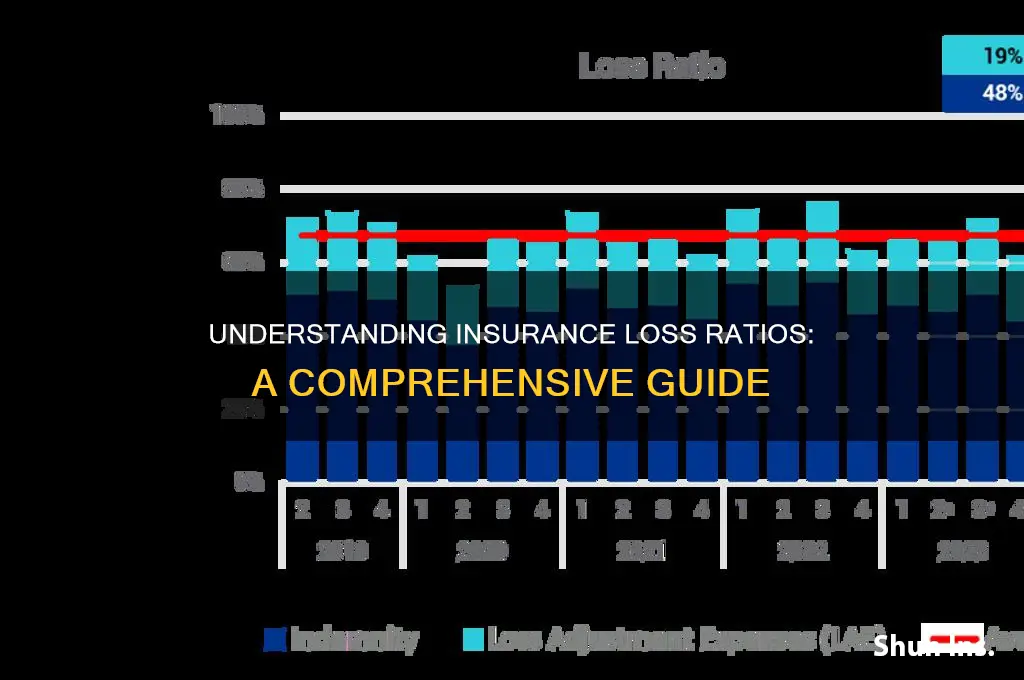

The loss ratio is a metric used to evaluate the financial health and profitability of an insurance company. It is calculated by dividing the total losses incurred (paid and reserved) in claims plus adjustment expenses by the total premiums earned from policyholders. The loss ratio provides a high-level overview of an insurance company's financial performance by comparing the costs paid for claims versus the premiums received. A high loss ratio may indicate financial distress, especially for property or casualty insurance companies. Conversely, a lower ratio indicates higher profitability. Loss ratios vary depending on the type of insurance, with health insurance typically having higher loss ratios than property and casualty insurance.

| Characteristics | Values |

|---|---|

| Definition | A loss ratio is a ratio of losses to gains, used primarily in the insurance industry. |

| Formula | Loss ratio = ((insurance claims paid + loss adjustment expenses)/Total premiums earned) x 100 |

| Purpose | To provide insurance companies with a high-level overview of their financial performance. |

| Interpretation | A low loss ratio indicates high profitability. A high loss ratio may indicate financial distress. |

| Combined ratio | The loss ratio is often combined with the expense ratio to provide a more holistic view of an insurance company's performance. |

| Medical Loss Ratio (MLR) | Health insurance companies must spend at least 80% (85% in the large group market) of premiums on medical care and quality improvement, otherwise they must issue refunds. |

| Auto insurance | Loss ratios improved in 2023 and the first half of 2024, recovering from a $21 billion net operating loss in 2022. |

Explore related products

What You'll Learn

![]()

Loss ratio formula

The loss ratio formula is used in the insurance industry to represent the relationship between total premiums earned and actual losses incurred over a given period. It is a quick way to evaluate the financial health and profitability of an insurance company. The formula is calculated as follows:

Loss ratio = ((insurance claims paid + loss adjustment expenses)/premium earned) x 100

For example, if an insurance company earned $100 million in premiums from clients in 2020, and paid out a total of $60 million in claims and an additional $5 million in adjusting claims, the loss ratio would be calculated as ($60,000,000 + $5,000,000) / ($100,000,000) x 100 = 65%. This means the insurance company used 65% of its premiums to pay for claims.

