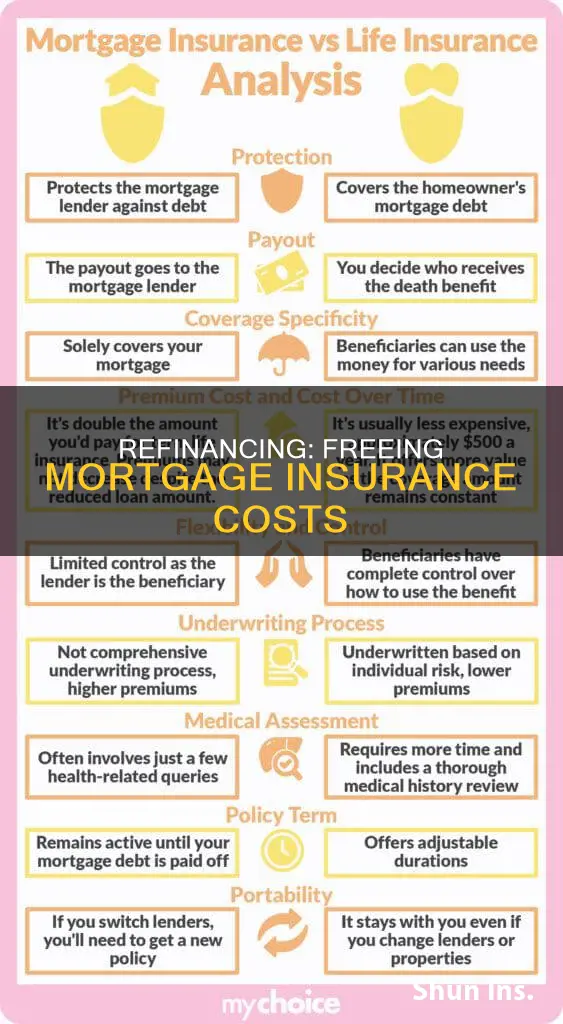

When you buy a home, you may be required to pay mortgage insurance, which protects the lender in case you default on your loan. This insurance is usually required if you put less than 20% down on your home. However, there are ways to get rid of mortgage insurance, such as refinancing your mortgage to a new loan with a lower balance. Refinancing can help you reach the mortgage insurance cancellation window sooner, but it's important to consider the costs involved, such as closing costs, and determine if refinancing will result in overall savings.

| Characteristics | Values |

|---|---|

| When to refinance | When interest rates have decreased |

| Purpose of refinancing | To get a lower rate and lower monthly payments |

| Private Mortgage Insurance (PMI) | Required when the value of home equity is less than 20% |

| Cancelling PMI | Automatic cancellation when mortgage balance reaches 78% of the home's purchase price or at the halfway point of the loan term |

| Requesting PMI cancellation | When mortgage balance reaches 80% |

| Refinancing costs | Closing costs between 2% to 6% of the loan amount |

Explore related products

What You'll Learn

![]()

Refinancing costs money, but can make sense depending on your finances

Refinancing can be a great way to save money, but it's important to remember that it's not a free process and there are costs involved. These costs can include closing costs, which can range from 2% to 6% of the total loan amount, as well as flat fees such as application and credit check fees, and percentage-based charges like origination fees.

So, how do you know if refinancing makes financial sense for you? Well, one way is to calculate your break-even point. This is the point at which your savings from refinancing equal the costs. For example, if refinancing saves you $100 a month and your closing costs are $2,400, it will take you 24 months to break even. If you plan to stay in your home beyond the break-even point, refinancing could be a good option.

Another thing to consider is your interest rate. Refinancing can help you take advantage of lower interest rates, which can reduce your monthly payments and the total amount of interest you pay over the life of the loan. However, if you refinance to a higher interest rate, you may not save money in the long run.

Your credit score is also important. A higher credit score can help you get a lower interest rate and reduce the cost of refinancing. It's a good idea to get your credit in the best shape possible before applying for refinancing.

Additionally, refinancing can be a way to get rid of private mortgage insurance (PMI). If you have a conventional loan and your home equity is 20% or more, you may be able to refinance and cancel your PMI.

Finally, refinancing can also give you the opportunity to change the length of your loan term. You can refinance to a longer term to lower your monthly payments or to a shorter term to pay off your mortgage faster and save on interest.

In conclusion, while refinancing costs money, it can make sense depending on your financial situation. It's important to do your research, compare costs and savings, and consider your interest rate, credit score, and loan term to determine if refinancing is the right choice for you.

Strategies for Affording Home Insurance

You may want to see also

Explore related products

![]()

Lower interest rates can prompt people to refinance

Refinancing a mortgage means paying off an existing loan and replacing it with a new one. One of the most common reasons to refinance is to secure a lower interest rate.

