Healthcare insurance is a critical financial tool designed to protect individuals and families from the high costs of medical care. It operates on the principle of risk pooling, where policyholders pay regular premiums to an insurance company, which in turn covers all or part of their medical expenses when needed. This coverage typically includes doctor visits, hospital stays, prescription medications, and preventive services, though the extent of coverage varies depending on the policy. By providing financial security, healthcare insurance ensures that individuals can access necessary medical treatments without facing overwhelming out-of-pocket expenses, promoting both physical and financial well-being. It also plays a vital role in public health by encouraging preventive care and early intervention, which can reduce the overall burden of disease in society.

| Characteristics | Values |

|---|---|

| Definition | A contract between an individual and an insurance company to cover medical expenses in exchange for premiums. |

| Purpose | Provides financial protection against high medical costs, ensuring access to healthcare services. |

| Types | Private Health Insurance, Public Health Insurance (e.g., Medicare, Medicaid), Employer-Sponsored Insurance. |

| Coverage | Includes hospitalization, doctor visits, prescription drugs, preventive care, and sometimes dental/vision. |

| Premiums | Regular payments (monthly/annual) made by the policyholder to maintain coverage. |

| Deductibles | Amount paid out-of-pocket before insurance coverage kicks in. |

| Copayments/Coinsurance | Fixed fees (copay) or percentage (coinsurance) paid by the insured for services. |

| Out-of-Pocket Maximum | The maximum amount an insured pays annually before the insurer covers all costs. |

| Network | Group of healthcare providers (doctors, hospitals) contracted with the insurer for lower rates. |

| Pre-existing Conditions | Conditions present before coverage starts; covered under laws like the ACA in the U.S. |

| Mandates | Required by law in some countries (e.g., ACA in the U.S. mandates coverage). |

| Tax Benefits | Premiums may be tax-deductible or subsidized, depending on jurisdiction. |

| Global Trends | Increasing adoption of digital health, telemedicine, and value-based care models. |

| Challenges | Rising costs, access disparities, and administrative complexities. |

| Regulation | Governed by national/regional bodies (e.g., CMS in the U.S., NHS in the UK). |

Explore related products

What You'll Learn

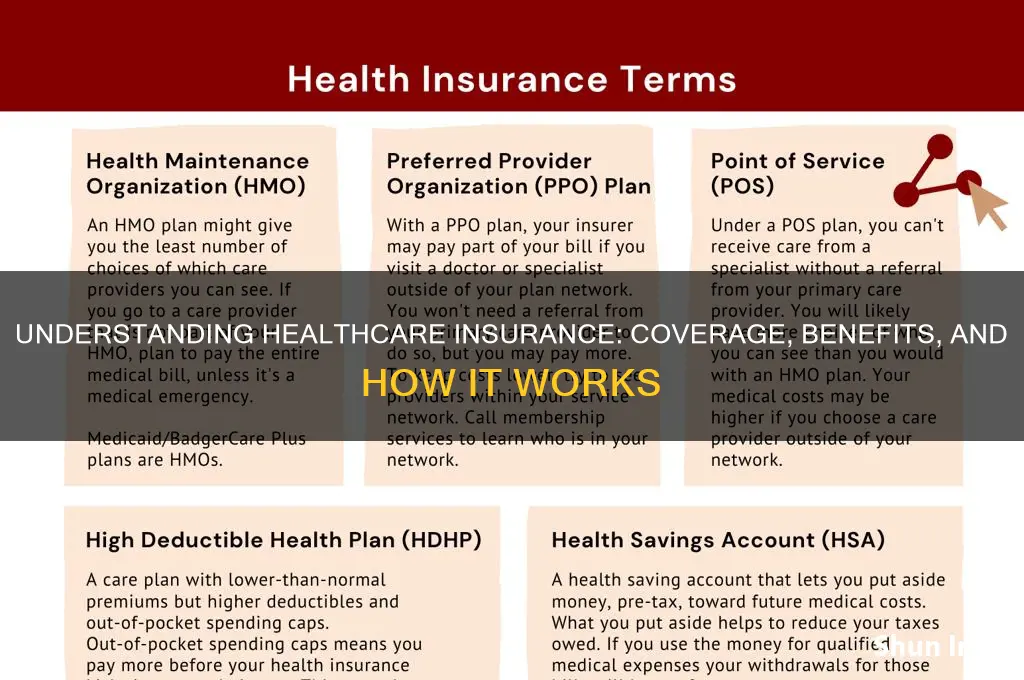

- Types of Plans: HMO, PPO, EPO, POS, and indemnity plans explained briefly

- Coverage Basics: In-network vs. out-of-network care, deductibles, copays, and coinsurance details

