Mortality risk is a fundamental concept in the insurance industry that plays a crucial role in determining insurance premiums and coverage. It refers to the likelihood of an individual's death within a specific period, taking into account various factors such as age, gender, health condition, occupation, and lifestyle choices. Insurance companies use medical information, including an individual's history of disease and the presence of risk factors, to classify the mortality risk of applicants. This information is then used to calculate the probability of policyholders making claims due to death-related events and set premiums accordingly. Mortality risk also affects the coverage offered by insurance policies, with certain high-risk individuals being excluded from certain types of coverage or facing limited options.

| Characteristics | Values |

|---|---|

| Definition | Mortality risk is the chance that an insurance company will have to pay out a death benefit sooner than expected. |

| Mortality and expense risk charge | A fee imposed on investors in annuities and other products offered by insurance companies. |

| Purpose of the charge | To compensate the insurer for any losses that it might suffer as a result of unexpected events, including the death of the annuity holder. |

| Factors determining the charge | The age of the investor, the net amount at risk under the policy, the risk classification of the policyholder, and the health status and coverage amount. |

| Range of the charge | From about 0.40% to about 1.75% per year. |

| Calculation | Based on assumptions about the life expectancy of the client and the likelihood of various other adverse events. |

| Risk assessment | The insurer assesses the likelihood of the policyholder's death within a specific year and assigns a cost to cover this risk. |

| Impact on insurance premiums | Mortality risk significantly influences the cost of insurance premiums. |

| Impact on coverage | Mortality risk affects the coverage offered by insurance policies. Certain high-risk individuals may be excluded from certain types of coverage altogether or may have limited options available to them. |

| Prediction | Insurance companies use medical information, including the history of disease and the presence of risk factors, to classify the mortality risk of applicants. |

Explore related products

What You'll Learn

![]()

Mortality and expense risk charges

The mortality component addresses the risk of paying out a death benefit sooner than expected. It is based on the likelihood of the policyholder's death within a given period, considering their life expectancy and the potential for adverse events. A younger applicant will generally result in a lower mortality and expense risk charge due to their higher life expectancy.

The expense component covers the costs associated with managing and administering the investment, such as administrative fees and operating expenses. These charges are intended to offset the expenses incurred by the insurer in providing income guarantees and other benefits included in the annuity contract.

The amount of the mortality and expense risk charge varies depending on factors such as the age of the investor, the net amount at risk under the policy, and the risk classification of the policyholder. The charge is typically expressed as a percentage of the account value and deducted annually, ranging from approximately 0.40% to 1.75% per year.

Understanding mortality and expense risk charges is crucial for both insurers and policyholders. It helps them assess the financial implications of mortality risk and make informed decisions regarding their financial planning and investment choices.

Mexican Investment Accounts: Are They Insured?

You may want to see also

Explore related products

![]()

Mortality risk prediction

Mortality risk is the chance that an insurance company will have to pay out a death benefit sooner than expected. Insurance companies use medical information to classify the mortality risk of applicants. The applicant's risk is estimated from their history of disease and the presence of risk factors. The younger the applicant, the lower the mortality risk.

In recent years, there has been a debate about adding genetic testing to mortality risk prediction. Proponents argue that genetic information could provide valuable insights into an individual's predisposition to certain diseases and conditions, improving the accuracy of risk assessment. However, critics argue that the potential benefits of genetic testing may be limited, especially for applicants with low absolute mortality risks. Additionally, there are ethical considerations and potential costs associated with genetic testing that could impact the feasibility of implementing it on a large scale.

To improve mortality risk prediction, insurance companies have been developing more sophisticated algorithms and models. These models consider a wide range of data points, including demographics, medical history, family history, and lifestyle factors. By analysing large datasets and using advanced analytics techniques, insurance companies can identify patterns and correlations that can help refine their risk assessments.

Accurate mortality risk prediction is crucial for insurance companies to set appropriate premiums and ensure the sustainability of their business. It also enables individuals to make informed decisions about their financial planning and health management. While mortality risk prediction has advanced significantly, it is important to recognise its limitations. Mortality is influenced by various factors, some of which may be unpredictable or beyond an individual's control. Therefore, mortality risk prediction should be just one aspect of a comprehensive risk management strategy.

Aetna Commercial: What's the Deal?

You may want to see also

Explore related products

![]()

Mortality charges

When determining mortality charges, insurers consider various factors, including the insured's age, health status, and coverage amount. The likelihood of the policyholder's death within a specific year is assessed, and a cost is assigned to cover this risk. Younger individuals tend to have lower mortality charges due to their higher life expectancy. Additionally, the mortality risk charge protects the insurance company from unexpected events, such as the untimely death of the policyholder.

The mortality and expense risk charge is calculated based on assumptions about the client's life expectancy and the probability of other adverse events. It aims to offset the cost to the insurer of any income guarantees included in the annuity contract. The charge compensates the insurer for potential losses resulting from unexpected events, including the death of the annuity holder. The average fee for this charge is approximately 1.25% per year, although it can range from 0.40% to 1.75% annually.

Underwriters typically consider three critical factors when determining mortality and expense risk charges: the net amount at risk under the policy, the risk classification of the policyholder, and the age of the policyholder. The insurance company invests a significant portion of the premium into a savings fund, which is returned to the policyholder upon maturity or to the nominee upon the policyholder's death.

Insurance companies use medical information, including family history and the presence of risk factors, to classify the mortality risk of applicants. This assessment helps set appropriate premiums and determine the likelihood of the policyholder's death within a specific timeframe.

Operational Risk: Insurable or Not?

