Globe Life Insurance offers a range of life insurance products, including whole life insurance, which provides permanent coverage for the entirety of the policyholder's life as long as premiums are paid. One notable aspect of life insurance policies, including those offered by Globe Life, is the concept of contestability. Contestability refers to the period during which the insurance company can investigate and contest any claims made or the issuance of the policy due to potential misrepresentation on the application for coverage. This contestability period typically lasts for two years after the policy is issued, and it allows the insurance company to review and potentially dispute claims made during this timeframe.

| Characteristics | Values |

|---|---|

| Contestability period | Two years |

| Contestability | Insurance company can contest or investigate any claim made, or the issuance of the policy due to misrepresentation on the application for life insurance coverage |

| Whole life insurance | Yes |

| Purchase options | Agent, mail, online, phone |

| Customer satisfaction | Ranked No. 16 out of 21 companies in J.D. Power's 2024 U.S. Individual Life Insurance Study |

| Financial strength rating | A (Excellent) |

Explore related products

What You'll Learn

![]()

Contestability period

Contestability refers to the period when an insurance company can contest or investigate any claim made, or the issuance of the policy due to misrepresentation on the application for life insurance coverage. For most insurance companies, the contestability period is the two-year period following the date the policy is issued.

During the contestability period, the insurance company is given time to contest the policy if the insured person dies. Some life insurance policies have no time limit to submit a claim for a death benefit. If there is a time limit, the life insurance policy will have specific language detailing the time period in the life insurance policy issued. After a beneficiary files a claim, the death benefit payout is usually processed within 14-60 days, unless there are questions on the claim.

Globe Life Insurance offers whole life insurance, which is a type of permanent policy designed to cover your entire life as long as you pay the premiums. You are not able to purchase Globe Life whole life insurance online; you’ll have to work with an agent or purchase coverage by mail.

Globe Life has drawn far more than the expected number of complaints to state regulators for a company of its size, according to a NerdWallet analysis of data from the National Association of Insurance Commissioners. Globe Life ranked No. 16 out of 21 companies for customer satisfaction in J.D. Power's 2024 U.S. Individual Life Insurance Study.

Get a Copy of Your Life Insurance License

You may want to see also

Explore related products

![]()

Whole life insurance

Contestability refers to the period when an insurance company can contest or investigate a claim made on a life insurance policy. This is usually a two-year period following the date the policy is issued. During this time, the insurance company can also contest the issuance of the policy if there was a misrepresentation on the application for life insurance coverage.

Banker's Life Insurance: Is It Still Around?

You may want to see also

Explore related products

![]()

Final expense insurance

Contestability refers to the period when an insurance company can contest or investigate a claim made on a life insurance policy. This is usually a two-year period following the date the policy is issued. During this time, the insurance company can also investigate the issuance of the policy due to misrepresentation on the application for life insurance coverage. Most life insurance policies have a contestability period, and some have no time limit to submit a claim for a death benefit.

Globe Life Insurance offers whole life insurance, which is a type of permanent policy designed to cover your entire life as long as you pay the premiums. You cannot purchase this policy online; you must work with an agent or purchase coverage by mail.

Globe Life also offers final expense insurance, which is a burial insurance policy designed to cover end-of-life costs. This can be a good option for those who want to ensure their funeral expenses are covered, as well as other end-of-life costs.

While Globe Life offers some life insurance products that do not require a medical exam, this does not automatically equal a guaranteed issue policy. If you have chronic or severe health issues, you may still be declined for many of Globe Life's coverage options. It is important to carefully review the terms and conditions of any life insurance policy before purchasing it to ensure it meets your needs and expectations.

Supplementary Annuity and Life Insurance: Understanding the Basics

You may want to see also

Explore related products

![]()

Customer satisfaction

Contestability refers to the period when an insurance company can contest or investigate any claim made, or the issuance of a policy due to misrepresentation on the application for life insurance coverage. This is a standard practice for most insurance companies, and the contestability period is usually two years from the date the policy is issued.

Globe Life Insurance offers whole life insurance, which is a type of permanent policy designed to cover your entire life as long as you pay the premiums. You cannot purchase this policy online and must work with an agent or purchase coverage by mail. Globe Life has also been known to offer final expense insurance, which is a burial insurance policy designed to cover end-of-life costs.

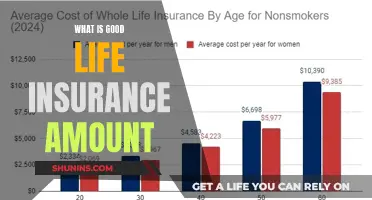

In terms of customer satisfaction, Globe Life has received mixed reviews. According to a NerdWallet analysis of data from the National Association of Insurance Commissioners, the company has drawn more complaints than expected for its size over a three-year period. In the J.D. Power's 2024 U.S. Individual Life Insurance Study, Globe Life ranked 16th out of 21 companies for customer satisfaction. However, AM Best gives Globe Life an A (Excellent) financial strength rating.

One advantage of Globe Life Insurance is that some of its life insurance products do not require a medical exam, making it a convenient option for many consumers. However, it is important to note that no medical exam does not guarantee a policy, and individuals with chronic or severe health issues may still be declined for coverage. Overall, Globe Life Insurance offers a range of coverage options, but customers should carefully review the company's offerings to ensure they meet their specific needs and expectations.

Universal Life Insurance: Interest-Earning Policies Explained

You may want to see also

Explore related products

![]()

Medical exam requirements

Contestability refers to the period when the insurance company can contest or investigate any claim made, or the issuance of the policy due to misrepresentation on the application for life insurance coverage. For most insurance companies, the contestability period is the two-year period following the date the policy is issued.

Globe Life offers a handful of life insurance products that do not require a medical exam, making it a convenient option for many consumers. However, it is important to note that no medical exam does not automatically equal a guaranteed issue policy. If you deal with chronic or severe health issues, you may still be declined for many of Globe Life's coverage options.

The medical exam requirements for Globe Life Insurance vary depending on the type of policy and the individual's health history. For some policies, a medical exam may not be required at all, while for others, a basic health screening may be sufficient. However, for more comprehensive coverage options, a full medical exam may be necessary.

The medical exam typically includes a review of the individual's medical history, as well as a physical examination. The physical examination may include measurements of height, weight, blood pressure, and other vital signs. Additionally, blood and urine samples may be collected for laboratory testing. The insurance company may also request access to the individual's medical records to verify the information provided during the exam.

It is important to note that the medical exam requirements may vary depending on the individual's age, health status, and the amount of coverage being sought. In some cases, the insurance company may require additional testing or evaluations to ensure that the individual meets the underwriting guidelines for the specific policy.

Life Insurance Agent: Is It a Tough Job?

You may want to see also

Frequently asked questions

The contestability period is the two-year period following the date the policy is issued, during which the insurance company can contest or investigate any claim made.

The contestability period is in place so that the insurance company can investigate any claim made, or the issuance of the policy, due to misrepresentation on the application for life insurance coverage.

If the insured person dies during the contestability period, the insurance company is given a period of time to contest the policy.

No, you cannot purchase Globe Life whole life insurance online. You will have to work with an agent or purchase coverage by mail.