- Premiums & Costs: Monthly payments, out-of-pocket maximums, and cost-sharing responsibilities overview

- Essential Benefits: Coverage for hospitalization, prescriptions, preventive care, and mental health services

- Enrollment Periods: Open enrollment, special enrollment, and Medicaid/Medicare eligibility windows

![]()

Types of Plans: HMO, PPO, EPO, POS, and indemnity plans explained briefly

Healthcare insurance is a critical component of managing medical expenses, providing individuals and families with financial protection against the high costs of medical care. When exploring healthcare insurance, understanding the different types of plans is essential to making an informed decision. The most common types of health insurance plans include Health Maintenance Organizations (HMOs), Preferred Provider Organizations (PPOs), Exclusive Provider Organizations (EPOs), Point of Service (POS) plans, and indemnity plans. Each plan type offers distinct features, provider networks, and cost structures, catering to diverse healthcare needs and preferences.

HMO (Health Maintenance Organization) plans are known for their cost-effectiveness and emphasis on preventive care. In an HMO, members choose a primary care physician (PCP) who acts as a gatekeeper for all healthcare services. Referrals from the PCP are typically required to see specialists, and coverage is generally limited to in-network providers. HMOs often have lower premiums and out-of-pocket costs but offer less flexibility in choosing healthcare providers. This plan is ideal for individuals who prioritize affordability and are comfortable with a coordinated approach to care.

PPO (Preferred Provider Organization) plans offer greater flexibility in choosing healthcare providers. Members can visit any in-network or out-of-network provider, though staying within the network results in lower costs. Unlike HMOs, PPOs do not require a referral to see a specialist. While premiums and out-of-pocket expenses are typically higher than HMOs, PPOs provide more freedom in accessing care. This plan suits those who prefer a broader choice of providers and are willing to pay more for that flexibility.

EPO (Exclusive Provider Organization) plans combine elements of HMOs and PPOs. Like HMOs, EPOs generally restrict coverage to in-network providers, but they do not require a referral to see a specialist. EPOs often have lower premiums than PPOs but lack the out-of-network coverage option. This plan is a good fit for individuals who want a balance between cost and flexibility within a specific network of providers.

POS (Point of Service) plans offer a hybrid approach, blending features of HMOs and PPOs. Members select a primary care physician and can receive care within or outside the network, though out-of-network services typically come with higher costs. Referrals may be required for specialist visits, depending on the plan. POS plans provide a middle ground for those who want a PCP to coordinate care but also desire some out-of-network coverage.

Indemnity plans, also known as fee-for-service plans, offer the most flexibility in choosing healthcare providers. Members can visit any doctor or hospital without restrictions, and the insurance company reimburses a portion of the costs after the service is provided. While indemnity plans provide maximum freedom, they often come with higher premiums, deductibles, and out-of-pocket expenses. This plan is best suited for individuals who prioritize unrestricted access to providers and are willing to manage higher costs.

In summary, the choice of healthcare insurance plan depends on individual needs, budget, and preferences. HMOs and EPOs offer cost savings with network restrictions, PPOs provide flexibility at a higher cost, POS plans strike a balance between coordination and choice, and indemnity plans offer unparalleled freedom but with increased financial responsibility. Understanding these differences ensures that individuals can select a plan that aligns with their healthcare priorities.

Zander Life Insurance: Affordable Coverage, How?

You may want to see also

Explore related products

![]()

Coverage Basics: In-network vs. out-of-network care, deductibles, copays, and coinsurance details

Healthcare insurance is a critical tool that helps individuals manage the costs of medical care. At its core, it provides financial protection against high medical expenses by covering a portion or all of the costs associated with healthcare services. Understanding the basics of healthcare insurance coverage is essential to maximizing its benefits. One of the fundamental aspects to grasp is the difference between in-network and out-of-network care. Insurance plans typically have a network of healthcare providers—doctors, hospitals, and specialists—with whom they have negotiated lower rates. When you receive care from an in-network provider, the insurance company covers a larger portion of the cost, reducing your out-of-pocket expenses. Conversely, out-of-network care often results in higher costs because these providers have not agreed to the insurer’s negotiated rates, leaving you responsible for a larger share of the bill.

