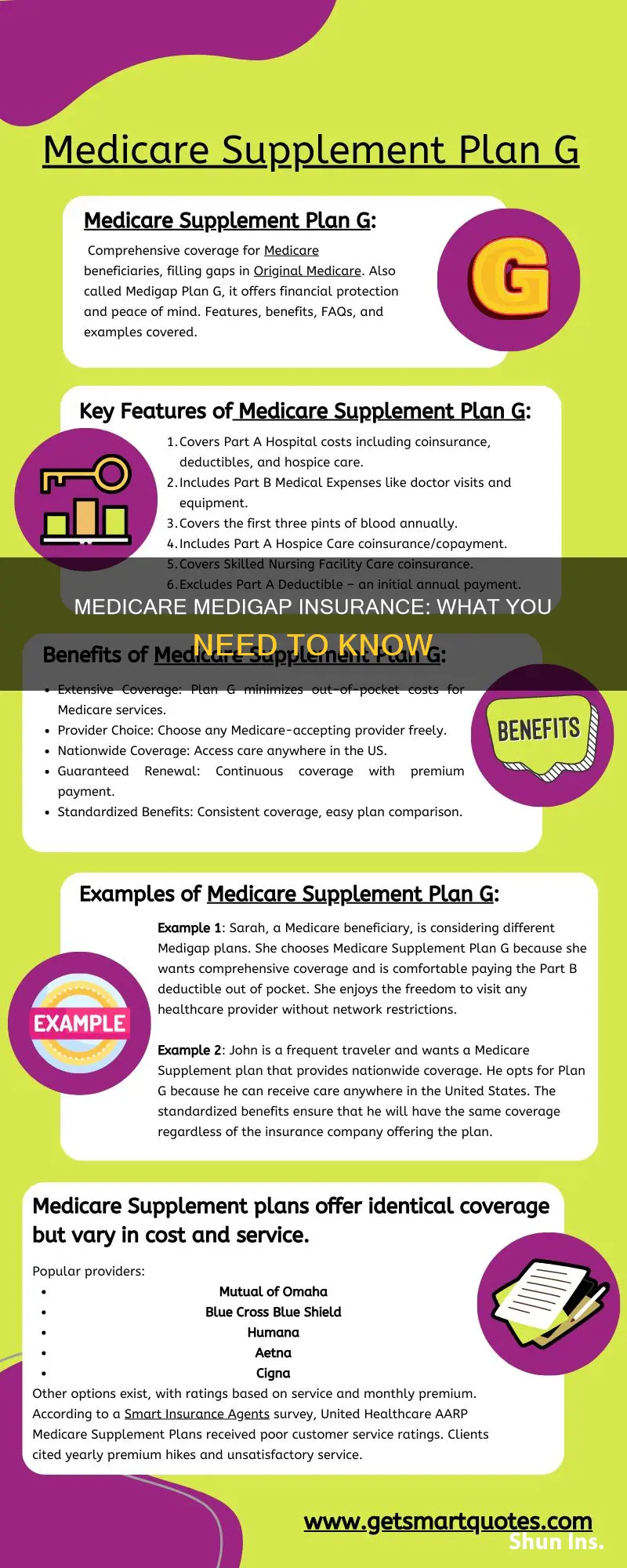

Medicare Supplement Insurance, also known as Medigap, is extra insurance you can buy from a private health insurance company to help pay for costs that Original Medicare (Part A and B) doesn't cover. Medigap policies are sold by private insurance companies to fill the gaps in Original Medicare Plan coverage. Generally, you must have Original Medicare – Part A (Hospital Insurance) and Part B (Medical Insurance) – to buy a Medigap policy. There are up to 10 Medicare Supplement plans offered in each state, ranging from basic to extensive coverage.

| Characteristics | Values |

|---|---|

| Type of Insurance | Medicare Supplement Insurance (Medigap) is extra insurance that can be purchased from a private health insurance company to supplement Original Medicare (Part A and B) |

| Purpose | Medigap helps pay for out-of-pocket costs that Original Medicare does not cover, such as about 20% of Medicare expenses |

| Enrollment Requirements | To purchase a Medigap policy, an individual must already be enrolled in both Original Medicare Part A (Hospital Insurance) and Part B (Medical Insurance) |

| Policy Standardization | Medigap policies are standardized and must follow Federal and state laws. The core benefits of Medigap plans are the same across different insurance companies, but costs can vary |

| Policy Renewal | Medigap policies are guaranteed renewable as long as the premium is paid. Coverage continues year after year with timely premium payments |

| Spouse Coverage | Each spouse must buy separate Medigap policies. A Medigap policy will not cover the healthcare costs of a spouse |

| Plan Types | There are up to 10 Medicare Supplement plans offered in each state, named alphabetically from Plan A to Plan N. The availability of specific plans may differ by state |

| Plan Costs | The cost of Medigap premiums depends on the insurance company and the type of Medigap plan chosen. Costs can vary between different insurance providers |

| Additional Benefits | Some Medigap policies offer extra benefits beyond those covered by Original Medicare, such as prescription and dental plans |

