Silver plans are a specific type of insurance plan offered through the Affordable Care Act (ACA). They are one of four categories of Health Insurance Marketplace plans, also known as metal levels, which include Platinum, Gold, Silver, and Bronze. Silver plans fall in the middle of the cost and coverage spectrum, where you pay moderate monthly premiums and moderate costs when you need care. Silver plans are unique among the four metal levels because they offer cost-sharing reductions (CSRs), which is financial help that lowers out-of-pocket costs for care. PPO, or Preferred Provider Organization, medical plans are a type of health insurance plan that offers flexibility in selecting doctors and hospitals within your plan's network. PPO plans are often offered to employees of small businesses, providing affordable group health insurance and freedom of choice.

PPO Silver Medical Insurance Characteristics and Values Table

| Characteristics | Values |

|---|---|

| Cost | Moderate monthly premiums and moderate costs when you need care. |

| Cost-sharing reductions (CSRs) | Financial help that lowers out-of-pocket costs for care. |

| Out-of-pocket maximum | The most you pay for your healthcare expenses annually. Once you reach the maximum, your insurer covers 100% of eligible healthcare costs for the rest of the plan year. |

| Coverage | Silver plans cover about 70% of the total cost of covered healthcare services on average. |

| Flexibility | You have the freedom to choose your doctors and hospitals within your plan's network. Out-of-network services are usually covered at a higher cost. |

| Prescription drugs | The specific medications covered can vary, and some prescription drugs may not be included. |

| Dental and vision coverage | Pediatric dental and vision coverage is included, but adult coverage is usually limited or not included. |

| Annual deductibles | Many silver plans have annual deductibles that you must meet before certain benefits kick in. |

| Plan variation | Availability, coverage, and cost can vary from state to state. |

Explore related products

What You'll Learn

![]()

Silver plans are one of four 'metal levels' of health insurance plans

Silver plans are one of four metal levels of health insurance plans offered through the Affordable Care Act (ACA). The other three metal tiers are Platinum, Gold, and Bronze. Silver plans are considered to fall in the middle of the cost and coverage spectrum of the four metal tiers. This means that you pay moderate monthly premiums and moderate costs when you need care.

Silver plans cover about 70% of the total cost of covered healthcare services on average, leaving the remaining 30% to be paid by the enrollee. This can include deductibles, copayments, and coinsurance. Silver plans are unique among the four metal levels because they offer cost-sharing reductions (CSRs), which is financial help that lowers out-of-pocket costs for care. If you qualify for CSRs, your insurer will automatically apply the savings to your plan, reducing your deductible, copays, coinsurance, and out-of-pocket maximum.

It is important to note that Silver plans are not the highest coverage tier available in the Health Insurance Marketplace. Gold and Platinum plans offer more comprehensive coverage, but they also come with higher premiums. When choosing a Silver plan, it is important to consider various factors, including affordability, coverage flexibility, and potential limitations to make an informed decision. Additionally, the availability, coverage, and cost of Silver plans can vary from one state to another, as health insurance plans are regulated at the state level.

Medical Record Privacy: Releasing to Insurance Companies

You may want to see also

Explore related products

![]()

Silver plans offer cost-sharing reductions (CSRs), which lower out-of-pocket costs

Silver health insurance plans are one of the four categories of Health Insurance Marketplace plans, also known as "metal levels". The other three tiers are Platinum, Gold, and Bronze. Silver plans are considered a mid-tier option, with moderate monthly premiums and moderate costs when you need care.

Silver plans offer cost-sharing reductions (CSRs), which are a form of financial help that lowers out-of-pocket costs for care. CSRs are unique to Silver plans and are designed to increase the actuarial value of the plan. This means that if you qualify for CSRs, your insurer will automatically apply savings to your deductible, copays, coinsurance, and out-of-pocket maximum. For example, if you have a Silver plan with a $3,000 deductible and you qualify for CSRs, your deductible may be reduced to $1,500, meaning you would only pay $1,500 out-of-pocket before your insurer starts paying for covered medical expenses.

