Underwriting in insurance refers to the process by which insurers evaluate and assume the risk of insuring a person or property. It involves assessing the potential risks associated with a policyholder, determining the appropriate premium to charge, and deciding whether to accept, modify, or reject the application for coverage. Underwriters rely on various factors, such as the applicant's health, age, occupation, and claims history, as well as the value and condition of the property being insured. The goal of underwriting is to ensure that the insurer can cover potential claims while maintaining profitability, ultimately balancing risk exposure with the financial stability of the insurance company.

Explore related products

What You'll Learn

- Risk Assessment Process: Evaluating risks to determine policy terms and premiums for applicants

- Underwriting Guidelines: Standard criteria insurers use to accept or reject insurance applications

- Types of Underwriting: Manual, automated, or hybrid methods for policy evaluation

- Underwriting Profitability: Balancing premiums with claims to ensure insurer profitability

- Role of Underwriters: Professionals who assess risks and set policy conditions

![]()

Risk Assessment Process: Evaluating risks to determine policy terms and premiums for applicants

Underwriting in insurance is the process by which insurers evaluate the risks associated with insuring a particular individual or entity and determine the terms and premiums of the policy. Central to this process is risk assessment, a systematic and detailed evaluation of potential risks to ensure that the policy is both fair to the applicant and financially viable for the insurer. This involves analyzing various factors to predict the likelihood of claims and the potential cost of those claims.

The risk assessment process begins with data collection, where underwriters gather information about the applicant. This includes personal or business details, medical history (for life or health insurance), property details (for home or auto insurance), financial stability, and claims history. For instance, in life insurance, underwriters may request medical exams or records to assess health risks. In property insurance, they might evaluate the location, construction materials, and safety features of a building. The accuracy and completeness of this data are crucial for a fair assessment.

Once the data is collected, underwriters proceed to risk analysis, where they evaluate the likelihood and severity of potential losses. This step involves applying actuarial models, statistical tools, and industry benchmarks to quantify risk. For example, a young, healthy individual with no family history of chronic illnesses may be classified as low risk for life insurance, while a business located in a flood-prone area would be considered high risk for property insurance. Underwriters also consider external factors such as economic trends, crime rates, and environmental risks that could impact the applicant's risk profile.

Based on the risk analysis, underwriters determine policy terms and premiums. Low-risk applicants typically receive more favorable terms, such as lower premiums or broader coverage, while high-risk applicants may face higher premiums, exclusions, or even denial of coverage. Underwriters may also recommend risk mitigation measures, such as installing security systems for property insurance or quitting smoking for life insurance, to improve the applicant's risk profile. The goal is to balance the insurer's exposure to risk with the applicant's need for coverage.

Finally, the risk assessment process includes decision-making and documentation, where underwriters finalize the policy terms and premiums. This decision is communicated to the applicant, often through an insurance agent or broker. Underwriters must document their reasoning and decisions clearly to ensure transparency and compliance with regulatory standards. This documentation is also essential for future reference, especially if claims are filed or disputes arise. Through this structured and meticulous process, underwriting ensures that insurance policies are priced appropriately and risks are managed effectively.

Life Insurance Income: Financial Security for Your Family

You may want to see also

Explore related products

![]()

Underwriting Guidelines: Standard criteria insurers use to accept or reject insurance applications

Underwriting in insurance is the process through which insurers evaluate the risks associated with insuring a person or property and decide whether to accept the application, reject it, or modify the terms of coverage. This critical function ensures that the insurer maintains a balanced portfolio of risks while offering fair premiums to policyholders. Underwriting guidelines are the standardized criteria insurers use to make these decisions, providing a framework for consistency and fairness in the evaluation process. These guidelines are rooted in actuarial data, industry standards, and the insurer’s risk appetite, ensuring that only acceptable risks are underwritten.

