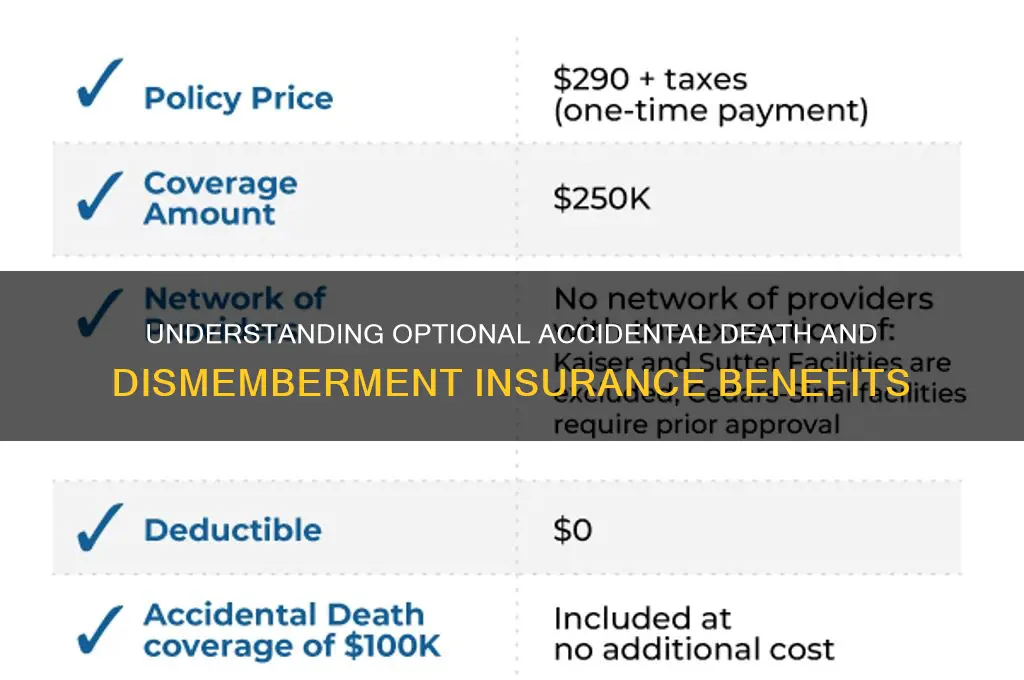

Optional Accidental Death and Dismemberment (AD&D) insurance is a supplemental coverage designed to provide financial protection in the event of severe accidents resulting in death, dismemberment, or loss of bodily functions. Unlike standard life insurance, AD&D specifically focuses on accidents, offering a lump-sum benefit to the policyholder or their beneficiaries if the insured dies or sustains serious injuries, such as the loss of a limb, sight, or hearing, due to an accident. This type of insurance is often offered as an add-on to existing policies or through employers, providing an extra layer of security for individuals and their families against the financial impact of unforeseen accidents. While not mandatory, it can be a valuable safeguard for those seeking comprehensive coverage beyond traditional health or life insurance.

| Characteristics | Values |

|---|---|

| Definition | Supplemental insurance providing financial benefits for accidental death or dismemberment (loss of limbs, sight, etc.). |

| Coverage Types | Death benefit, dismemberment benefit, paralysis benefit, and other specified losses. |

| Benefit Payout | Lump-sum payment to the beneficiary or policyholder based on the type of injury or death. |

| Premiums | Typically low-cost, with rates based on age, health, occupation, and coverage amount. |

| Policy Duration | Usually term-based (e.g., 1 year, renewable) or tied to an employer-sponsored plan. |

| Exclusions | Deaths or injuries due to illness, suicide, war, illegal activities, or high-risk activities (unless covered by rider). |

| Portability | Often portable if obtained through an employer, allowing continuation after job change. |

| Tax Treatment | Benefits are generally tax-free for the recipient. |

| Common Providers | Employers, insurance companies, or as an add-on to life insurance policies. |

| Eligibility | Available to individuals, employees, or groups, with minimal underwriting requirements. |

| Additional Riders | Optional riders may include coverage for specific high-risk activities or increased benefits. |

| Claim Process | Requires proof of accidental death or dismemberment, often involving medical documentation. |

| Typical Coverage Amounts | Ranges from $10,000 to $500,000, depending on the policy and provider. |

| Renewability | Often guaranteed renewable up to a certain age (e.g., 65 or 70). |

| Waiting Period | Minimal or no waiting period for coverage to begin after purchase. |

| Global Coverage | Many policies cover accidents worldwide, subject to policy terms. |