The out-of-pocket maximum for Silver plans also varies depending on the specific plan and insurer, but there are annual limits for Marketplace plans. The Centers for Medicare & Medicaid Services state that for the 2025 plan year, the out-of-pocket limit for a Marketplace plan cannot exceed $9,450 for an individual and $18,900 for a family.

It's important to note that to qualify for CSRs, you must meet specific income requirements, generally no more than 250% of the federal poverty level. Additionally, Silver plans with robust CSR benefits can sometimes offer lower overall out-of-pocket costs than Platinum plans, which have higher premiums and lower out-of-pocket costs.

When considering a Silver plan, it's essential to review various factors, including affordability, coverage flexibility, and potential limitations, to make an informed decision about your healthcare needs.

Ohio Medical Malpractice Insurance: What's the Cost?

You may want to see also

Explore related products

![]()

Silver plans are ideal for those with modest incomes

The benefits of a Silver plan include coordinated care from doctors and hospitals within the same network, with the flexibility to choose your own healthcare providers. Out-of-network services are typically covered but may incur higher costs. Silver plans also provide access to in-network specialists without the need for a referral, and they cover essential health benefits such as annual check-ups, vaccines, screenings, and more, at no extra cost.

For individuals with modest incomes, Silver plans offer cost-sharing reductions (CSRs) or "extra savings". These CSRs lower out-of-pocket costs, including deductibles, copayments, and coinsurance. If you qualify for CSRs, your insurer will automatically apply the savings to your plan, reducing your financial burden. This feature of Silver plans makes them particularly attractive to those with modest incomes, as it enhances affordability without compromising on the quality of healthcare services.

Additionally, Silver plans have out-of-pocket maximums, which means that once you reach a certain annual limit, your insurer will cover 100% of eligible healthcare costs for the remainder of the plan year. This provides individuals with modest incomes protection against excessive healthcare expenses, ensuring that their financial liability for healthcare has a clear limit.

When considering a Silver plan, it is important to review various factors, including affordability, coverage flexibility, and potential limitations. The availability, coverage, and cost of Silver plans can also vary from state to state, so it is essential to research the specific details of the plan in your state. Overall, Silver plans offer a good balance of coverage and cost, making them a suitable option for those with modest incomes seeking comprehensive healthcare coverage.

Florida Medical Malpractice: Are Insurance Policies Mandatory?

You may want to see also

Explore related products

![]()

PPO plans offer freedom of choice and flexibility

Silver plans are one of the four categories of Health Insurance Marketplace plans, also known as "metal levels". They are considered a mid-tier option, with moderate monthly premiums and moderate costs when you need care. Silver plans are unique among the four metal levels because they offer cost-sharing reductions (CSRs), which provide financial help to lower out-of-pocket costs for care.

PPO plans, on the other hand, offer freedom of choice and flexibility. With a PPO plan, you have the freedom to choose any doctor or hospital you wish, whether they are in-network or out-of-network. This flexibility comes at a cost, as out-of-network services are typically covered at a higher price. PPO plans also tend to have higher monthly premiums than other types of plans.

The main advantage of a PPO plan is the freedom to choose your own healthcare providers without being restricted to a specific network. This can be especially beneficial if you have a preferred doctor or specialist who is out-of-network. PPO plans also offer flexibility in terms of seeking specialty care. With a PPO plan, you typically do not need a referral from your primary care physician to see a specialist, giving you the freedom to seek the care you need without additional steps.

Additionally, PPO plans offer a balance between cost and coverage. While they may have higher premiums than some other plan types, they often provide more comprehensive coverage for out-of-network services. This can be particularly advantageous if you require specialized care that may not be available within your network.

PPO plans are a good option for those who value the freedom to choose their healthcare providers and seek flexibility in their coverage options. They provide a balance between cost and coverage, making them a viable choice for those who want the option to access out-of-network care without incurring excessive expenses.

