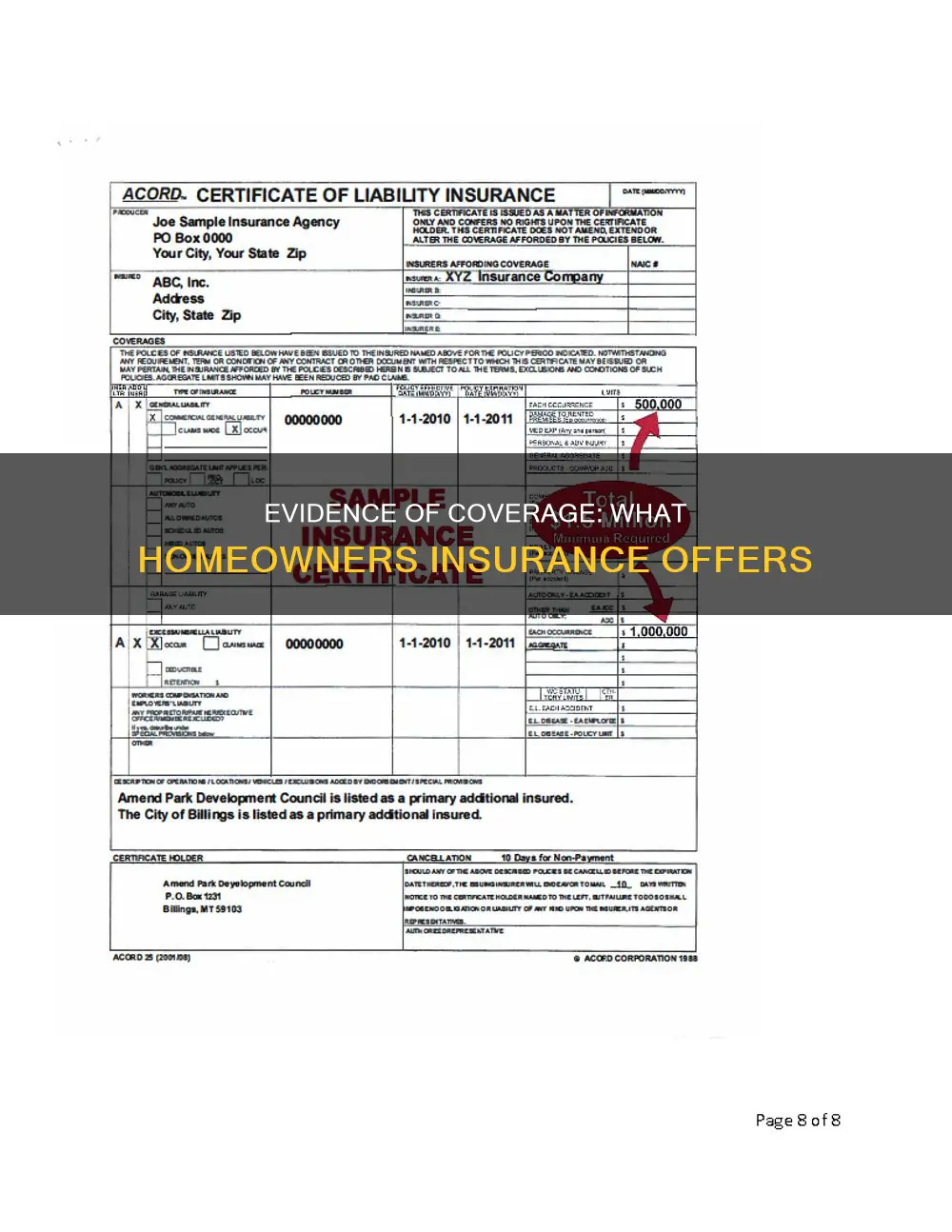

Whether you're a renter or a homeowner, you will likely need to provide evidence of insurance at some point. Evidence of insurance is a document that demonstrates that an individual or business has insurance coverage. In the context of homeowners insurance, evidence of insurance is crucial for protecting your financial interests in the property and ensuring compliance with any mortgage requirements. This evidence can be provided in various ways, such as through a declarations page, a full policy document, or a temporary proof of insurance called a homeowners insurance binder. Understanding the concept of evidence of insurance is essential for landlords, lenders, and homeowners alike, as it provides assurance that the property is adequately insured and helps manage financial risks.

