Object-Oriented Programming (OOP) in the context of health insurance refers to the application of OOP principles—such as encapsulation, inheritance, and polymorphism—to design and develop software systems that manage health insurance processes. By organizing data and behavior into reusable objects, OOP simplifies the modeling of complex health insurance workflows, including policy management, claims processing, and provider networks. This approach enhances system modularity, scalability, and maintainability, allowing insurers to adapt quickly to regulatory changes and evolving customer needs. For instance, a policyholder object can encapsulate details like coverage limits and premiums, while inheritance can model different policy types based on a common base class. OOP thus streamlines health insurance operations, improves efficiency, and ensures robust, flexible solutions in a dynamic industry.

| Characteristics | Values |

|---|---|

| Definition | Out-of-Pocket (OOP) costs are expenses paid by the insured individual directly, not covered by the insurance plan. |

| Components | Deductibles, Copayments, Coinsurance, and Maximum Out-of-Pocket (MOOP) limits. |

| Deductibles | Fixed amount paid annually before insurance coverage kicks in. |

| Copayments | Fixed amount paid per service (e.g., doctor visit, prescription). |

| Coinsurance | Percentage of costs paid after the deductible is met (e.g., 20% of a procedure). |

| Maximum Out-of-Pocket (MOOP) | Annual limit on OOP costs; insurance covers 100% of costs beyond this. |

| Purpose | Encourages cost-sharing between the insured and insurer, reducing premiums. |

| Impact on Premiums | Higher OOP costs typically result in lower monthly premiums and vice versa. |

| Tax Implications | OOP expenses may be tax-deductible if they exceed a certain percentage of income. |

| Common in Plans | High-Deductible Health Plans (HDHPs) often have higher OOP costs. |

| Preventive Care | Often exempt from OOP costs under the Affordable Care Act (ACA). |

| Variability | OOP costs vary by plan type, insurer, and geographic location. |

| Consumer Responsibility | Requires policyholders to understand their OOP costs to avoid unexpected expenses. |

Explore related products

What You'll Learn

- OOP Basics: Out-of-pocket costs, including deductibles, copays, and coinsurance, in health insurance plans

- OOP Maximum Limits: Annual caps on out-of-pocket expenses to protect policyholders from excessive costs

- OOP vs. Premiums: How out-of-pocket costs differ from monthly premiums in health insurance

- OOP in HDHPs: Role of out-of-pocket costs in high-deductible health plans (HDHPs)

- OOP and Preventive Care: How out-of-pocket costs apply (or don’t) to preventive services

![]()

OOP Basics: Out-of-pocket costs, including deductibles, copays, and coinsurance, in health insurance plans

Out-of-pocket (OOP) costs are the expenses you pay directly for healthcare services before your insurance coverage kicks in or after it has been applied. These costs are a critical component of health insurance plans, shaping how much you spend annually on medical care. Understanding the three primary types of OOP costs—deductibles, copays, and coinsurance—is essential for navigating your plan effectively. Each functions differently, impacting your financial responsibility in distinct ways.

Deductibles are the amount you must pay out of pocket before your insurance begins covering costs. For example, if your plan has a $1,500 deductible, you’ll pay the full cost of covered services until you’ve spent $1,500. Only then does your insurance start sharing expenses. Deductibles reset annually, meaning you’ll need to meet this threshold each year. High-deductible plans often pair with Health Savings Accounts (HSAs), allowing you to save pre-tax dollars for medical expenses. However, preventive services like vaccinations or annual checkups are typically exempt from deductibles, ensuring you can access essential care without upfront costs.

Copays are fixed amounts you pay for specific services, such as a $25 fee for a doctor’s visit or $10 for a generic prescription. Copays are straightforward and predictable, making it easier to budget for routine care. They apply immediately, regardless of whether you’ve met your deductible. For instance, if you visit a specialist, you’ll pay the copay even if your deductible hasn’t been satisfied. Some plans tier copays based on service type—a $30 primary care visit versus a $50 specialist visit—so review your plan’s structure to avoid surprises.

Coinsurance is your share of costs after meeting your deductible, expressed as a percentage. For example, if your plan has 80/20 coinsurance, the insurer covers 80% of costs, and you pay 20%. This applies to services like hospitalizations or surgeries. Suppose a procedure costs $5,000. After meeting your deductible, you’d pay $1,000 (20%), and the insurer covers $4,000. Coinsurance can add up quickly, especially for expensive treatments, so understanding your plan’s split is crucial. Some plans cap out-of-pocket maximums, limiting your total annual liability, which includes deductibles, copays, and coinsurance.