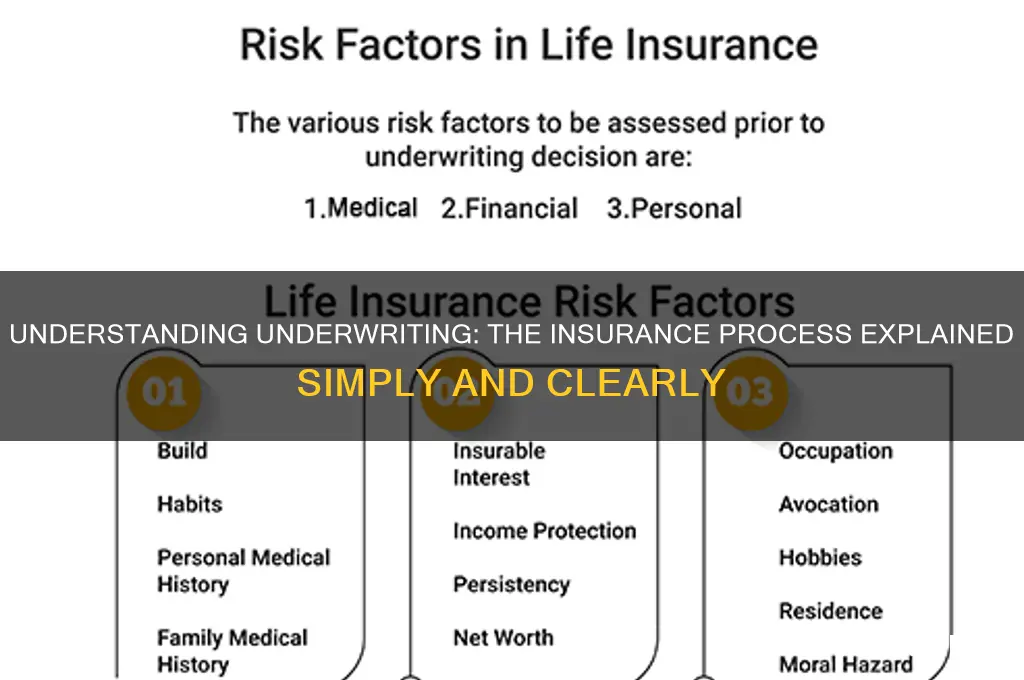

The first standard criterion in underwriting guidelines is the applicant’s risk profile. Insurers assess factors such as age, health, occupation, lifestyle, and medical history for life or health insurance. For property insurance, the focus shifts to the condition of the property, its location, and potential hazards like natural disasters or crime rates. High-risk profiles, such as individuals with pre-existing medical conditions or properties in flood-prone areas, may face higher premiums, exclusions, or rejection. Underwriters use this information to determine the likelihood of claims and price the policy accordingly.

Another key criterion is the accuracy and completeness of the application. Insurers rely on the information provided by the applicant to assess risk. Misrepresentation or omission of critical details can lead to rejection or policy cancellation. Underwriters verify the data through third-party sources, such as medical records, credit reports, or property inspections, to ensure transparency and accuracy. Applications that fail to meet these verification standards are often declined to mitigate potential fraud or adverse selection.

Policy limits and coverage scope also play a significant role in underwriting decisions. Insurers evaluate whether the requested coverage aligns with the applicant’s needs and risk level. For instance, a high-value property may require specialized coverage that exceeds standard limits, prompting underwriters to assess whether the insurer can bear the additional risk. Similarly, applicants seeking excessive coverage relative to their risk profile may face rejection or adjustments to the policy terms.

Finally, compliance with legal and regulatory requirements is a non-negotiable criterion in underwriting guidelines. Insurers must adhere to state and federal laws governing insurance practices, ensuring that policies are fair and non-discriminatory. Underwriters assess whether the application meets these standards, particularly in areas like health insurance, where pre-existing conditions cannot be grounds for rejection under certain regulations. Failure to comply with legal requirements can result in regulatory penalties and reputational damage for the insurer.

In summary, underwriting guidelines are the backbone of the insurance evaluation process, providing insurers with a structured approach to assess and manage risk. By focusing on the applicant’s risk profile, application accuracy, policy scope, and regulatory compliance, underwriters ensure that only acceptable risks are insured. These guidelines not only protect the insurer’s financial stability but also promote fairness and transparency in the insurance market.

Understanding Life Insurance Fees and Their Impact

You may want to see also

Explore related products

![]()

Types of Underwriting: Manual, automated, or hybrid methods for policy evaluation

Underwriting in insurance is the process of evaluating risks and determining whether to accept an application for coverage, as well as setting the terms and premiums for the policy. It involves assessing the potential risks associated with insuring a person or property and ensuring that the risk is acceptable to the insurer. The underwriting process is critical for insurers to maintain profitability and financial stability by avoiding excessive claims payouts. To achieve this, insurers employ different underwriting methods: manual, automated, or hybrid approaches, each with its own advantages and applications in policy evaluation.