Another key component of healthcare insurance is the deductible, which is the amount you must pay out of pocket before your insurance coverage kicks in. For example, if your plan has a $1,000 deductible, you are responsible for the first $1,000 of covered medical expenses in a given year. Once you meet the deductible, the insurance company begins to pay its portion of the costs. It’s important to note that not all services require meeting the deductible; some preventive care services, like vaccinations or annual check-ups, may be covered in full without needing to meet the deductible first.

After meeting your deductible, you’ll typically encounter copays and coinsurance, which are additional out-of-pocket costs. A copay is a fixed amount you pay for a specific service, such as $20 for a doctor’s visit or $50 for a specialist appointment. Copays are straightforward and predictable, making it easier to budget for routine care. Coinsurance, on the other hand, is a percentage of the cost of a service that you are responsible for after meeting your deductible. For instance, if your plan has 20% coinsurance for hospital stays, you would pay 20% of the total cost, while the insurance company covers the remaining 80%. Coinsurance can vary depending on the type of service and whether the provider is in-network or out-of-network.

Understanding the interplay between deductibles, copays, and coinsurance is crucial for estimating your potential healthcare costs. For example, if you have a high deductible, you may pay more upfront before insurance coverage begins, but your monthly premiums might be lower. Conversely, a plan with a low deductible may have higher premiums but lower out-of-pocket costs when you need care. Additionally, some plans have out-of-pocket maximums, which cap the total amount you’ll pay for covered services in a year, providing a financial safety net.

Lastly, it’s important to review your insurance plan’s details carefully to understand what services are covered and under what conditions. Some plans may exclude certain treatments or require prior authorization for specific procedures. Knowing these details can help you avoid unexpected costs and make informed decisions about your healthcare. By familiarizing yourself with in-network vs. out-of-network care, deductibles, copays, and coinsurance, you can navigate your healthcare insurance more effectively and ensure you’re getting the most value from your plan.

Selling Life Insurance: A Tough Task to Persuade Customers

You may want to see also

Explore related products

![The Medicare Bible for Beginners: [3 in 1] Unlock Medical Benefits and Quality Healthcare | Super Easy Insider Strategies to Navigate Medicare While Avoiding Costly Mistakes](https://m.media-amazon.com/images/I/71tm-tSiWnL._AC_UY218_.jpg)

![]()

Premiums & Costs: Monthly payments, out-of-pocket maximums, and cost-sharing responsibilities overview

Healthcare insurance is a critical tool for managing medical expenses, providing financial protection against high healthcare costs. At the heart of understanding healthcare insurance are the concepts of premiums and costs, which determine how much you pay for coverage and how much you’re responsible for when receiving care. Let’s break down the key components: monthly payments, out-of-pocket maximums, and cost-sharing responsibilities.

Monthly premiums are the recurring payments you make to maintain your health insurance coverage, regardless of whether you use medical services. These payments are typically due every month and are a fixed cost agreed upon when you enroll in a plan. Premiums vary widely based on factors such as the type of plan (e.g., HMO, PPO), the level of coverage (e.g., bronze, silver, gold), your age, location, and whether you qualify for subsidies. Higher premiums often correspond to lower out-of-pocket costs when you need care, while lower premiums usually mean higher costs when you access services. It’s essential to balance your budget with your expected healthcare needs when choosing a plan.

In addition to premiums, out-of-pocket maximums are a critical aspect of healthcare insurance. This is the most you’ll have to pay for covered services in a policy period (usually a year) before your insurance covers 100% of the costs. Out-of-pocket maximums include expenses like deductibles, copayments, and coinsurance, but typically exclude premiums. For example, if your plan has a $5,000 out-of-pocket maximum, once you’ve spent that amount on covered services, your insurance will cover all additional costs for the rest of the year. This cap provides financial protection against catastrophic medical expenses.