To manage OOP costs effectively, analyze your healthcare usage. If you rarely visit the doctor, a high-deductible plan with lower premiums might save money. Conversely, frequent medical needs may justify higher premiums for lower deductibles and copays. Always compare plans during open enrollment, considering both premiums and OOP costs. Tools like healthcare.gov’s plan comparison feature can help you estimate total annual expenses based on your expected usage. Finally, keep detailed records of payments to track progress toward your out-of-pocket maximum and ensure accurate billing.

Understanding Medical Insurance Options During the OPT Grace Period

You may want to see also

Explore related products

![]()

OOP Maximum Limits: Annual caps on out-of-pocket expenses to protect policyholders from excessive costs

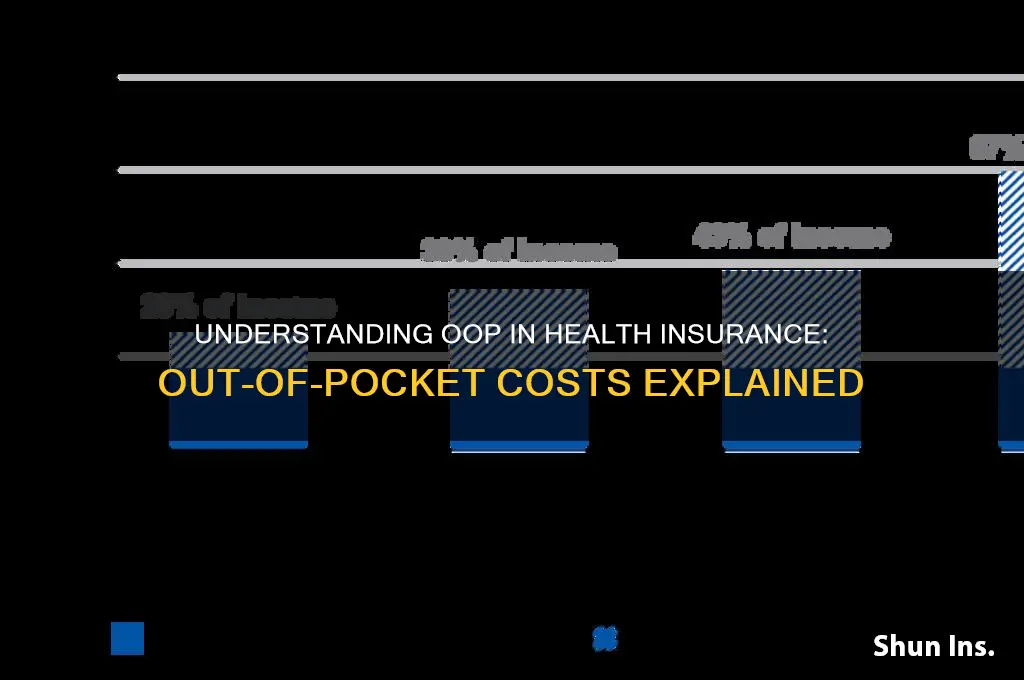

Out-of-pocket (OOP) maximum limits are a critical safeguard in health insurance, capping the total amount policyholders must pay annually for covered services before the insurer assumes full responsibility. These limits, typically ranging from $1,000 to $8,000 for individuals and double for families, are designed to prevent financial catastrophe from unexpected medical expenses. For instance, a policy with a $5,000 OOP maximum ensures that once a policyholder spends this amount on deductibles, copayments, and coinsurance, the insurer covers all remaining costs for the year. This protection is particularly vital for chronic conditions or sudden illnesses requiring extensive treatment.

Consider a 45-year-old with diabetes who requires frequent doctor visits, insulin prescriptions, and lab tests. Without an OOP maximum, their annual expenses could spiral into tens of thousands of dollars. However, with a $6,000 cap, their financial liability is predictable and manageable. This predictability allows individuals to budget for healthcare without fearing bankruptcy. It’s essential to note that OOP maximums do not include premiums, non-covered services, or out-of-network costs, so policyholders should review their plan details carefully.

When selecting a health insurance plan, compare OOP maximums alongside premiums and coverage breadth. Lower OOP limits often come with higher premiums, while higher limits reduce monthly costs but increase financial risk. For example, a plan with a $2,000 OOP maximum might cost $500 more annually in premiums than one with a $7,000 cap. Families with young children or individuals with pre-existing conditions may prioritize lower OOP limits for added security, while healthy, low-risk individuals might opt for higher limits to save on premiums.