You may want to see also

Explore related products

$39.65 $71.99

![]()

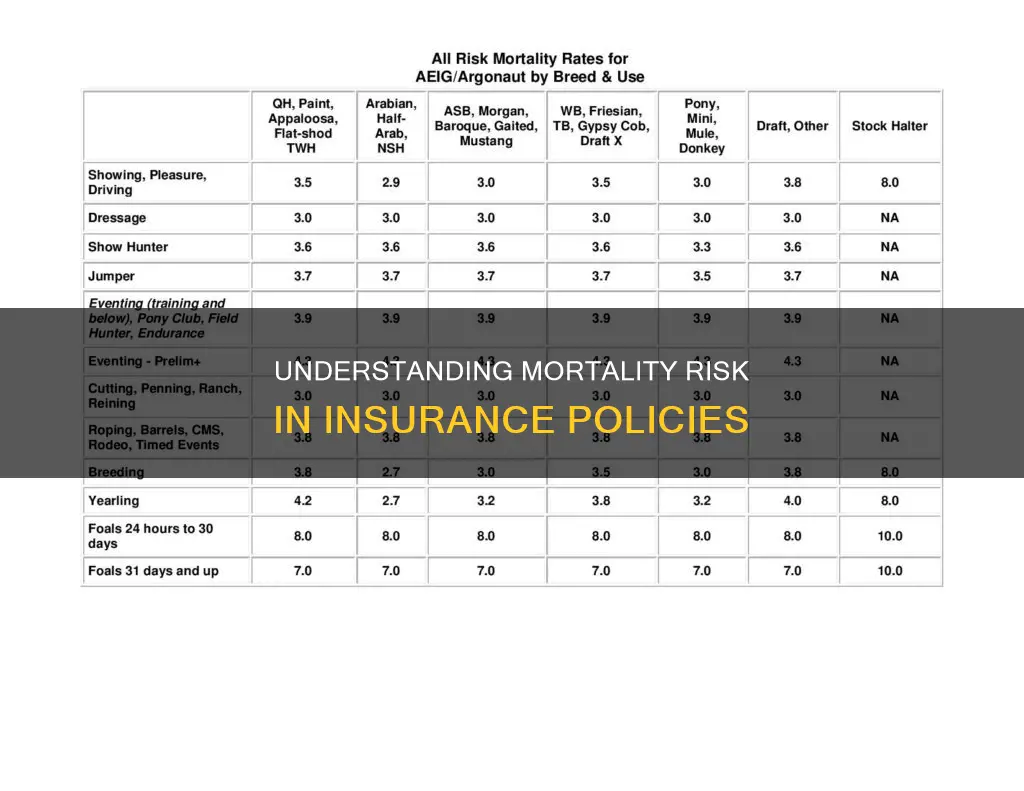

Valuation mortality tables

Mortality risk is the chance that an insurance company will have to pay out a death benefit sooner than expected. Insurance companies use medical information, including family history, to classify the mortality risk of applicants. The younger the applicant, the lower the mortality risk.

The National Association of Insurance Commissioners (NAIC) sets minimum reserve requirements for insurance and related products and updates this guidance periodically. The current table, based on 2010 data, became effective in May 2023. The NAIC and SAC update their tables less frequently, most recently transitioning from 2001 to 2017 CSO tables for all new products sold.

Dump Trucks: Commercial Insurance and Truckers' Policies

You may want to see also

Explore related products

![]()

Mortality risk and underwriting

Mortality risk is a fundamental concept in the insurance industry, and it plays a crucial role in determining insurance premiums and coverage. It refers to the likelihood of an individual's death within a specific period, taking into account various factors such as age, gender, health condition, occupation, and lifestyle choices.

Insurance companies assess mortality risk to calculate the probability of policyholders making claims due to death-related events. This assessment is a critical component of the underwriting process. Insurers use actuarial tables and statistical models, such as valuation mortality tables, to estimate the average life expectancy of different demographic groups. They also evaluate an applicant's health history, medical records, lifestyle habits, and family medical history to determine their mortality risk.

Based on this assessment, insurers make underwriting decisions, including whether to accept or reject an application or adjust the premium accordingly. The younger the applicant is, the lower the mortality and expense risk will be, and thus the lower the premium. Conversely, individuals with higher mortality risks, such as older adults or those with pre-existing medical conditions, are likely to face higher premiums compared to younger and healthier individuals.

Mortality risk also affects the coverage offered by insurance policies. Certain high-risk individuals may be excluded from certain types of coverage altogether or may have limited options available to them. For example, someone with a terminal illness may find it challenging to obtain life insurance coverage at affordable rates due to their heightened mortality risk.

In summary, mortality risk and underwriting are closely intertwined in the insurance industry. Insurers use mortality risk assessments to make informed decisions about accepting or rejecting applications, setting premium rates, and determining the coverage options available to applicants.

Risk Management: Chief Risk Officer's Role in Insurance

You may want to see also

Frequently asked questions

Mortality risk is a fundamental concept in the insurance industry that plays a crucial role in determining insurance premiums and coverage. It refers to the likelihood of an individual's death within a specific period, taking into account various factors such as age, gender, health condition, occupation, and lifestyle choices.

Insurance companies use medical information, including an individual's history of disease and the presence of risk factors, to classify their mortality risk. They also use actuarial tables and statistical models to estimate the average life expectancy of different demographic groups.

Mortality risk significantly influences the cost of insurance premiums. Individuals with higher mortality risks, such as older adults or those with pre-existing medical conditions, are likely to face higher premiums compared to lower-risk individuals.

Mortality risk also impacts the coverage offered by insurance policies. Certain high-risk individuals may be excluded from certain types of coverage or have limited options available to them. For example, someone with a terminal illness may find it challenging to obtain life insurance coverage at affordable rates due to their heightened mortality risk.