| Characteristics | Values |

|---|---|

| Purpose | To demonstrate that a property is adequately insured |

| Types of coverage | First-party coverages (protects the insured from losses resulting from injuries to themselves and damage to their belongings and property) and third-party coverages (protects the insured from liability for injuries or damages caused to other people or their belongings and property) |

| Forms | ACORD 27 for residential and small commercial properties, ACORD 28 for large commercial properties, and ACORD 24 for property insurance coverage |

| What it covers | Property description, coverage extent, nature and scope of protection, and mortgage information |

Explore related products

What You'll Learn

![]()

Fire, theft, vandalism, and natural disasters

Homeowners insurance is designed to protect residences and valuables from damaging incidents such as fire, theft, vandalism, and certain natural disasters. The physical structure of the insured property is protected under dwelling coverage, while personal property coverage, or contents coverage, protects belongings inside the home.

Fire is one of the most common causes of damage to homes, and most homeowners insurance policies cover the cost of repairing or rebuilding the home, as well as replacing personal belongings damaged in the fire. Standard policies that cover fire also typically cover the cost of additional living expenses incurred due to the fire, such as hotel stays, rentals, or restaurant meals.

Theft is generally covered under homeowners insurance, protecting the policyholder from losses resulting from the theft of their belongings. However, it is important to note that coverage limits may apply, and certain items may not be covered or may have limited coverage, such as jewellery or other valuable possessions.

Vandalism is typically covered under an all-risks or all-perils policy unless specifically excluded. Vandalism coverage usually applies to unoccupied homes but may not extend to vacant homes after a certain period. It is important for policyholders to carefully review their insurance policies to understand the scope of coverage, exclusions, and terms regarding vandalism.

Natural disasters , such as lightning, thunderstorms, hurricanes, and hail, are typically covered by homeowners insurance. However, not all natural disasters are included, and basic policies often exclude coverage for earthquakes and floods. If you live in an area prone to these types of disasters, you may need to purchase separate catastrophe insurance or add coverage to your existing policy.

In summary, homeowners insurance provides financial protection against fire, theft, vandalism, and certain natural disasters. It is important for homeowners to carefully review their policies to understand the specific perils covered and any exclusions or limitations that may apply.

Home Insurance Discounts: How to Save Money

You may want to see also

Explore related products

![]()

Liability coverage

Personal liability coverage, a subset of liability coverage, is designed to safeguard the policyholder and their family members from the financial consequences of liability claims. This includes protection against accidental bodily injury or property damage caused by the policyholder, their family, or their pets. For example, if a guest is injured on the property due to negligence, such as an unrepaired railing, personal liability insurance may cover their medical bills and legal costs if they decide to sue.

In the context of business transactions, a Certificate of Insurance (COI) is often required to outline the liability coverage provided by the insurance policy. This document includes crucial details such as the insurer's name and serves as evidence of the policyholder's current coverage. Similarly, for residential properties, evidence of insurance is typically conveyed through a form called ACORD 27, which can also include mortgage information.

Liability Coverage: Protecting Your Business Under Homeowners Insurance

You may want to see also

Explore related products

![]()

Personal property coverage

The amount of personal property coverage you can select may vary depending on the type of property insurance you have. For example, your homeowners insurance policy may include a certain percentage of your dwelling coverage for personal property. If your policy's dwelling limit is $200,000, you may have $100,000 in personal property insurance coverage. Many renters insurance policies also provide personal property coverage options, which can range from $10,000 to $500,000.