Explore related products

What You'll Learn

- Coverage Details: Includes death, limb loss, paralysis, and severe injuries due to accidents

- Eligibility Criteria: Available to individuals, employees, or group members, often with age limits

- Cost Factors: Premiums vary by age, health, occupation, and coverage amount chosen

- Claim Process: Requires proof of accident, medical records, and policyholder documentation for payout

- Exclusions: No coverage for illness, suicide, war, or high-risk activities unless specified

![]()

Coverage Details: Includes death, limb loss, paralysis, and severe injuries due to accidents

Optional Accidental Death and Dismemberment (AD&D) insurance is a supplemental coverage designed to provide financial protection in the event of severe accidents. The Coverage Details of this policy are specific and focus on critical outcomes resulting from accidents, including death, limb loss, paralysis, and severe injuries. This type of insurance complements existing life or health insurance by offering additional benefits for accidental incidents that lead to these specific conditions.

One of the primary components of AD&D insurance is coverage for death caused by accidents. If the insured individual dies as a result of an accident, the policy pays out a lump sum benefit to the designated beneficiaries. This benefit is typically in addition to any life insurance payout, providing extra financial support to the family during a difficult time. The key requirement is that the death must be directly attributable to an accident, as defined by the policy terms.

Another critical aspect of AD&D insurance is coverage for limb loss or dismemberment. This includes the loss of limbs such as arms, legs, hands, or feet, as well as the loss of sight, hearing, or speech due to an accident. The policy pays a specified benefit amount based on the severity of the loss, often as a percentage of the total coverage. For example, the loss of one limb might pay 50% of the policy’s face value, while the loss of multiple limbs could result in a higher payout.

Paralysis is also covered under AD&D insurance, provided it results from an accident. This includes both partial and total paralysis, with benefits paid out based on the extent of the condition. The policy terms will define what constitutes paralysis and the corresponding benefit amounts. This coverage is particularly important as paralysis often leads to long-term medical expenses and lifestyle adjustments.

Lastly, AD&D insurance covers severe injuries resulting from accidents, such as traumatic brain injuries, severe burns, or multiple fractures. The policy may provide benefits for these injuries based on their severity and impact on the insured’s life. Unlike health insurance, which covers medical expenses, AD&D insurance provides a lump sum payment that can be used to cover additional costs, such as rehabilitation, home modifications, or lost income.

In summary, the Coverage Details of Optional Accidental Death and Dismemberment insurance are tailored to address the financial consequences of severe accidents. By including benefits for death, limb loss, paralysis, and severe injuries, this policy offers a layer of financial security that goes beyond traditional life or health insurance. It is particularly valuable for individuals in high-risk professions or those seeking additional protection for their families in the event of a catastrophic accident.

Maximizing Life Insurance: Funding Your Future

You may want to see also

Explore related products

![]()

Eligibility Criteria: Available to individuals, employees, or group members, often with age limits

Optional Accidental Death and Dismemberment (AD&D) insurance is a supplemental coverage designed to provide financial protection in the event of accidental death or severe injuries, such as loss of limbs, sight, or hearing. While the core concept of AD&D insurance is widely understood, eligibility criteria play a crucial role in determining who can access this coverage. Eligibility Criteria for Optional AD&D insurance are structured to include a broad range of individuals while maintaining specific guidelines to manage risk. This coverage is available to individuals, employees, or group members, making it accessible through various channels, including personal policies, employer-sponsored plans, or membership in organizations like associations or unions.

For individuals, eligibility often depends on age, health status, and residency. Most insurers set age limits, typically ranging from 18 to 65 or 70, though some policies may extend coverage to older individuals with adjusted terms. Applicants may need to complete a health questionnaire or undergo a medical exam to assess their risk profile. Additionally, individuals must reside in a region where the insurer operates, as coverage is often geographically restricted. This direct-to-consumer approach allows people to purchase AD&D insurance independently, ensuring they have added financial protection beyond standard life or health insurance.

Employees are another key group eligible for Optional AD&D insurance, often as part of a voluntary benefits package offered by their employer. In this case, eligibility is usually tied to employment status, with full-time, part-time, or even temporary workers potentially qualifying. Age limits still apply, but these are generally aligned with the insurer’s standard guidelines. Employers may also set participation requirements, such as a minimum number of hours worked per week. Group policies through employers often simplify the enrollment process, as coverage is typically guaranteed without individual underwriting, making it an accessible and affordable option for workers.