To maximize the benefits of OOP maximums, policyholders should track their healthcare spending throughout the year. Many insurers provide online portals or apps to monitor OOP accumulators. Additionally, scheduling high-cost procedures early in the year can help reach the OOP limit sooner, shifting more expenses to the insurer. For instance, if a policyholder knows they need surgery, coordinating it early ensures subsequent treatments are fully covered. This strategic approach transforms the OOP maximum from a safety net into a tool for optimizing healthcare spending.

In summary, OOP maximum limits are a cornerstone of financial protection in health insurance, offering predictability and peace of mind. By understanding how these caps work and strategically managing healthcare expenses, policyholders can mitigate the risk of excessive costs. Whether prioritizing lower limits for comprehensive protection or higher limits for affordability, the key is aligning the OOP maximum with individual health needs and financial circumstances. This balance ensures that healthcare remains accessible without becoming financially overwhelming.

Equine Major Medical Insurance: What's Covered and What's Not

You may want to see also

Explore related products

![]()

OOP vs. Premiums: How out-of-pocket costs differ from monthly premiums in health insurance

Out-of-pocket (OOP) costs and monthly premiums are two distinct components of health insurance, each playing a unique role in how individuals manage healthcare expenses. While premiums are predictable, fixed payments made to maintain coverage, OOP costs are variable expenses incurred when healthcare services are used. Understanding this difference is crucial for budgeting and selecting the right insurance plan. For instance, a family with frequent doctor visits may prioritize a plan with lower deductibles and copays, even if it means higher premiums, to minimize OOP spending.

Consider the mechanics of these costs. Premiums are paid regardless of whether you use healthcare services, acting as a subscription fee for coverage. OOP costs, however, are triggered by specific events, such as a doctor’s visit, prescription refill, or hospital stay. These include deductibles (the amount paid before insurance kicks in), copayments (fixed fees per service), and coinsurance (a percentage of costs after the deductible). For example, a plan with a $1,500 deductible and 20% coinsurance means you pay the first $1,500 and then 20% of subsequent costs until reaching the out-of-pocket maximum, after which the insurer covers 100% of expenses.

The interplay between premiums and OOP costs highlights a trade-off in plan design. Plans with lower premiums often have higher OOP costs, such as a $7,000 deductible and 30% coinsurance, suitable for healthy individuals who rarely need care. Conversely, plans with higher premiums typically feature lower OOP costs, like a $500 deductible and $20 copays, ideal for those with chronic conditions or families anticipating frequent medical needs. Analyzing your healthcare usage patterns—such as annual prescriptions, specialist visits, or preventive care—can help determine which balance is most cost-effective.

Practical tips for managing these costs include maximizing preventive care, which is often covered at 100% with no OOP expense, and using generic medications to reduce copay amounts. For those with high-deductible plans, contributing to a Health Savings Account (HSA) can offset OOP costs with pre-tax dollars. Additionally, reviewing your Explanation of Benefits (EOB) after each service ensures accuracy in billing and helps track progress toward your out-of-pocket maximum. By strategically navigating premiums and OOP costs, individuals can optimize their health insurance investment while minimizing financial surprises.

Health Insurance and Medicaid: Florida's Dual Coverage

You may want to see also

Explore related products

![]()

OOP in HDHPs: Role of out-of-pocket costs in high-deductible health plans (HDHPs)

Out-of-pocket (OOP) costs in high-deductible health plans (HDHPs) serve as a financial threshold that policyholders must cross before insurance coverage fully kicks in. Unlike traditional plans, HDHPs pair lower monthly premiums with higher deductibles, shifting more upfront costs to the individual. For example, a typical HDHP might have a deductible of $2,000 for an individual or $4,000 for a family, meaning members pay these amounts annually before most services are covered. This structure is designed to encourage cost-conscious healthcare decisions, but it also requires careful planning to avoid unexpected financial strain.

The role of OOP costs in HDHPs extends beyond the deductible. These plans often include additional OOP components like copayments, coinsurance, and an out-of-pocket maximum. Copayments are fixed fees for specific services (e.g., $30 for a doctor’s visit), while coinsurance requires the member to pay a percentage of costs (e.g., 20% for a hospital stay). The out-of-pocket maximum, typically capped at $7,000 for individuals and $14,000 for families in 2023, limits total annual spending on deductibles, copayments, and coinsurance. Understanding these layers is critical for maximizing HDHP benefits while minimizing financial risk.

One practical strategy for managing OOP costs in HDHPs is pairing the plan with a Health Savings Account (HSA). HSAs allow individuals to save pre-tax dollars for qualified medical expenses, effectively reducing taxable income. For instance, contributing $1,000 to an HSA could save someone in the 22% tax bracket $220 annually. These funds can be used to cover deductibles, copayments, or even over-the-counter medications, making HDHPs more manageable. However, HSA eligibility requires enrollment in a qualified HDHP, and contributions are capped at $3,850 for individuals and $7,750 for families in 2023.

