Medicare is a health insurance program that covers a significant portion of the medical expenses of its enrollees, who are primarily senior citizens aged 65 and above. While Medicare premiums are typically not paid with pre-tax dollars, certain beneficiaries, such as the self-employed, may be eligible to deduct their Medicare premiums and medical expenses when filing their income tax returns. The eligibility for these deductions depends on factors such as income, age, and the availability of employer-sponsored health plans. This topic is covered under Topic No. 502, Medical and Dental Expenses, by the Internal Revenue Service.

| Characteristics | Values |

|---|---|

| Who can deduct Medicare premiums on their tax return? | Self-employed people who earn a profit from their self-employment |

| What can be deducted? | Medicare Part A (hospital) premiums, Medicare Part B (medical) premiums, Medicare Part C (Medicare Advantage/MA) premiums, Medicare Part D (prescription drug plan) premiums, Medicare Supplement Insurance (Medigap) premiums |

| How much does Medicare cost? | Costs vary based on coverage, services, and providers |

| Can I deduct my medical expenses? | Yes, if they exceed 7.5% of your adjusted gross income for the year |

Explore related products

$19.95 $14.95

What You'll Learn

- Self-employed individuals can deduct health insurance premiums from their income taxes

- Medical expenses exceeding 7.5% of adjusted gross income can be deductible

- Medicare Part A, B, C, and D premiums are deductible

- Medicare Advantage plans offer extra benefits beyond Original Medicare

- Self-employed individuals cannot deduct if eligible for an employer-sponsored health plan

![]()

Self-employed individuals can deduct health insurance premiums from their income taxes

Self-employed individuals can deduct health insurance premiums, including medical, dental, and qualifying long-term care insurance coverage for themselves, their spouse, and their dependents, from their income taxes. This write-off is entered on Part II of Schedule 1 as an adjustment to income and then transferred to page 1 of Form 1040. This means that the deduction is beneficial regardless of whether or not you itemize your deductions. This is because the deduction lowers your adjusted gross income (AGI), which can reduce the likelihood of being affected by unfavourable phase-out rules that may cut back or eliminate certain tax breaks.

It is important to note that you cannot claim the health insurance premium write-off for months when either you or your spouse were eligible to participate in an employer-subsidized health plan. Additionally, the health insurance premium deduction cannot exceed the earned income you collect from your business. For example, if your self-employment activity is a sole proprietorship that generated a tax loss for the year, you cannot claim the deduction as the business did not generate any positive earned income.

If you are a business partner or a member of an LLC who is treated as a partner for tax purposes, you can deduct the health insurance premiums you pay directly. If the partnership or LLC pays the premiums, you can still claim the deduction for premiums paid for your coverage by following special rules.

Furthermore, if you have an S-corporation, you should be aware of a 2015 notice regarding reimbursement for health premiums. The S-corporation can reimburse a shareholder for the cost of an individual market health plan, and then include the reimbursement amount in the shareholder's W-2 income. The shareholder can then deduct that amount using the self-employed health insurance deduction when filing their taxes.

Overall, self-employed individuals have the option to deduct health insurance premiums from their income taxes, providing a financial benefit and making health insurance more affordable.

Medical Indemnity Insurance: Understanding the Cost of Coverage

You may want to see also

Explore related products

![]()

Medical expenses exceeding 7.5% of adjusted gross income can be deductible

If you itemize your deductions for a taxable year on Schedule A (Form 1040), you may be able to deduct medical and dental expenses that exceed 7.5% of your adjusted gross income (AGI) for the year. This includes expenses for yourself, your spouse, and your dependents. It's important to note that the deduction only applies to expenses not compensated by insurance or other means.

To calculate the deductible amount, you need to multiply your AGI by 0.075 to find the threshold. Only expenses exceeding this threshold can be included as an itemized deduction. For example, if your AGI is $45,000 and your medical expenses are $5,475, you would multiply $45,000 by 0.075, resulting in a threshold of $3,375. This means you can deduct the amount above this threshold, which is $2,100 ($5,475 minus $3,375).

Medical care expenses eligible for deduction include payments for diagnosis, cure, mitigation, treatment, or prevention of disease, as well as treatments affecting the structure or function of the body. This can include inpatient hospital care, residential nursing home care (if medical care is the primary reason for residence), acupuncture treatments, inpatient treatment for drug addiction, smoking-cessation programs, prescription drugs, weight-loss programs for specific diagnosed diseases, and health club memberships for preventing or alleviating obesity. Additionally, you can deduct unreimbursed payments for preventative care, dental and vision care, visits to psychologists and psychiatrists, prescription medications, appliances like glasses and hearing aids, and travel expenses for qualified medical care.