Group members, such as those belonging to professional associations, credit unions, or alumni organizations, also have access to Optional AD&D insurance. Eligibility here is contingent on active membership in the group, and age limits are enforced similarly to individual and employee policies. Group coverage is often offered at discounted rates due to the collective purchasing power of the organization. Members may need to provide proof of membership and meet the group’s specific enrollment criteria. This option is particularly beneficial for individuals who may not have access to employer-sponsored plans but still seek additional financial protection.

It’s important to note that while Optional AD&D insurance is widely available, age limits are a consistent factor across all eligibility categories. Insurers impose these limits to manage risk, as older individuals are statistically more likely to file claims. However, some providers offer modified policies for seniors, though these may come with reduced benefit amounts or higher premiums. Understanding these eligibility criteria ensures that individuals, employees, or group members can make informed decisions about securing Optional AD&D insurance tailored to their needs. Always review the specific terms and conditions of a policy to confirm eligibility and coverage details.

Term Life Insurance: Getting Money Back

You may want to see also

Explore related products

![]()

Cost Factors: Premiums vary by age, health, occupation, and coverage amount chosen

Optional Accidental Death and Dismemberment (AD&D) insurance is a supplemental policy that provides financial protection in the event of accidental death or severe injury, such as loss of limbs, sight, or hearing. When considering this type of coverage, understanding the cost factors is crucial, as premiums can vary significantly based on several key elements: age, health, occupation, and the coverage amount chosen. These factors directly influence the risk perceived by insurers, which in turn affects the cost of the policy.

Age is one of the most significant determinants of AD&D insurance premiums. Younger individuals typically pay lower premiums because they are statistically less likely to experience accidents resulting in death or dismemberment. As age increases, so does the risk of accidents and health complications, leading to higher premiums. For example, a 25-year-old may pay significantly less than a 55-year-old for the same level of coverage. Insurers use actuarial tables to assess risk based on age, ensuring that premiums align with the likelihood of claims.

Health also plays a critical role in determining AD&D insurance costs. While AD&D insurance primarily covers accidents, pre-existing health conditions can still impact premiums. Individuals with chronic illnesses or conditions that increase the risk of accidents may face higher costs. Insurers may require a medical exam or review medical history to evaluate risk accurately. For instance, someone with a condition that affects mobility or cognitive function might be considered higher risk and thus pay more for coverage.

Occupation is another major factor influencing AD&D insurance premiums. Jobs with higher inherent risks, such as construction, law enforcement, or firefighting, typically result in higher premiums. Insurers categorize occupations into risk classes, with hazardous professions attracting steeper costs. Conversely, individuals in low-risk occupations, like office workers or teachers, generally pay less. Some insurers may also consider hobbies or lifestyle activities that increase the risk of accidents, further adjusting the premium accordingly.

The coverage amount chosen directly impacts the cost of AD&D insurance. Higher coverage limits mean larger potential payouts, which translates to higher premiums. Policyholders must balance their financial needs with their budget when selecting a coverage amount. For example, a policy with a $500,000 benefit will cost more than one with a $100,000 benefit. Additionally, some policies offer optional riders, such as coverage for paralysis or coma, which can further increase premiums based on the added protection.

In summary, the cost of optional AD&D insurance is not one-size-fits-all; it is tailored to individual circumstances. Age, health, occupation, and the desired coverage amount are the primary factors insurers consider when calculating premiums. By understanding these cost factors, individuals can make informed decisions about whether AD&D insurance is right for them and how much coverage they need. It’s advisable to compare quotes from multiple insurers to find the most competitive rates based on personal risk profiles.

Life Insurance Reinstatement in Florida: Understanding the Process

You may want to see also

Explore related products

![]()

Claim Process: Requires proof of accident, medical records, and policyholder documentation for payout

Optional Accidental Death and Dismemberment (AD&D) insurance provides additional financial protection in the event of accidental death or specific severe injuries, such as loss of limbs or eyesight. When filing a claim under this policy, the process is designed to ensure accuracy and legitimacy, requiring specific documentation to verify the circumstances of the accident and the policyholder’s coverage. The claim process is straightforward but detailed, emphasizing the need for proof of accident, medical records, and policyholder documentation to facilitate a successful payout.

The first step in the claim process involves providing proof of the accident. This typically includes a detailed accident report, which can be obtained from law enforcement, emergency services, or other relevant authorities. The report should clearly outline the date, time, location, and circumstances of the accident. For fatalities, a death certificate specifying the cause of death as accidental is mandatory. In cases of dismemberment or severe injury, a description of the event and its immediate aftermath is crucial. This documentation ensures the insurer can verify that the incident qualifies under the policy’s terms.