It is important to note that personal property coverage typically applies to movable items in your home. Items that are permanently installed, such as certain appliances, are usually covered under dwelling coverage rather than personal property. Additionally, there may be limits to how much your policy will pay out, and certain risks, like floods or earthquakes, may not be covered unless you purchase separate endorsements.

To ensure you have adequate coverage, you can schedule an item or add an insurance rider to your policy. This means adding a specific item to your policy, which may raise your premium but provides extra protection for valuable items. For example, if you have an expensive engagement ring, you may want to schedule it separately to ensure it is covered for its full value.

Understanding Homeowner Insurance: Prorated Quotes Explained

You may want to see also

Explore related products

![]()

Dwelling coverage

The perils covered by a homeowner insurance policy vary by policy but can include fire, theft, vandalism, and certain natural disasters. For example, dwelling coverage on a standard policy typically won't protect against damage caused by water damage from flooding. However, depending on your location, you may have the option to buy a separate flood insurance policy to protect your home's structure and belongings against water damage.

The amount of dwelling coverage you need is determined by your insurer, based on the cost to rebuild your home from scratch. This is called the "replacement cost value" and is usually different from your home's fair market value. To determine the rebuild price, insurers may ask for specific information about your home, such as the type of roof, the year it was built, square footage, flooring, and the number of bathrooms.

Solar Panels: Insurance Impact

You may want to see also

Explore related products

![]()

Medical expenses and legal costs

Medical payments coverage is a standard feature of most homeowners insurance policies. It covers minor medical expenses incurred by neighbours, guests, or any non-residents who are injured on the policyholder's property, regardless of who is at fault. This coverage is meant as a “gesture of goodwill” to prevent lawsuits and subsequent high-dollar liability claims. Coverage F, as it is known, typically covers expenses up to $5,000 and includes ambulance rides, hospital bills, X-rays, doctor and surgeon fees, physical therapy, prosthetic devices, and emergency dental treatment. It may also cover funeral expenses if the injury results in death. It is important to note that medical payments coverage does not apply to injuries sustained by the policyholder or their family members or anyone who lives in the household.

Personal liability coverage, on the other hand, covers more expensive medical bills and litigation costs in the event that the policyholder is found legally responsible for damages. This coverage typically has much higher limits, often starting at $100,000, and can also pay for property damage. It may also apply if the policyholder, a family member, or a pet injures someone away from the insured property. Personal liability coverage usually requires a deductible, which is the amount the policyholder must pay before the insurance coverage kicks in.

Legal expenses cover, also known as family legal protection, is not compulsory but is often included as standard or offered as an optional extra in home insurance policies. This type of insurance covers the costs of legal advice and representation related to property ownership, such as boundary disputes, home renovations, medical malpractice, and employment disputes. It can protect the policyholder from the costs of being sued or of making a claim against someone else. Legal expenses cover typically ranges from £50,000 to £100,000, with an average annual cost of under £35. 'Before the event' insurance covers incidents that occur while the policy is active, while 'after the event' insurance can be purchased after a triggering event but before major legal expenses are incurred, usually to cover the other party's legal fees if the policyholder loses the case.

Home Insurance: Does It Cover Workers on Your Property?

You may want to see also

Frequently asked questions

Evidence of coverage in homeowner's insurance is a document that shows your landlord, lender, or other individuals that you have active insurance on your home.

Homeowner's insurance covers the cost of repairing or rebuilding a home in the event of damage or natural disasters, as well as the cost of replacing personal belongings. It also includes liability coverage, which provides financial protection if a policyholder damages their property or injures someone else on it.

A certificate of insurance outlines the liability coverage provided by the insurance policy and includes details such as the insurer's name. Evidence of insurance, on the other hand, provides detailed information about property insurance coverage, including what assets are covered and the nature and scope of protection.

You can usually download your homeowner's insurance policy from your insurer's website or request a copy from a representative via email, fax, or phone call. Your insurance company may also send you a "homeowner's insurance binder," which serves as temporary proof of insurance.