It's important to note that certain expenses are not deductible, such as funeral or burial expenses, nonprescription medicines, toiletries, cosmetics, health improvement programs, cosmetic surgery, and nicotine replacement products that don't require a prescription. Furthermore, if you have a health insurance plan through your employer, the portion of the premiums treated as paid by your employer is generally not deductible. However, if you are self-employed and have a net profit, you may be eligible to deduct health insurance premiums, including Medicare Parts A and B, Medicare Advantage, and prescription drug plan premiums.

Prescription Coverage: Is It Included in Medical Insurance?

You may want to see also

Explore related products

![]()

Medicare Part A, B, C, and D premiums are deductible

Medicare premiums can be tax-deductible under certain conditions. Medicare Part A, B, C, and D premiums are deductible if you meet the criteria. If you are self-employed and your business shows a profit, you can claim your health insurance premiums, including Medicare Parts A and B, Medicare Advantage (Part C), and Part D prescription drug plan premiums, as a tax deduction. This deduction is applicable to your income tax return, not your employment taxes. Additionally, if your medical expenses, including Medicare plan premiums, exceed 7.5% of your adjusted gross income, and you itemize your deductions, you may be able to deduct these expenses.

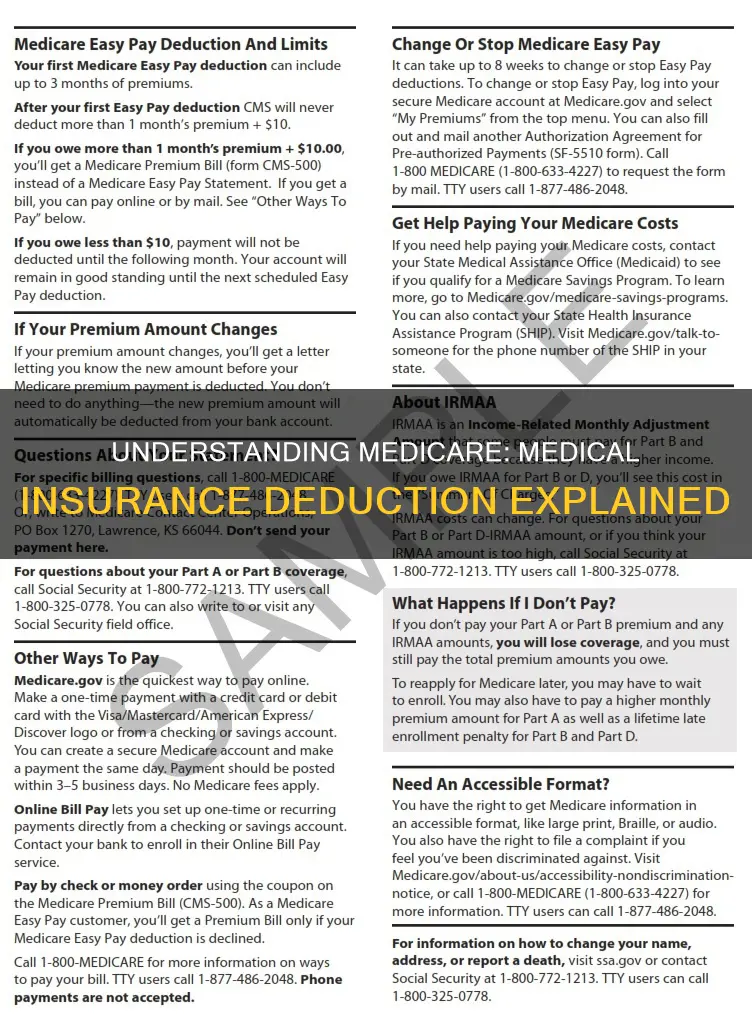

It is important to note that monthly premiums for Medicare vary based on factors such as the specific plan, your income, location, and other factors. The amount can also change annually. If you have limited income and resources, you may be eligible for assistance from your state in paying your premiums and other costs.

Medicare Part A (hospital insurance) premiums are usually not paid monthly by individuals who have worked and paid taxes. For those who need to pay for Part A, these premiums may be deductible. Medicare Part B (medical insurance) premiums are typically paid monthly, and these premiums are also deductible.

Medicare Part C, also known as Medicare Advantage, offers expanded coverage beyond Original Medicare and may include extra benefits. The premiums for Medicare Part C plans are deductible. Medicare Part D covers prescription drug plans, and the premiums for these plans are also deductible. It is important to note that Medicare Part D has a late enrollment penalty, but individuals with limited income and resources may qualify for assistance with the plan premiums and drug costs.