In summary, PPO plans offer freedom of choice and flexibility by allowing you to select your own healthcare providers, both in-network and out-of-network, and providing access to specialty care without the need for referrals. While they may come with higher costs, PPO plans offer a balanced approach to coverage and affordability, making them a popular choice for those seeking customizable healthcare options.

VA or Private Insurance: Which Medical Care is Right for You?

You may want to see also

![]()

PPO plans are available for small businesses

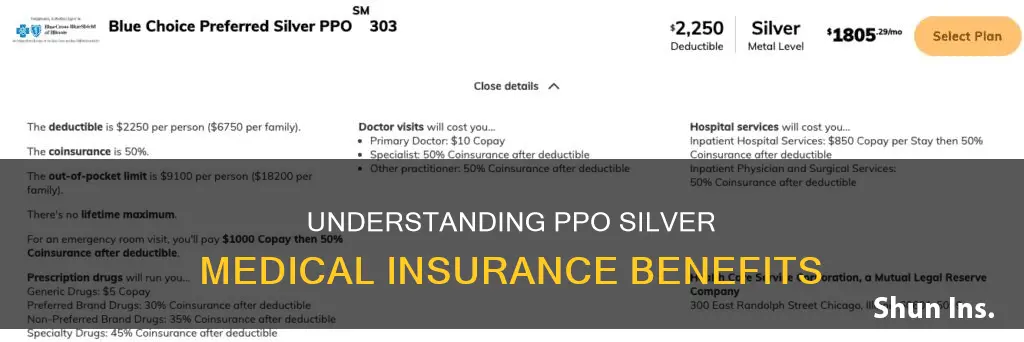

Silver healthcare plans are a specific type of insurance plan offered through the Affordable Care Act (ACA). Silver plans are unique among the four metal levels of plans because they offer cost-sharing reductions (CSRs), which lower out-of-pocket costs for care. This means that deductibles, copays, coinsurance, and out-of-pocket maximums will be lower than they would be without CSRs. For example, if you have a Silver plan with a $3,000 deductible and you qualify for CSRs, your deductible may be reduced to $1,500.

UnitedHealthcare's employer-sponsored insurance plans serve groups of different sizes, with Small Group plans referring to employers with up to 100 employees. They offer a range of group health plans and network options, as well as integrated pharmacy benefits to help lower costs for employers and employees.

Blue Cross and Blue Shield of Illinois offer flexible PPO and HMO health insurance plans for small businesses based on budget and needs. They provide health insurance quotes for small businesses in Illinois, allowing employers to compare coverage options and estimated monthly costs to choose the right plan for their employees.

Small businesses can benefit from providing health insurance for their employees, as it can help boost productivity and show that the company cares about their employees' health and wellness.

Medicare Plan Jargon: Supplemental Insurance Explained

You may want to see also

Frequently asked questions

Silver healthcare plans are a specific type of insurance plan offered through the Affordable Care Act (ACA). Silver plans fall in the middle of the four metal tiers of ACA Marketplace healthcare plans. They have moderate monthly premiums and moderate costs when you need care.

Cost-sharing reduction is financial help that lowers out-of-pocket costs for care. Silver plans are eligible for CSRs, and if you qualify for them, your insurer will automatically apply the savings to your plan. This means that your deductible, copays, coinsurance, and out-of-pocket maximum will be lower.

Silver plans cover about 70% of the total cost of covered healthcare services on average, so you are responsible for the remaining 30%. This can include deductibles, copayments, and coinsurance.

Silver plans, like all Marketplace plans, are required to cover a set of essential health benefits, including outpatient care, emergency services, and inpatient care (hospitalization). They also include pediatric dental and vision coverage, but adult dental and vision coverage is usually limited or not included.

PPO medical plans offer employees of small businesses affordable group health insurance and freedom of choice. A Silver PPO plan would likely refer to a Silver-tier plan within a PPO network.