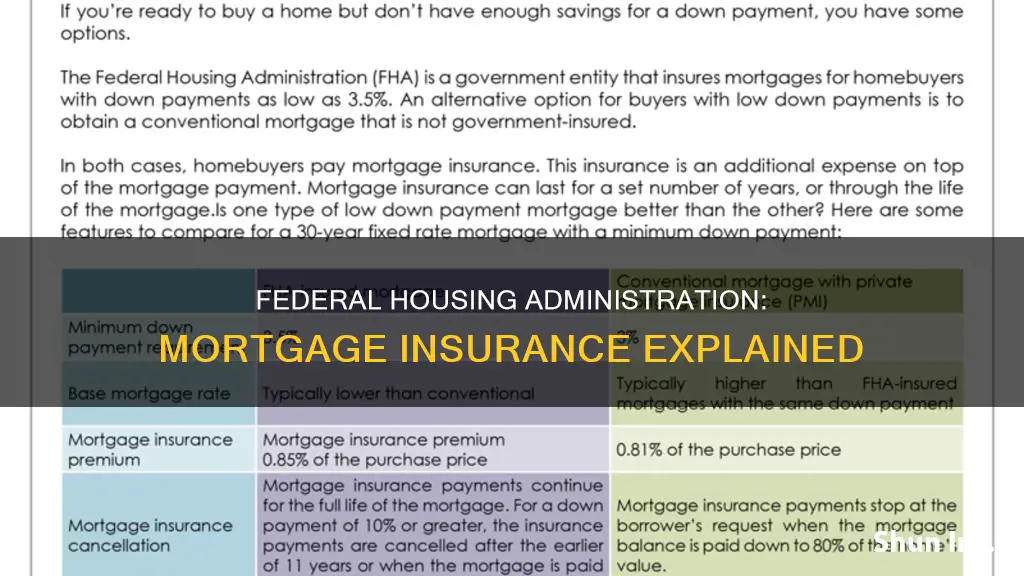

The Federal Housing Administration (FHA) offers mortgage insurance to borrowers who might find it difficult to obtain loans otherwise. FHA mortgage insurance is a type of insurance that protects lenders against losses in the event of a homeowner defaulting on their mortgage loans. Borrowers who qualify for an FHA loan are required to purchase mortgage insurance, with the premium payments going to the FHA. FHA loans are designed to help low- to moderate-income families attain homeownership, and they are particularly popular with first-time homebuyers.

| Characteristics | Values |

|---|---|

| Type of insurance | Mortgage insurance |

| Insurer | Federal Housing Administration (FHA) |

| Insured | Lenders |

| Protection | Against losses from homeowners defaulting on mortgage loans |

| Insured mortgages | On single-family and multi-family homes, manufactured homes, and hospitals |

| Requirements | Established by FHA |

| Availability | Throughout the United States and its territories |

| Applicant | Borrowers who qualify for an FHA loan |

| Applicant's credit score | Lower than usually required |

| Applicant's down payment | Lower than usually required |

| Applicant's income | Low to moderate |

| Applicant's status | First-time homebuyers |

| Mortgage insurance premium (MIP) | Two types: upfront and monthly |

| Upfront MIP | 1.75% of the base loan amount |

| Monthly MIP | Included in the monthly payment |

Explore related products

What You'll Learn

- FHA loans are insured by the government and issued by approved lenders

- FHA borrowers must pay two types of mortgage insurance premiums

- FHA insurance lowers the risk to lenders and makes it easier for borrowers to qualify

- FHA mortgage insurance provides lenders with protection against losses

- FHA loans are designed to help low- to moderate-income families

![]()

FHA loans are insured by the government and issued by approved lenders

The Federal Housing Administration (FHA) provides mortgage insurance on loans made by approved lenders. FHA loans are a form of home mortgage insured by the government and issued by approved lenders, such as banks. The FHA was created in 1934 to reduce the risk to lenders and make it easier for borrowers to qualify for home loans.

FHA loans are designed to help low- to moderate-income families attain homeownership, and they are particularly popular with first-time homebuyers. They are available to everyone, even those who can afford conventional mortgages. FHA loans require a lower minimum down payment than many conventional loans, and applicants may have lower credit scores than is usually required. Due to FHA insurance, approved lenders are more willing to lend to homebuyers with low credit scores and small down payments.

FHA borrowers must pay two types of mortgage insurance premiums (MIPs)—one upfront and the other monthly. The upfront MIP is equal to 1.75% of the base loan amount. For example, if you're issued a home loan for $350,000, you'll pay an upfront MIP of $6,125. You can pay the upfront MIP at the time of closing or add the amount to the loan. These payments go to the FHA.

Mortgage insurance lowers the risk to the lender of granting a loan. If the borrower falls behind on their payments, the lender is protected against losses. However, it increases the cost of the loan for the borrower.

Reporting Insurance Fraud: What You Need to Know

You may want to see also

Explore related products

$13.25

![]()

FHA borrowers must pay two types of mortgage insurance premiums

The Federal Housing Administration (FHA) provides mortgage insurance on single-family, multifamily, manufactured home, and hospital loans made by FHA-approved lenders. FHA loans are designed to help low- to moderate-income families attain homeownership and are particularly popular with first-time homebuyers.

The annual MIP is paid monthly and the cost varies depending on factors such as the base loan amount, loan term, and down payment size. For example, if you have a loan term of more than 15 years and a base loan amount of $726,200 or less, your annual MIP will be 0.50% of the base loan amount. With a down payment of 10% or more, you can remove the MIP after 11 years, whereas a down payment of less than 10% will result in the MIP lasting for the entire loan term.