The loss ratio is a useful metric for insurance companies to assess their profitability. A lower ratio indicates higher profitability. However, other expenses such as agent's sales commissions, salaries, marketing expenses, and general expenses should also be considered, as they are not reflected in the loss ratio but are included in the expense ratio.

Loss ratios vary depending on the type of insurance. For example, health insurance tends to have a higher loss ratio compared to property and casualty insurance.

Term Life Insurance: Modified for Your Needs

You may want to see also

Explore related products

![]()

Loss ratio and financial health

Loss ratios are used to evaluate the financial health and profitability of an insurance company. They are calculated by adding up the losses incurred in claims and adjustment expenses and then dividing that sum by the total earned premiums. The formula is as follows:

> ((insurance claims paid + loss adjustment expenses)/premium earned) x 100

The higher the loss ratio, the less profitable the company, and vice versa. A loss ratio above 100% indicates that the insurance company is unprofitable and may be in poor financial health because it is paying out more in claims than it is receiving in premiums. For example, if an insurance company pays out $5 million in claims and receives $3 million in premiums, the loss ratio is 167%, indicating that the company is in poor financial health.

Loss ratios vary depending on the type of insurance. For instance, the loss ratio for health insurance tends to be higher than that for property and casualty insurance. As of 2007, the average US medical loss ratio for private insurers was 81% (a profit of 19%). In contrast, loss ratios for property and casualty insurance typically range from 70% to 99%.

Insurance companies use loss ratios to make management decisions, such as setting target premiums or determining if a rate change is necessary. They also help insurers assess the risk profiles of their clients. If an insurer underestimates the risk profile of a client, the loss ratio will likely be higher. For example, in auto insurance, insurance companies consider factors such as the client's driving record, the type of car, age, and gender to determine the premium. If the insurance company underestimates the client's risk, they may offer a lower premium than what the client's actual risk profile warrants.

Life Insurance: Annual Increases and What They Mean for You

You may want to see also

Explore related products

![]()

Loss ratio and insurance premiums

Loss ratio is a metric used to evaluate the financial health and profitability of an insurance company. It is calculated by dividing the total losses incurred (paid and reserved) in claims and adjustment expenses by the total premiums earned from policyholders. The loss ratio is expressed as a percentage and represents the portion of premium income paid out to cover claims. For example, if an insurance company pays out $60 in claims for every $100 collected in premiums, its loss ratio is 60%.

The loss ratio is an important indicator of an insurance company's performance and financial stability. A lower loss ratio indicates higher profitability for the insurance company, while a higher loss ratio may suggest financial distress, especially for property or casualty insurance companies. When the loss ratio exceeds 100%, it means the insurer is paying out more in claims than they are receiving in premiums, indicating potential financial instability.

Insurance companies use the loss ratio to make management decisions, such as setting target premiums, determining rate changes, and comparing the profitability of different product lines. Carriers may also review the loss ratio history when assessing the risk associated with a policyholder and deciding on premium increases or policy renewals.

The loss ratio is often used in conjunction with the expense ratio, which considers expenses such as underwriting, sales commissions, salaries, and marketing expenses. The combination of the loss ratio and expense ratio is known as the combined ratio, providing a more comprehensive view of an insurance company's financial health by accounting for both losses and expenses relative to earned premiums.

Regulators and external parties also utilise the loss ratio to monitor and assess the performance of insurance companies, ensuring they maintain adequate loss ratios to prevent excessive profits or financial instability.

How to Get Life Insurance for Your Husband

You may want to see also

Explore related products

![]()

Medical cost ratio

The medical cost ratio (MCR), also known as the medical loss ratio or medical benefit ratio, is a type of loss ratio that is used in managed health care and health insurance. It measures medical costs as a percentage of premium revenues.