Medical Assistant Jobs: What Insurance Benefits Are Offered?

You may want to see also

Explore related products

![Medicare and Social Security: [5 in 1] Maximize Your Retirement Benefits, Secure Medical Coverage and Quality Healthcare | Proven Strategies to Protect Your Financial Future Avoiding Costly Mistakes](https://m.media-amazon.com/images/I/71sRJGiWeQL._AC_UL320_.jpg)

![]()

Medicare Advantage plans offer extra benefits beyond Original Medicare

Medicare Advantage plans, also known as Medicare Part C, are an alternative to Original Medicare. They are offered by Medicare-approved private companies and must follow the rules set by Medicare. These plans offer a range of benefits beyond what is covered by Original Medicare.

One of the key advantages of Medicare Advantage plans is their inclusion of prescription drug coverage, also known as Part D. While Original Medicare does not include prescription drug coverage, most Medicare Advantage plans include this benefit, helping to reduce the cost of medications for beneficiaries.

Medicare Advantage plans also typically cover vision, hearing, and dental services. This includes eyeglasses, eye exams, hearing aids, and routine dental care, which are not typically covered by Original Medicare. Additionally, many Medicare Advantage plans offer health and wellness programs aimed at promoting healthy lifestyles, preventive care, and disease management.

Some plans also provide coverage for fitness programs, caregiver support, meal delivery, acupuncture, and transportation services for non-emergency medical appointments. The availability of these benefits can vary depending on the insurance company and the specific plan chosen.

It is important to note that Medicare Advantage plans may have network limitations and prior authorization requirements for certain extra benefits. If you choose to receive care from providers outside of the plan's network, the extra benefits may not be covered or may be limited. Therefore, it is essential to carefully review the details of each plan and its associated benefits before making a decision.

Christian Health Ministries: Double Insurance or Smart Strategy?

You may want to see also

Explore related products

![]()

Self-employed individuals cannot deduct if eligible for an employer-sponsored health plan

Self-employed individuals can deduct their health insurance premiums, including medical, dental, vision, and long-term care insurance, from their income tax returns. This deduction is applicable if they have a net profit for the year and can be claimed on Schedule 1 (Form 1040), line 17. However, it's important to note that this deduction is not allowed if the self-employed individual is eligible to participate in an employer-sponsored health plan, including their spouse's employer or the employer of their dependent or child under the age of 27. This rule applies even if the individual does not actually participate in the employer-sponsored plan.

The IRS has specific criteria for this deduction, and eligible health insurance plans include medical insurance and all Medicare premiums (Parts A, B, C, and D). Self-employed individuals can deduct the premiums they paid during the year for themselves, their spouses, dependents, and any non-dependent children under the age of 27. This deduction is an adjustment to income rather than an itemized deduction.

It's important to note that self-employed individuals cannot include the premiums for months they were eligible for an employer-sponsored plan in their deduction. This restriction applies to both the individual's employer and the employers of their spouse, dependent, or child. Additionally, any medical insurance payments that cannot be deducted on Schedule 1 (Form 1040) can be included as medical expenses on Schedule A (Form 1040) if itemized deductions are made.

Self-employed individuals should carefully review the IRS criteria and consult a tax professional to determine their eligibility for deducting health insurance premiums and ensure they follow the correct procedures for claiming deductions on their tax returns.

Understanding Commercial Medical Insurance Plans

You may want to see also

Frequently asked questions

Medicare medical insurance deduction refers to the ability of some taxpayers to deduct their Medicare premiums and other eligible medical expenses from their income taxes.

Self-employed individuals who earn a profit from their business can deduct their Medicare premiums and other eligible health insurance premiums on Schedule 1 of Form 1040. This lowers their Adjusted Gross Income (AGI).

Yes, you cannot claim this deduction if you are eligible to enroll in an employer-subsidized health plan, either from your own employer or your spouse's. Additionally, the deductible premium amount cannot exceed the profits made by your business.

The following Medicare premiums may be deducted:

- Medicare Part A hospital insurance premiums, although most people do not pay a premium for this part.

- Medicare Part B medical insurance premiums, which are typically deducted from Social Security benefit payments.

- Medicare Part C (Medicare Advantage/MA) premiums.

- Medicare Part D (prescription drug plan) premiums.

- Medicare Supplement Insurance (Medigap) premiums.

![The Medicare Bible for Beginners: [3 in 1] Unlock Medical Benefits and Quality Healthcare | Super Easy Insider Strategies to Navigate Medicare While Avoiding Costly Mistakes](https://m.media-amazon.com/images/I/71tm-tSiWnL._AC_UL320_.jpg)