Manual Underwriting is the traditional method where human underwriters review and assess applications for insurance coverage. This process involves a detailed examination of the applicant's information, such as medical history, financial records, and property details. Manual underwriters rely on their expertise, experience, and judgment to evaluate risks and make decisions. They may request additional documentation or clarification from the applicant to ensure a thorough assessment. This method is particularly useful for complex or high-risk cases that require a nuanced understanding of the applicant's circumstances. However, manual underwriting can be time-consuming and resource-intensive, making it less efficient for high-volume, straightforward applications.

Automated Underwriting, on the other hand, leverages technology and algorithms to evaluate insurance applications quickly and consistently. This method uses predefined rules and data analytics to assess risks based on the information provided by the applicant. Automated systems can process large volumes of applications in a short time, reducing turnaround times and operational costs for insurers. They are particularly effective for standard, low-risk policies where the criteria for acceptance are well-defined. However, automated underwriting may struggle with complex cases or applicants who fall outside standard risk profiles, as it lacks the flexibility and judgment of human underwriters.

Hybrid Underwriting combines elements of both manual and automated methods to leverage their respective strengths. In this approach, automated systems handle the initial evaluation of applications, flagging those that meet predefined criteria for acceptance or rejection. Cases that require further review are then passed on to human underwriters for a more detailed assessment. This method optimizes efficiency by automating routine tasks while ensuring that complex or borderline cases receive the attention they need. Hybrid underwriting is increasingly popular as it balances speed, accuracy, and the ability to handle a wide range of risk profiles.

The choice of underwriting method depends on factors such as the type of insurance, the complexity of the risk, and the insurer's operational capabilities. For instance, life insurance applications often involve detailed medical assessments, making manual or hybrid underwriting more suitable. In contrast, auto insurance policies, which are typically more standardized, may benefit from automated underwriting. Insurers must carefully consider their underwriting approach to ensure it aligns with their risk management goals and customer service expectations.

In conclusion, underwriting is a fundamental process in insurance that ensures risks are adequately assessed and priced. The methods of manual, automated, and hybrid underwriting each offer distinct advantages, catering to different needs and scenarios. As technology continues to evolve, the insurance industry is likely to see further innovations in underwriting practices, enhancing efficiency and accuracy while maintaining the critical human element in risk evaluation.

Vanguard's SIPC Insurance: What Investors Need to Know

You may want to see also

Explore related products

![]()

Underwriting Profitability: Balancing premiums with claims to ensure insurer profitability

Underwriting in insurance is the process by which insurers evaluate and assume the risk of insuring a person or property, determining the appropriate premium to charge based on the assessed risk. It involves a meticulous analysis of various factors, such as the applicant’s health, age, occupation, or the condition of a property, to predict the likelihood of future claims. Effective underwriting ensures that the insurer collects sufficient premiums to cover potential claims, operating expenses, and still generate a profit. This balance is critical for underwriting profitability, which hinges on accurately pricing policies to avoid underpricing risks that could lead to financial losses.

Achieving underwriting profitability requires insurers to strike a delicate balance between premiums collected and claims paid out. Premiums must be set high enough to cover expected claims, administrative costs, and a margin for profit, but not so high that they become uncompetitive in the market. Insurers use historical data, actuarial science, and predictive analytics to estimate future claims accurately. For instance, in health insurance, underwriters assess medical histories to gauge the likelihood of costly treatments, while in property insurance, they evaluate factors like location and construction quality to predict damage risks. This data-driven approach ensures premiums are fair and reflective of the risk assumed.

A key challenge in underwriting profitability is managing volatility in claims frequency and severity. Unexpected events, such as natural disasters or pandemics, can lead to a surge in claims, disrupting the premium-to-claims balance. To mitigate this, insurers often diversify their portfolio by insuring a mix of risks across different regions, industries, or demographics. Additionally, reinsurance—transferring a portion of the risk to another insurer—is a common strategy to protect against catastrophic losses. By spreading risk, insurers can maintain stability and ensure profitability even in adverse scenarios.