The MCR is calculated by dividing the premiums allocated for fully insured or self-funded healthcare coverage by the total expenses for inpatient, professional (including physicians and other licensed providers), outpatient, and pharmacy services. The formula for MCR can be simplified as costs/premiums. A lower MCR is desirable, with a ratio of 85% or less being considered good.

In the context of health insurance, the MCR is an important metric for assessing the financial health and profitability of the insurance company. Under the Affordable Care Act (ACA), health insurance providers are mandated to allocate a significant portion of premiums to clinical services and improving healthcare quality. Specifically, insurers must divert 80% of premiums to claims and activities that enhance the quality of care, with the remaining 20% being used for expenses and profit. If an insurer fails to meet this 80/20 threshold, they are required to issue a rebate to their policyholders.

For example, consider a health insurance carrier that collects $10 in premiums and pays out $8 in claims. This insurer has an MCR of 80%, which is within the desired range. However, if the insurer paid out $9 in claims, their MCR would increase to 90%, indicating a less profitable position.

The MCR is a valuable tool for assessing the financial stability and performance of health insurance companies, helping to ensure that insurers are providing value to their customers and that premiums are being used efficiently to cover claims and improve healthcare services.

Life Insurance: A Safety Net for Disability Income Loss

You may want to see also

Explore related products

![]()

Loss ratio and combined ratio

The loss ratio is a financial indicator used in the insurance industry to evaluate the financial health and profitability of an insurance company. It compares the amount paid out in claims to the premiums earned from policyholders. The loss ratio formula is calculated by adding up insurance claims paid and adjustment expenses, then dividing that sum by the total earned premiums. For example, if a company pays out $8 million in claims for every $16 million in collected premiums, the loss ratio would be 50%. A high loss ratio can be an indicator of financial distress, especially for a property or casualty insurance company.

The combined ratio, on the other hand, is a broader measure that includes both the loss ratio and the expense ratio. It accounts for underwriting and administrative expenses, providing a more holistic view of an insurance company's performance. The combined ratio is calculated by adding up the incurred losses and expenses and then dividing that sum by the total earned premiums. For example, if an insurance company pays out $7 million in claims and has $5 million in expenses, with a total revenue of $60 million in collected premiums, the combined ratio is 20%, indicating profitability and financial health.

The combined ratio is specifically useful for property and casualty insurance companies as it measures the money flowing out of the company in dividends, expenses, and losses. A combined ratio below 100% indicates underwriting profit, while a ratio above 100% means the company is paying out more in claims than it is receiving from premiums. Even with a combined ratio above 100%, a company can still be profitable if its operating costs are managed well.

Both the loss ratio and the combined ratio are used by insurance companies and external stakeholders to assess the financial health and profitability of the insurance business. While the loss ratio focuses solely on incurred claims compared to earned premiums, the combined ratio provides a broader picture by including both claims and operating expenses. This means that a company with a low loss ratio could still be unprofitable if its operating costs are too high, which would be revealed by the combined ratio.

In summary, the loss ratio and combined ratio are financial metrics used in the insurance industry to assess the financial health and profitability of insurance companies. The loss ratio focuses on incurred losses and premiums, while the combined ratio adds expenses and provides a more comprehensive view of a company's performance and profitability. These ratios are essential tools for insurance companies, investors, and regulators to make informed decisions and assess the stability and success of the insurance business.

Universal Employee Life Insurance: What's Covered and Why It Matters

You may want to see also

Frequently asked questions

A loss ratio in insurance is a ratio of losses to gains, used to evaluate the financial health and profitability of an insurance company. It is calculated by taking the sum of insurance claims paid and loss adjustment expenses and dividing it by the total earned premiums.

The loss ratio provides insurance companies with a high-level overview of their financial performance. It is used by insurers and external parties, such as regulators, lenders and consumer advocates, to monitor and assess performance. A high loss ratio can indicate financial distress, especially for property or casualty insurance companies.

A high loss ratio may result in an insurance provider raising premiums or choosing not to renew a policy. Conversely, if the loss ratio is low, it indicates higher profitability for the insurance company.