Despite their cost-saving potential, HDHPs are not ideal for everyone. Individuals with chronic conditions or frequent medical needs may find the high OOP costs burdensome. For example, a diabetic patient requiring regular insulin and doctor visits could face significant expenses before the deductible is met. In such cases, a traditional plan with higher premiums but lower OOP costs might be more suitable. Prospective enrollees should assess their health status, anticipated medical needs, and financial flexibility before choosing an HDHP.

In conclusion, OOP costs in HDHPs play a dual role: they incentivize cost-conscious healthcare decisions while requiring individuals to shoulder more upfront expenses. By understanding deductibles, copayments, coinsurance, and the out-of-pocket maximum, policyholders can navigate HDHPs effectively. Pairing an HDHP with an HSA offers a strategic way to offset costs, but this approach is best suited for those with predictable health needs and sufficient savings. Ultimately, the success of an HDHP hinges on aligning its structure with individual health and financial circumstances.

Medicare DRG Changes: Do Insurers Follow Suit?

You may want to see also

Explore related products

![]()

OOP and Preventive Care: How out-of-pocket costs apply (or don’t) to preventive services

Out-of-pocket (OOP) costs in health insurance typically include deductibles, copayments, and coinsurance, which can deter individuals from seeking necessary care. However, preventive services are a notable exception. Under the Affordable Care Act (ACA), most health plans are required to cover a range of preventive services without any OOP costs, meaning patients pay nothing for these services when provided by in-network providers. This includes vaccinations, screenings, and check-ups that are essential for early detection and disease prevention. For example, a 50-year-old individual can receive a colonoscopy, a critical screening for colorectal cancer, without incurring any OOP expenses if the procedure is coded as preventive.

The elimination of OOP costs for preventive care is rooted in a cost-benefit analysis. Preventive services reduce long-term healthcare expenses by identifying and addressing health issues before they escalate. For instance, a blood pressure screening for adults aged 18 and older can detect hypertension early, allowing for lifestyle changes or medication that prevent costly complications like heart disease or stroke. Similarly, immunizations such as the annual flu shot or the HPV vaccine for adolescents (aged 11–12) are fully covered, reducing the risk of widespread outbreaks and associated healthcare burdens. This approach aligns with public health goals, as it encourages individuals to prioritize their well-being without financial barriers.

Despite these provisions, confusion often arises when preventive services are bundled with diagnostic or treatment-related procedures. For example, a mammogram is covered without OOP costs as a preventive service for women over 40, but if an abnormality is found and additional imaging is required, the patient might be responsible for copays or coinsurance. To avoid unexpected costs, patients should verify with their insurer whether a service is classified as preventive and ensure the provider bills it accordingly. Additionally, some plans may require pre-authorization for certain screenings, such as a PSA test for prostate cancer, so proactive communication with the insurer is essential.

Employers and insurers also play a role in promoting the use of preventive services by educating plan members about their benefits. Wellness programs often incentivize participation in preventive care, offering rewards like reduced premiums or gift cards for completing annual physicals or health risk assessments. For families, ensuring children receive all recommended vaccinations (e.g., MMR, Tdap) by age 6 not only protects their health but also complies with school entry requirements, avoiding last-minute OOP expenses for catch-up doses. By leveraging these resources, individuals can maximize their coverage and minimize financial strain while staying proactive about their health.

In summary, OOP costs are waived for preventive services under most health plans, making essential care accessible and affordable. However, understanding the nuances of what qualifies as preventive and how services are billed is crucial to avoiding unexpected expenses. Patients should take advantage of fully covered screenings, vaccinations, and check-ups tailored to their age and risk factors, while also staying informed about plan-specific requirements. This approach not only supports individual health but also contributes to a more sustainable healthcare system by reducing the overall burden of treatable and preventable conditions.

Florida Insurance Crisis: Why Companies Are Dropping Customers

You may want to see also

Frequently asked questions

OOP stands for "Out-of-Pocket," which refers to the costs you pay for healthcare services that are not covered by your insurance plan.

OOP costs typically include deductibles, copayments, coinsurance, and any other expenses not covered by your insurance plan, up to your plan’s out-of-pocket maximum.

The out-of-pocket maximum is the most you’ll have to pay for covered services in a plan year before your insurance covers 100% of additional costs.

Plans with lower OOP costs (like copays and deductibles) often have higher monthly premiums, while plans with higher OOP costs usually have lower premiums. It’s a trade-off between upfront costs and potential expenses when you need care.