Next, medical records play a pivotal role in substantiating the claim. For dismemberment or injury claims, medical reports from treating physicians or hospitals are required to confirm the extent and nature of the injuries. These records should include diagnostic details, treatment plans, and prognoses. In the case of accidental death, an autopsy report or coroner’s statement may be necessary to validate the cause of death. The insurer uses these medical records to assess whether the injuries or death align with the policy’s covered conditions, such as loss of limb, paralysis, or other specified severe outcomes.

Equally important is the submission of policyholder documentation. This includes the original insurance policy or a copy of it, which outlines the coverage details, exclusions, and payout amounts. Additionally, proof of the policyholder’s identity and relationship to the beneficiary (if applicable) must be provided. For instance, a death claim would require the beneficiary to submit their identification and proof of their relationship to the deceased. This documentation ensures that the claim is filed by the rightful party and that the policy was active at the time of the accident.

Once all required documents are gathered, they must be submitted to the insurance provider according to their specified procedures. Many insurers offer online claim portals, while others may require physical submission of documents. It is essential to follow the insurer’s guidelines carefully to avoid delays. After submission, the insurer will review the claim, verify the documentation, and determine eligibility for payout. If approved, the beneficiary or policyholder will receive the benefit amount as outlined in the policy. Understanding and adhering to this claim process ensures a smoother experience during an already challenging time.

Life Insurance Licenses: Renewal Reminders and Deadlines

You may want to see also

Explore related products

![]()

Exclusions: No coverage for illness, suicide, war, or high-risk activities unless specified

Optional Accidental Death and Dismemberment (AD&D) insurance is designed to provide financial protection in the event of accidental death or specific severe injuries, such as loss of limbs or sight. However, it is crucial to understand the exclusions to ensure clarity on what is not covered. One of the primary exclusions is illness. AD&D insurance does not provide benefits for deaths or injuries resulting from sickness, disease, or natural causes. For example, if an insured individual passes away due to a heart attack or cancer, the policy will not pay out, as these are considered health-related issues rather than accidents.

Another significant exclusion is suicide. AD&D policies explicitly exclude coverage for self-inflicted injuries or death, regardless of the individual's mental health state at the time. This exclusion is standard across most insurance policies to prevent misuse and ensure the product remains financially viable for insurers. If death or injury occurs as a direct result of a suicide attempt, no benefits will be provided under the AD&D policy.

War is also a notable exclusion in AD&D insurance. Deaths or injuries sustained during active participation in war, whether as a member of the armed forces or a civilian, are not covered. This includes both declared wars and undeclared military conflicts. Additionally, injuries or deaths resulting from acts of terrorism may fall under this exclusion, depending on the policy's specific terms and conditions. It is essential to review the policy details to understand how such events are treated.

High-risk activities are another area where coverage is typically excluded unless explicitly specified in the policy. Activities such as skydiving, bungee jumping, racing, or participating in professional sports are often considered high-risk and may not be covered under a standard AD&D policy. However, some insurers offer optional riders that can extend coverage to include these activities for an additional premium. If an insured individual engages in a high-risk activity not covered by the policy and sustains an injury or dies, the claim will likely be denied.

Lastly, it is important to note that these exclusions are standard across most AD&D policies, but specific terms can vary between insurers. Policyholders should carefully review their policy documents to understand any additional exclusions or limitations. For instance, some policies may exclude coverage for injuries sustained while under the influence of drugs or alcohol, or while committing a felony. Being aware of these exclusions ensures that individuals can make informed decisions about their insurance needs and avoid unexpected denials of claims. Always consult with an insurance professional to clarify any uncertainties regarding coverage.

Credit Life Insurance: Protecting Your Financial Security

You may want to see also

Frequently asked questions

Optional AD&D Insurance is a supplemental insurance policy that provides financial benefits in the event of accidental death or specific severe injuries, such as loss of limbs, sight, or hearing, resulting from a covered accident.

Optional AD&D Insurance specifically covers deaths or injuries caused by accidents, whereas regular life insurance provides a payout upon the policyholder’s death regardless of the cause. AD&D is often an add-on to existing coverage.

Individuals with high-risk jobs, frequent travelers, or those seeking additional financial protection for their families in case of accidental death or severe injury may benefit from Optional AD&D Insurance.

Covered injuries typically include loss of limbs, paralysis, loss of sight or hearing, and other severe injuries specified in the policy. The exact coverage varies by provider, so it’s important to review the policy details.