Mortgage insurance is a type of insurance that is required by lenders for homebuyers whose down payment is less than 20% of the home's purchase price. It protects the lender in the event that the borrower falls behind on their payments. There are several types of mortgage insurance, including private mortgage insurance (PMI), borrower-paid mortgage insurance (BPMI), lender-paid mortgage insurance (LPMI), and mortgage insurance premium (MIP). MIP is specifically required for loans backed by the Federal Housing Administration (FHA) and includes both upfront and annual payments. PMI rates vary based on the down payment amount and credit score, while BPMI is typically paid monthly along with regular mortgage payments. LPMI involves the lender covering the premium but results in a higher interest rate on the mortgage. Understanding the different types of mortgage insurance and their requirements is crucial for homebuyers to make informed decisions about their loans.

| Characteristics | Values |

|---|---|

| Type of insurance | Mortgage Insurance Premium (MIP) |

| Who requires it | Homeowners who take out loans backed by the Federal Housing Administration (FHA) |

| Who it protects | Lenders against financial loss in the event of borrower default |

| Who it does not protect | Borrowers—no insurance benefit if you fall behind on payments |

| When it is required | When the down payment is less than 20% of the purchase price |

| Cost | Upfront premium of 1.75% of the loan amount and an annual premium of 0.15% to 0.75% |

| Payment options | Monthly, upfront, or split |

| Tax implications | No longer deductible as of 2020 |

Explore related products

What You'll Learn

![]()

Mortgage insurance premium (MIP)

FHA-backed lenders use MIPs to mitigate the risk of lending to borrowers who may be more likely to default on their loans. This type of insurance is particularly relevant for borrowers with lower credit scores or those who make a down payment of less than 20% of the purchase price of the home.

MIP includes both upfront and annual costs. The upfront MIP is typically 1.75% of the loan amount, paid either in cash at closing or rolled into the loan. The annual payment ranges from 0.15% to 0.75% of the loan amount and is determined by factors such as the loan term, loan amount, and loan-to-value (LTV) ratio.

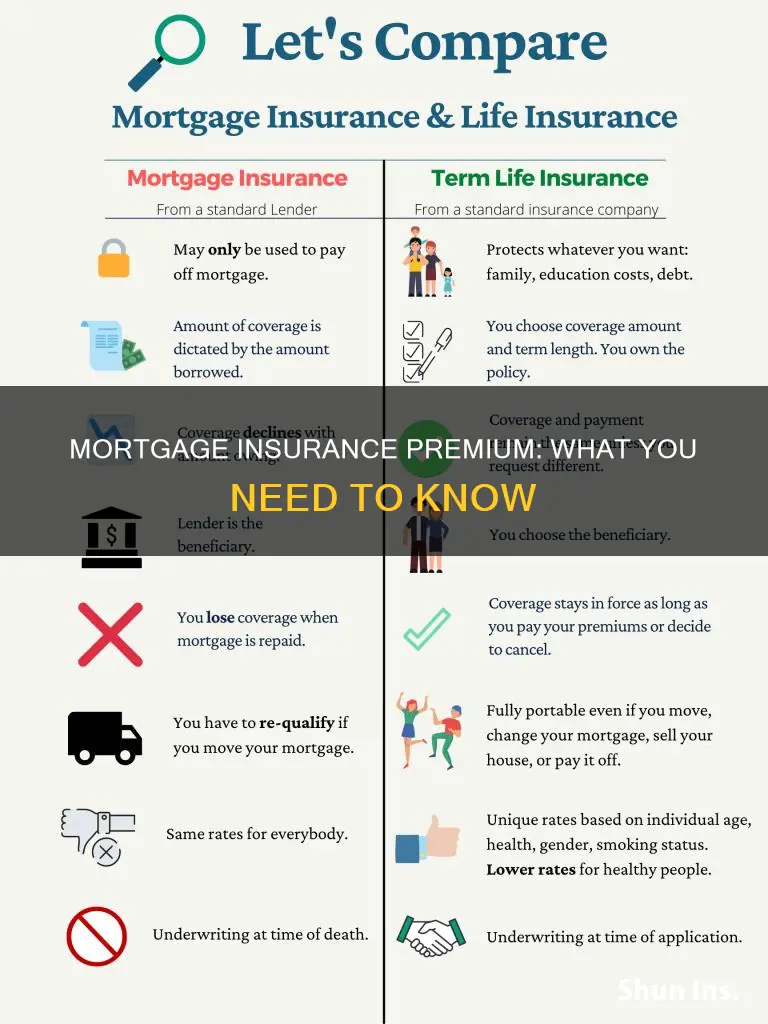

It's important to note that MIP should not be confused with private mortgage insurance (PMI). PMI is typically associated with conventional loans and is influenced by factors such as down payment amount and credit score. Unlike MIP, PMI rates can vary and are generally cheaper for borrowers with good credit. Additionally, PMI can be cancelled under certain circumstances, whereas MIP is required for the life of the FHA loan.

Until 2017, mortgage insurance premiums, including MIP, were tax-deductible. However, this deduction is no longer available unless specific criteria are met, such as in the case of the Further Consolidated Appropriations Act of 2020, which allowed tax deductions for MIP and PMI for the years 2018, 2019, and 2020.

Insuring Freighters in EVE: Worth the Cost?

You may want to see also

Explore related products

![]()

Private mortgage insurance (PMI)

PMI rates vary by down payment amount and credit score but are generally cheaper than FHA rates for borrowers with good credit. Most private mortgage insurance is paid monthly, with little or no initial payment required at closing. The exact cost of PMI and the rate at which it is paid will depend on the terms of the loan.