Cost-sharing responsibilities refer to the portion of healthcare expenses you’re required to pay when you receive medical services. These include deductibles, copayments, and coinsurance. A deductible is the amount you must pay out of pocket before your insurance begins covering costs. For instance, if your plan has a $1,000 deductible, you’ll pay the first $1,000 of covered services before insurance kicks in. Copayments are fixed amounts you pay for specific services, such as $20 for a doctor’s visit, while coinsurance is a percentage of the cost you pay after meeting your deductible, such as 20% of the cost of a hospital stay. Understanding these cost-sharing elements helps you predict your potential expenses when using healthcare services.

It’s important to note that not all services are subject to cost-sharing. Many plans cover preventive care, such as vaccinations and screenings, at no cost to you, even before you meet your deductible. Additionally, some plans may have separate out-of-pocket maximums for in-network and out-of-network care, with out-of-network costs often being significantly higher. When selecting a plan, consider your health needs, budget, and how often you anticipate using medical services to ensure the premiums and cost-sharing structure align with your financial situation.

In summary, premiums, out-of-pocket maximums, and cost-sharing responsibilities are foundational elements of healthcare insurance. Premiums are your monthly payments to maintain coverage, out-of-pocket maximums cap your annual expenses, and cost-sharing mechanisms like deductibles, copayments, and coinsurance determine how much you pay when you receive care. By understanding these components, you can make informed decisions about which insurance plan best meets your needs and provides the financial protection you require.

Life Insurance for Non-Profits: Funding Peace of Mind

You may want to see also

Explore related products

$14.97 $22.79

![]()

Essential Benefits: Coverage for hospitalization, prescriptions, preventive care, and mental health services

Healthcare insurance is a critical tool designed to protect individuals and families from the financial burden of medical expenses. At its core, it provides coverage for a range of essential health services, ensuring that policyholders can access necessary care without facing overwhelming costs. Among the most vital components of healthcare insurance are essential benefits, which include coverage for hospitalization, prescriptions, preventive care, and mental health services. These benefits are foundational to maintaining overall health and well-being, addressing both immediate and long-term medical needs.

Coverage for hospitalization is one of the cornerstone benefits of healthcare insurance. Hospital stays can be exorbitantly expensive, often involving costs for room and board, surgeries, diagnostic tests, and specialized care. Insurance plans that include hospitalization coverage ensure that individuals are protected from these high expenses, allowing them to focus on recovery rather than financial strain. This coverage typically extends to emergency room visits, intensive care, and surgical procedures, providing a safety net for unexpected or critical health situations.

Another essential benefit is prescription drug coverage, which helps offset the cost of medications prescribed by healthcare providers. Prescription drugs are often necessary for managing chronic conditions, treating acute illnesses, or preventing disease progression. Without insurance, the cost of these medications can be prohibitive, leading individuals to skip doses or forgo treatment altogether. Comprehensive insurance plans cover a wide range of prescription drugs, ensuring that policyholders can adhere to their treatment plans and maintain their health.

Preventive care is a proactive aspect of healthcare insurance that focuses on maintaining health and preventing illness before it occurs. This includes services such as vaccinations, screenings, check-ups, and counseling to promote healthy behaviors. By covering preventive care, insurance plans encourage early detection of health issues, which can lead to more effective and less costly treatments. For example, regular screenings for conditions like cancer or diabetes can identify problems in their early stages, significantly improving outcomes and reducing long-term healthcare costs.

Mental health services are equally essential, as they address the psychological and emotional well-being of individuals. Mental health coverage includes therapy sessions, counseling, and treatment for conditions such as depression, anxiety, and substance use disorders. Access to mental health services is crucial, as untreated mental health issues can negatively impact physical health, relationships, and overall quality of life. Insurance plans that include mental health coverage ensure that individuals can seek the support they need without financial barriers, fostering a holistic approach to healthcare.

In summary, the essential benefits of healthcare insurance—coverage for hospitalization, prescriptions, preventive care, and mental health services—form the backbone of a robust and comprehensive health plan. These benefits are designed to address a wide spectrum of health needs, from emergency care to long-term wellness. By providing financial protection and access to necessary services, healthcare insurance empowers individuals to take control of their health, ensuring that they can lead healthier, more secure lives. Understanding these essential benefits is key to selecting a plan that meets one’s unique health and financial needs.

