year. While a deductible refers to the amount you pay before your insurance coverage kicks in, coinsurance is the percentage of medical costs that you continue to pay even after meeting your deductible. For example, if you have a 20% coinsurance requirement, you will pay 20% of each medical bill, and your health insurance will cover the remaining 80%. This arrangement continues until you reach your out-of-pocket maximum for the policy year. At that point, your insurer will cover 100% of your covered medical expenses for the rest of that year.

The amount of coinsurance you pay depends on the specific health insurance plan you have chosen. Some plans may offer 0% coinsurance, meaning you pay nothing towards the medical costs, while others may have higher percentages such as 20% or 25%. It is important to review the details of your health plan to understand the coinsurance requirements and how they work alongside any copays or deductibles.

Coinsurance and deductibles work together but usually consecutively. Once you have met your deductible for the year, coinsurance typically applies to all additional medical services for the remainder of that year. It is worth noting that copays may still apply even after you have met your deductible and started paying coinsurance.

Understanding how coinsurance works after meeting your CYD is crucial for estimating your potential out-of-pocket expenses when seeking medical care. It helps you anticipate your financial responsibility for healthcare services beyond just the monthly premiums you pay for your health insurance plan.

Undocumented Immigrants: Access to Medical Insurance?

You may want to see also

Frequently asked questions

CYD stands for Calendar Year Deductible.

A deductible is the amount of money you must pay towards your medical expenses before your insurance starts contributing.

CYD directly influences your out-of-pocket costs, insurance shopping decisions, and overall healthcare expenses.

CYD runs from January 1st to December 31st and resets to $0 every January 1st. You must pay your CYD before your insurance starts contributing towards your medical costs.

"20 after CYD" refers to coinsurance, which is the percentage of covered expenses you must pay after meeting your deductible. "20 after CYD" means you are responsible for paying 20% of covered expenses after meeting your deductible.