There are a few types of PMI. Borrower-paid mortgage insurance (BPMI) is the most common type, where the borrower pays a monthly premium that is attached to their regular mortgage payments. With lender-paid mortgage insurance (LPMI), the lender covers the premium, but the borrower pays a higher interest rate on their mortgage in exchange. Split-premium mortgage insurance allows the borrower to pay a portion upfront, typically at closing, and the rest over time with their monthly mortgage payments.

Under certain circumstances, PMI can be cancelled. For example, if you build up at least 20% equity in your home, you may be able to cancel your PMI. Additionally, PMI was tax-deductible for the years 2018, 2019, and 2020, but it is no longer deductible as of 2021.

It is important to note that PMI only protects the lender and not the borrower. If a borrower falls behind on their mortgage payments, they will not receive any insurance benefits, even though they are paying a monthly PMI premium.

Genworth Mortgage Insurance: Protecting Your Home Loan

You may want to see also

Explore related products

![]()

Federal Housing Administration (FHA) loans

FHA loans require mortgage insurance, which is paid to the FHA. This insurance is a way for lenders to protect themselves against higher-risk borrowers who are more likely to default on loans. The mortgage insurance premium (MIP) is paid by homeowners who take out loans backed by the FHA. FHA loans require both an upfront premium of 1.75% of the loan amount and an annual premium of 0.15% to 0.75%. The upfront premium is paid at the loan issuance, while the annual premium is paid monthly.

FHA loans are a good option for homebuyers who have not saved much for their down payments, with some loans requiring as little as 3.5% down. They are also a good option for those with lower credit scores, as the FHA insures these loans, so lenders are more willing to approve applicants with lower credit. Additionally, FHA loans can be used to buy a house and borrow the money needed to repair or upgrade it, all within a single mortgage.

It's important to note that FHA loans are not just for lower-income borrowers; they are available to everyone, including those who can afford conventional mortgages. However, there is a maximum loan amount that the FHA will insure, known as the FHA lending limit. This limit is calculated based on the median house prices in each county and increases annually for many counties in the United States.

DUI and Insurance: What to Report and When

You may want to see also

Explore related products

![]()

Conventional loans

When you take out a loan to buy a house, you may be required to pay for mortgage insurance. This is to lower the risk to the lender in case you fall behind on your payments. Mortgage insurance is typically required on conventional loans if you make a down payment of less than 20% of the purchase price of the home. This type of insurance is called private mortgage insurance (PMI) because it is provided by private companies and is not insured by the government. The cost of PMI depends on factors such as your credit score and the amount of your down payment. The higher your credit score and down payment, the lower your PMI premium will be.

Unlike Federal Housing Administration (FHA) loans, not every person who buys a house with a conventional loan is required to pay for mortgage insurance. If you make a down payment of 20% or more, you do not need to pay for PMI. However, if you make a down payment of less than 20%, you will most likely be required to pay for PMI by your lender.

With conventional loans, you pay PMI premiums monthly, as part of your regular mortgage payments. You can expect to pay an average of $30 to $70 per month for every $100,000 you borrow in PMI premiums. It's important to note that PMI rates are generally cheaper than FHA rates for borrowers with good credit. Additionally, under certain circumstances, you can cancel your PMI.

When deciding between a conventional loan and an FHA loan, it's essential to consider your financial situation and seek advice from a professional.

Islamic Law: House Insurance Compliance

You may want to see also

Explore related products

![]()

Lender-paid mortgage insurance (LPMI)

LPMI is often cheaper on a monthly basis than private mortgage insurance (PMI), but it may cost more over the life of the loan. With LPMI, the monthly mortgage payments do not include a separate line item for the insurance, but the cost is built into the mortgage rate. This results in a higher interest rate for the borrower, which cannot be cancelled or refunded, even if the loan-to-value (LTV) ratio reaches 80%.

LPMI can be a good option for those who don't plan to stay in their homes for a long time or who may refinance sooner. In these cases, the higher interest rate over the full loan term may not be a concern. Additionally, LPMI may be beneficial for those with excellent credit, as it can result in lower total monthly payments.

It's important to compare LPMI with other mortgage insurance options, such as borrower-paid mortgage insurance (BPMI), to determine the best choice based on individual circumstances. The decision should consider factors such as income, loan term, and plans for the property.

To summarise, while LPMI offers the advantage of lower monthly payments due to the absence of a separate insurance premium, it comes with the trade-off of a higher interest rate that cannot be cancelled. Therefore, careful consideration of one's financial situation and goals is necessary before opting for LPMI.

Freight Insurance: Worth the Cost?

You may want to see also

Frequently asked questions

Mortgage insurance is an additional layer of protection for the lender in the event that a borrower can't repay their loan. It is generally required when a homebuyer's down payment is less than 20% of the purchase price of the home.

MIP stands for Mortgage Insurance Premium. It is a type of mortgage insurance that is required for all homeowners who take out loans backed by the Federal Housing Administration (FHA). Unlike conventional loans, which may not require mortgage insurance, all FHA loans require MIP.

MIP includes an upfront cost of 1.75% of the total loan amount, paid as part of closing costs, and a monthly cost included in your monthly payments. The annual payment portion ranges from 0.15% to 0.75% of the loan amount.

PMI stands for Private Mortgage Insurance, which is generally required for conventional loans when the down payment is less than 20%. The cost of PMI depends on factors such as credit score and down payment amount, whereas FHA mortgage insurance costs are the same regardless of credit score.

You can pay the upfront MIP cost in cash at closing or roll it into your loan. The monthly MIP cost is included in your monthly mortgage payments.