Technology plays a pivotal role in enhancing underwriting profitability. Advanced tools like artificial intelligence (AI) and machine learning (ML) enable insurers to analyze vast datasets, identify patterns, and refine risk assessments. For example, AI can process medical records to predict health risks more accurately or use satellite imagery to assess property risks. Automation also streamlines the underwriting process, reducing operational costs and allowing underwriters to focus on complex cases. These technological advancements improve pricing accuracy, reduce inefficiencies, and ultimately bolster profitability.

Finally, maintaining underwriting profitability requires continuous monitoring and adjustment of strategies. Insurers must stay abreast of changing market conditions, regulatory requirements, and emerging risks. Regular reviews of policy performance and claims trends help identify areas where premiums may need adjustment or where risk selection criteria should be tightened. Proactive risk management, coupled with a customer-centric approach to ensure competitive pricing, is essential for long-term profitability. By balancing precision in risk assessment with adaptability, insurers can achieve sustainable underwriting profitability while fulfilling their commitment to policyholders.

Ace Your Life Insurance Agent Interview: Tips for Success

You may want to see also

![]()

Role of Underwriters: Professionals who assess risks and set policy conditions

Underwriting in insurance is the process through which insurers evaluate and assume the risk of insuring a person or property. At the heart of this process are underwriters, professionals who play a critical role in assessing risks and setting policy conditions. Their primary responsibility is to determine whether to accept or reject an insurance application based on the level of risk involved. Underwriters meticulously analyze various factors, including the applicant’s health, occupation, lifestyle, and the nature of the property or asset being insured. This assessment ensures that the insurer can maintain a balanced portfolio of risks and remain financially stable.

The role of underwriters extends beyond mere risk assessment; they are also responsible for setting the terms and conditions of insurance policies. This includes determining the premium amount, coverage limits, and any exclusions or additional clauses that may apply. Underwriters use actuarial data, historical trends, and predictive models to price policies accurately. By doing so, they ensure that the premiums charged are sufficient to cover potential claims while remaining competitive in the market. Their decisions directly impact the insurer’s profitability and ability to meet its financial obligations.

Underwriters also act as gatekeepers for the insurance company, ensuring that only acceptable risks are insured. They may request additional information, such as medical exams or property inspections, to make informed decisions. In some cases, underwriters may offer coverage with specific conditions or exclusions to mitigate risks. For instance, a life insurance policy might exclude coverage for certain high-risk activities. This tailored approach allows insurers to provide coverage to a broader range of applicants while managing their exposure to potential losses.

Another key aspect of an underwriter’s role is to stay updated on industry trends, regulatory changes, and emerging risks. They must continuously refine their assessment methods to account for new factors, such as climate change or technological advancements, that could impact risk profiles. Underwriters also collaborate with other departments, such as sales and claims, to ensure that policies are aligned with the company’s overall strategy and customer needs. Their expertise is invaluable in maintaining the integrity and sustainability of the insurance business.

In summary, underwriters are indispensable professionals in the insurance industry, tasked with assessing risks and setting policy conditions. Their decisions influence the insurer’s financial health, the scope of coverage offered, and the premiums charged. By carefully evaluating risks and tailoring policies, underwriters enable insurers to provide protection to individuals and businesses while managing their own exposure. Their role requires a blend of analytical skills, industry knowledge, and strategic thinking, making them vital to the functioning of the insurance market.

Life Insurance: PCI's Employee Coverage Explained

You may want to see also

Frequently asked questions

Underwriting in insurance is the process of evaluating and assuming the risk of insuring a person or property. It involves assessing the risks associated with a potential policyholder and determining whether to accept the risk, set premiums, or exclude certain conditions.

Underwriting is typically performed by underwriters, who are professionals trained to analyze risks and make decisions based on actuarial data, medical reports, financial information, and other relevant factors.

Underwriters consider factors such as the applicant's age, health, occupation, lifestyle, medical history, and the type and value of the property or asset being insured. They also evaluate the likelihood and potential cost of claims.

Underwriting directly influences insurance premiums. Higher-risk applicants may face higher premiums or policy exclusions, while lower-risk applicants may qualify for lower premiums or additional benefits.

Yes, an insurance application can be denied if the underwriter determines that the risk is too high or uninsurable. Alternatively, the insurer may offer coverage with modified terms, such as higher premiums or specific exclusions.