Explore related products

What You'll Learn

![]()

Medigap policies are sold by private insurance companies

Medicare Supplement Insurance, also known as Medigap, is extra insurance that can be purchased from a private health insurance company. Medigap policies are sold by private insurance companies to fill the "gaps" in Original Medicare Plan coverage. Generally, you must have Original Medicare Plan A (Hospital Insurance) and Plan B (Medical Insurance) to buy a Medigap policy. Medigap policies help pay some of the healthcare costs that the Original Medicare Plan doesn't cover.

Medigap policies are sold by a variety of private insurance companies, including Cigna Healthcare, which offers policies with competitive rates and up to 25% premium discounts. The cost of a Medigap policy depends on the insurance company and the type of Medigap plan selected. It's important to compare Medigap policies, as costs can vary, although the benefits provided by standardised Medigap policies are the same across different insurance companies.

When purchasing a Medigap policy, you will pay your insurance company a monthly premium. In addition to this premium, you will also need to pay the monthly Medicare Part B premium. As long as you pay your premium, your Medigap policy is guaranteed renewable, meaning it will automatically renew each year. Medigap policies are regulated by Federal and state laws, which protect consumers and ensure that policies provide the same core benefits regardless of the insurance company.

There are up to 10 Medigap plans offered in each state, named Plan A through Plan N. The types of plans offered may differ depending on the state, but each policy is standardised and offers the same basic benefits. Medigap plans range from basic to extensive coverage, and it's important to understand your healthcare and financial needs when choosing a plan. Some Medigap policies also cover extra benefits that aren't covered by Medicare.

Medical Insurance Premiums: Gross Income Implications?

You may want to see also

Explore related products

![Medicare and Social Security: [5 in 1] Maximize Your Retirement Benefits, Secure Medical Coverage and Quality Healthcare | Proven Strategies to Protect Your Financial Future Avoiding Costly Mistakes](https://m.media-amazon.com/images/I/71sRJGiWeQL._AC_UY218_.jpg)

![]()

Medigap policies fill the gaps in Original Medicare coverage

Medicare Supplement Insurance, also known as Medigap, is extra insurance that can be purchased from a private health insurance company to fill the gaps in Original Medicare (Part A and B) coverage. It helps pay for the out-of-pocket costs that Original Medicare does not cover, which can be significant for large medical bills. Medigap policies are sold by private insurance companies and help pay for some of the healthcare costs that Original Medicare does not. These policies are standardized, meaning they must follow federal and state laws, and the core benefits are the same no matter which insurer you choose.

There are up to 10 Medicare Supplement plans offered in each state, named Plan A through Plan N. These plans differ in the level of coverage they provide, ranging from basic to extensive. When choosing a plan, it is important to consider your healthcare needs and financial situation. The cost of a Medigap policy will depend on the insurance company and the type of plan selected. However, it's important to note that Medigap policies do not cover any healthcare costs for your spouse; separate policies must be purchased for each individual.

Medigap policies are guaranteed renewable as long as the premium is paid, and coverage will continue year after year. In some states, insurance companies may refuse to renew a Medigap policy purchased before 1992. Additionally, some Medigap policies offer extra benefits that are not covered by Medicare, such as prescription and dental plans.

Overall, Medigap policies provide valuable additional coverage for individuals with Original Medicare, helping to reduce out-of-pocket expenses and providing peace of mind. By understanding their healthcare needs and budget, individuals can choose the Medigap plan that best suits their specific requirements.

Understanding Your Medical Insurance Deductible

You may want to see also

Explore related products

![]()

Medigap policyholders pay a monthly premium

Medicare Supplement Insurance, or Medigap, is extra insurance that can be purchased from a private health insurance company. It helps to cover out-of-pocket costs that Original Medicare (Part A and Part B) does not. Medigap policies are designed to fill the "gaps" in Original Medicare Plan coverage, and they help pay some of the healthcare costs that the Original Medicare Plan doesn't cover.

Medigap policyholders are required to pay a monthly premium to their chosen private insurance company. This premium is separate from and in addition to the monthly Medicare Part B premium. The insurance company will communicate how to pay the monthly premium. The Medigap premium is set by each insurance company, and the price can vary depending on the company, the plan, and the policyholder's location.