FHA MIP provides protection for lenders in the event of default on the loan, allowing them to offer loans with lower down payment requirements and more flexible credit requirements. By reducing the risk to lenders, the FHA makes it easier for borrowers to qualify for home loans and achieve homeownership.

Reporting Insurance Fraud in Indiana: What You Need to Know

You may want to see also

Explore related products

![]()

FHA insurance lowers the risk to lenders and makes it easier for borrowers to qualify

The Federal Housing Administration (FHA) offers mortgage insurance on loans made by FHA-approved lenders. FHA mortgage insurance is a type of insurance that protects lenders against losses if a homeowner defaults on their mortgage loan. By insuring these loans, the FHA reduces the risk to lenders and makes it easier for borrowers to qualify for home loans.

The FHA was created in 1934 during the Great Depression when the housing industry was in trouble. Default and foreclosure rates had skyrocketed, and only one in ten households owned their homes. The FHA was established to reduce the risk to lenders and make it easier for borrowers to obtain home loans.

FHA loans are mortgages intended for borrowers who might find it difficult to obtain loans otherwise. They are designed to help low- to moderate-income families attain homeownership and are particularly popular with first-time homebuyers. FHA loans require a lower minimum down payment than conventional loans, and applicants may have lower credit scores. Due to the FHA insurance, lenders are more willing to lend to homebuyers with low credit scores and small down payments.

To qualify for an FHA loan, borrowers must purchase mortgage insurance, with the premium payments going to the FHA. There are two types of mortgage insurance premiums (MIPs) required for an FHA loan: an upfront MIP and an annual MIP, which is paid monthly. The upfront MIP is equal to 1.75% of the base loan amount, and it can be paid at the time of closing or rolled into the loan. The monthly MIP is included in the borrower's total monthly payment to the lender.

FHA mortgage insurance lowers the risk to lenders by providing protection against losses in the event of a homeowner's default. With FHA insurance, lenders bear less risk because the FHA will pay a claim to the lender if a homeowner defaults on their mortgage. This makes it easier for borrowers to qualify for FHA-insured loans, as lenders are more willing to lend to those who might not otherwise meet the strict requirements of conventional loans.

UPS Insurance: Worth the Cost?

You may want to see also

Explore related products

![]()

FHA mortgage insurance provides lenders with protection against losses

The Federal Housing Administration (FHA) provides mortgage insurance on single-family, multifamily, manufactured home, and hospital loans made by FHA-approved lenders. FHA mortgage insurance provides lenders with protection against losses resulting from homeowners defaulting on their mortgage loans.

Congress created the FHA in 1934 during the Great Depression to reduce the risk to lenders and make it easier for borrowers to qualify for home loans. At that time, the housing industry was in trouble due to high default and foreclosure rates, and only one in ten households owned their homes. The FHA was designed to help low- to moderate-income families attain homeownership, and it is particularly popular with first-time homebuyers.

FHA loans are mortgages intended for certain borrowers who might find it difficult to obtain loans otherwise due to low credit scores or small down payments. FHA borrowers are required to purchase mortgage insurance, with the premium payments going to the FHA. The FHA insurance encourages banks to lend to homebuyers with low credit scores and small down payments.

FHA loans require two types of mortgage insurance premiums (MIPs)—one upfront and the other paid monthly. The upfront MIP is equal to 1.75% of the base loan amount, and it can be paid at the time of closing or rolled into the loan. The monthly MIP is included in the borrower's monthly payment to the lender.

By providing mortgage insurance, the FHA reduces the risk to lenders and protects them against losses in the event of a homeowner's default. The FHA will pay a claim to the lender if a homeowner defaults on their mortgage, ensuring that the lenders bear less risk.

Insurance Code: Finding It in a Police Report

You may want to see also

Explore related products

![]()

FHA loans are designed to help low- to moderate-income families

The Federal Housing Administration (FHA) provides mortgage insurance on single-family and multifamily homes, as well as manufactured homes and hospitals. FHA loans are insured by the government and issued by approved lenders. They are designed to help low- to moderate-income families attain homeownership, particularly first-time homebuyers.

FHA loans require a lower minimum down payment than conventional loans, and applicants may have lower credit scores. Due to the FHA insurance, lenders are more willing to lend to homebuyers who might not otherwise qualify for a loan. The insurance protects lenders against losses in the event of homeowners defaulting on their mortgage loans.

Borrowers who qualify for an FHA loan are required to purchase mortgage insurance, with the premium payments going to the FHA. There are two types of mortgage insurance premiums (MIPs) for FHA loans: an upfront MIP, which is equal to 1.75% of the base loan amount, and a monthly MIP. These insurance payments increase the cost of the loan.

FHA loans are available to everyone, even those who can afford conventional mortgages. However, borrowers who can afford a substantial down payment may be better off with a conventional mortgage, as they can avoid the monthly mortgage insurance payments and get a lower interest rate. FHA loans are intended for certain borrowers who might find it difficult to obtain loans otherwise.

Pathology Reports: Insurance's Need-to-Know

You may want to see also

Frequently asked questions

It is a home mortgage insured by the government and issued by a bank or lender approved by the Federal Housing Administration.

FHA mortgage insurance is a type of insurance that is mandatory for all FHA loans. It includes an upfront cost, paid as part of the closing costs, and a monthly cost included in the monthly payment.

FHA mortgage insurance lowers the risk to the lender of making a loan. It provides lenders with protection against losses that result from homeowners defaulting on their mortgage loans.

FHA loans are designed for low- to moderate-income families who may find it difficult to obtain loans otherwise. They are particularly popular with first-time homebuyers.