Safety Deposit Boxes: Are They Insured?

You may want to see also

Explore related products

![[8 Pack 4" x 5 Yards] Beige-Self Adhesive Cohesive Bandage Wrap, Self Adherant Non-Woven Wrap Rolls, Atheletic Tape for Wrist, Ankle, Hand, Leg, Premium-Grade Medical Stretch Wrap](https://m.media-amazon.com/images/I/81wGnSXRl8L._AC_UL320_.jpg)

![]()

Enrollment Periods: Open enrollment, special enrollment, and Medicaid/Medicare eligibility windows

Healthcare insurance is a critical component of managing health-related expenses, providing coverage for medical services, treatments, and preventive care. Understanding the enrollment periods is essential for securing the right plan at the right time. Enrollment periods are specific windows during which individuals can sign up for, change, or renew their health insurance plans. These periods are categorized into open enrollment, special enrollment, and Medicaid/Medicare eligibility windows, each serving distinct purposes and adhering to specific rules.

Open Enrollment Period is the annual window during which individuals can enroll in or change their health insurance plans without needing a qualifying event. This period typically lasts for a few months, often between November and December, with coverage beginning the following year. For example, in the United States, the Health Insurance Marketplace open enrollment period usually runs from November 1 to December 15. During this time, individuals can compare plans, assess their healthcare needs, and select a policy that best fits their budget and medical requirements. Missing the open enrollment deadline generally means having to wait until the next year to enroll, unless a special enrollment period applies.

Special Enrollment Period (SEP) allows individuals to enroll in or change health insurance plans outside of the open enrollment period if they experience certain qualifying life events. These events include losing health coverage, getting married or divorced, having a baby or adopting a child, moving to a new area, or experiencing changes in income that affect eligibility for subsidies. For instance, if someone loses their job-based insurance, they typically have 60 days to enroll in a new plan through a special enrollment period. It’s crucial to provide documentation of the qualifying event when applying during an SEP. This period ensures that individuals are not left without coverage during significant life transitions.

Medicaid and Medicare Eligibility Windows operate differently from private insurance enrollment periods. Medicaid, a state and federal program for low-income individuals and families, allows year-round enrollment for those who qualify. There is no specific open enrollment period; eligible individuals can apply at any time through their state’s Medicaid agency or the Health Insurance Marketplace. Medicare, a federal program for individuals aged 65 and older and certain younger people with disabilities, has specific enrollment periods. The Initial Enrollment Period occurs around an individual’s 65th birthday, lasting for seven months (three months before, the birthday month, and three months after). The Annual Enrollment Period (October 15 to December 7) allows beneficiaries to switch Medicare Advantage or Part D prescription drug plans. Additionally, the Medicare Advantage Open Enrollment Period (January 1 to March 31) permits changes to Medicare Advantage plans. Understanding these windows is vital to avoid penalties or gaps in coverage.

Navigating enrollment periods requires careful planning and awareness of deadlines. For private insurance, open enrollment is the primary opportunity to secure coverage, while special enrollment periods provide flexibility during life changes. Medicaid offers continuous enrollment for eligible individuals, and Medicare has specific windows tailored to different needs. By staying informed about these periods, individuals can ensure they have the necessary coverage when they need it most. Always verify dates and requirements through official sources, such as healthcare.gov or state Medicaid agencies, to make informed decisions.

Life Insurance and Taxes: Which Form to File?

You may want to see also

Frequently asked questions

Healthcare insurance is a contract between an individual and an insurance company that helps cover medical expenses in exchange for regular premium payments. It provides financial protection against high healthcare costs, including doctor visits, hospital stays, prescription medications, and preventive care.

Healthcare insurance is important because it protects individuals and families from unexpected and often high medical costs. It ensures access to necessary healthcare services, promotes preventive care, and reduces the financial burden of illnesses or injuries, helping to avoid debt or bankruptcy.

Common types of healthcare insurance plans include Health Maintenance Organizations (HMOs), Preferred Provider Organizations (PPOs), Exclusive Provider Organizations (EPOs), and Point of Service (POS) plans. Additionally, there are high-deductible health plans (HDHPs) paired with Health Savings Accounts (HSAs), as well as government-sponsored plans like Medicare and Medicaid.