The average monthly Medigap premium across all current policyholders varies depending on the specific plan. For example, for Plan G, the most popular and comprehensive plan available to new enrollees, the average monthly premium among current policyholders in 2023 was $164. This ranged from $140 in Washington, D.C., and $141 in Hawaii and New Mexico, to $236 in New York. On the other hand, Plan F, which is no longer available to new enrollees, has an average premium of $274, ranging from $214 in Vermont to $313 in New York.

It is important to note that Medigap policies are standardized, meaning they must follow Federal and state laws, and the benefits provided by each lettered plan are the same across insurance companies. The main difference between policies from different companies is the cost. Therefore, it is recommended to compare plans with the same letter when considering purchasing a Medigap policy. Additionally, Medigap policies do not cover spouses, so spouses must purchase separate policies.

Private Insurance Psychiatric Medication Coverage: What You Need Know

You may want to see also

Explore related products

![]()

Medigap policies are standardised

Medicare Supplement Insurance, or Medigap, is an additional insurance option that can be purchased from a private health insurance company. It is designed to help pay for out-of-pocket costs in Original Medicare, which consists of Part A (Hospital Insurance) and Part B (Medical Insurance). Medigap policies are standardised across the United States, with federal and state laws in place to protect consumers. These laws mandate that Medigap policies must be clearly identified as "Medicare Supplement Insurance" and that insurance companies can only offer standardised policies with the same benefits.

The standardisation of Medigap policies means that regardless of the insurance company, individuals will receive the same benefits. The only difference between policies from different companies is the cost. This standardisation allows consumers to easily compare policies and make informed decisions based on their needs and budget. It also ensures that individuals receive a consistent level of coverage, regardless of their chosen provider.

The standardisation of Medigap policies was established through the Omnibus Budget Reconciliation Act of 1990, with an effective date of July 31, 1992. Since then, Medigap policies have followed a standard format with ten specific benefit plans permitted by federal law. While states have the flexibility to allow all or some of these plans to be marketed, there is a basic benefit package, known as the "core benefit" plan, that must be offered in all states and by all companies selling Medigap insurance.

It is important to note that Medigap policies are individual-specific, and spouses must purchase separate policies. Additionally, some seniors may still be covered by non-standardised plans issued before 1992, which are no longer available for purchase. However, individuals with these old policies can choose to switch to a new standardised plan by comparing the benefits and costs to make an informed decision.

The standardised benefit policies are labelled by letters, with Policy A representing the basic or "core" benefits. The other policies build upon this core by including additional benefits, allowing individuals to choose a plan that best suits their specific needs and ensuring that they only pay for the coverage they require.

Indemnity Insurance: Steps to Apply and Get Covered

You may want to see also

Explore related products

![]()

Medigap policies are guaranteed renewable

Medicare Supplement Insurance, also known as Medigap, is extra insurance that can be purchased from a private health insurance company. Medigap policies are designed to help pay for out-of-pocket costs in Original Medicare (Parts A and B), filling in the "gaps" in coverage. These policies are guaranteed renewable, providing added assurance to policyholders.

The guarantee of renewal for Medigap policies means that as long as the policyholder continues to pay their premium, their coverage will be automatically renewed each year without interruption. This assurance of continuity ensures that individuals can rely on their Medigap coverage year after year, providing stability and peace of mind.

The automatic renewal of Medigap policies is a significant advantage for policyholders. It eliminates the worry of having to reapply for coverage annually and the potential risk of being denied renewal. This guarantee also ensures that individuals can maintain their chosen level of healthcare coverage without unexpected disruptions.

While Medigap policies are guaranteed renewable, there are certain circumstances under which an insurance company may refuse to renew a policy. In some states, insurance companies have the right to decline the renewal of Medigap policies purchased before 1992. Additionally, if a Medigap plan is no longer part of the Medicare program, the insurer must notify the beneficiary in advance and allow them to choose a new plan for the following year.

It is important to note that Medigap policies are standardized, meaning that all insurance companies offering Medigap must provide the same benefits for policies with the same letter. However, costs may vary between different insurance providers, so it is advisable to compare policies before purchasing. Understanding the guaranteed renewable nature of Medigap policies empowers individuals to make informed decisions about their healthcare coverage.

Medical Insurance Costs in California: Monthly Breakdown

You may want to see also

Frequently asked questions

Medicare Supplement Insurance, also known as Medigap, is private health insurance that adds on to Original Medicare (Part A and B). It helps pay for some of the healthcare costs that Original Medicare doesn't cover.

Medigap policies help pay for some of the healthcare costs that the Original Medicare Plan doesn't cover. These costs can include about 20% of Medicare expenses, as well as other extra benefits.

You can buy a Medigap policy from a private health insurance company. To purchase a Medigap policy, you must already be enrolled in both Original Medicare Part A and Part B.