Interest rates are cyclical, and when they drop, many consumers refinance their mortgages to take advantage of the lower rates. This can result in substantial savings on the total cost of the loan. Even a small drop in the interest rate of 1%, 0.5%, or even 0.25% can make refinancing worthwhile, depending on your existing mortgage loan and financial goals. A lower interest rate can reduce short- and long-term interest payments while lowering monthly payments.

However, refinancing is not free. There are closing costs, which could range from 2% to 6% of the total loan amount. These include origination fees, appraisal fees, title services, underwriting, and more. Some lenders may offer to roll these fees into the loan, but this will increase the loan amount. Others may offer a "no-cost" refinance, but this usually comes with higher interest rates to offset the cost to the creditor. Therefore, it is important to weigh the upfront costs against the long-term savings to determine if refinancing is the right decision.

In addition to lowering interest rates, refinancing can also help homeowners switch to a fixed-rate mortgage to avoid future interest rate hikes or extend the loan term to reduce monthly payments. Refinancing can also be used to tap into home equity to raise money for a large purchase, consolidate debt, or deal with a financial emergency.

ACV Insurance: Is It Worth the Cost?

You may want to see also

Explore related products

$5.99 $12.99

![]()

Refinancing can help you reach the PMI cancellation window sooner

Refinancing your mortgage can be a good idea if today's interest rates are significantly lower than the rate on your current mortgage. This is because the savings from refinancing need to be worth it after you pay the refinance closing costs. If mortgage rates have decreased, refinancing to a new loan with a lower balance could help you reach the Private Mortgage Insurance (PMI) cancellation window sooner. This is because refinancing can help you build up the required amount of equity in your home faster.

PMI is a policy you must buy to protect your lender in the event that you default on your mortgage, and you typically pay premiums as part of your monthly mortgage payment. Federal law requires mortgage lenders to automatically cancel PMI when the balance of the mortgage drops to 78% of the home's purchase price, or when the loan term is at its halfway point, whichever comes first. You can also request cancellation when your mortgage balance reaches 80% of the home's purchase price.

If you refinance, the \"original value\" of your home is the appraised value at the time you refinanced. You can request PMI cancellation as long as you can provide evidence that the value of your property hasn't declined below the original value. You'll need to pay closing costs and provide documentation of your home's value and your income, assets and credit. Closing costs can be between 2% and 6% of the total loan amount and typically include origination fees, appraisal fees, title services, and underwriting.

Refinancing can be a good option if you can lower your interest rate, but it's important to do your research and consult a financial advisor if you're unsure. You should also be aware of mandatory waiting periods that can make it difficult to refinance within a year of buying a home.

Rideshare Insurance: Is GEICO's Coverage Worth the Cost?

You may want to see also

Explore related products

![]()

You can refinance to a conventional loan to get rid of MIP

Refinancing your mortgage can be a great way to save money and secure your financial future. If you have an FHA loan, you are required to pay for Mortgage Insurance Premium (MIP) for at least 11 years, or for the entire length of the loan, depending on the terms. MIP is a type of insurance that protects the lender in case you default on your mortgage, and it is required for all FHA loans, regardless of the down payment amount.

One way to get rid of MIP is to refinance to a conventional loan. When you refinance, you take out a new loan to pay off your existing FHA loan. If you have sufficient equity (generally 20% or more), you can refinance into a conventional loan without any mortgage insurance required. This is because, with a conventional loan, you can avoid mortgage insurance altogether if you have at least 20% equity. Additionally, refinancing can potentially lower your interest rate and monthly payments, and give you access to cash for other financial goals.

However, it's important to note that refinancing costs money, and it may only make financial sense if you can lower your interest rate. There are closing costs, which can range from 2% to 6% of the total loan amount, and these usually include origination fees, appraisal fees, title services, and underwriting. Some lenders may offer to roll these fees into the loan, but this will increase the total amount you owe. There are also "no-cost" refinance options, but these usually come with higher interest rates.

Before deciding to refinance, it's crucial to do your research and consider all the costs and potential savings. You can use a refinance calculator to estimate how much you might save by refinancing, and calculate a break-even point to see how long it will take for your savings to outweigh the costs. If you're unsure, you can always consult a financial advisor to help you determine if refinancing is the right move for you.

Farmers Insurance Open Tees Off at Torrey Pines: When and What to Expect

You may want to see also

Explore related products

![]()

You can avoid PMI if your home equity is 20% or more

Private mortgage insurance (PMI) is a type of insurance that mortgage lenders require when buyers make a down payment of less than 20% of the home's purchase price. It protects the lender if the borrower defaults on their loan. Typically, the buyer must pay premiums as part of their monthly mortgage payment. However, federal law requires lenders to cancel PMI when the mortgage balance reaches 78% of the home's purchase price or when the loan term is halfway through. Buyers can also request an early cancellation when their mortgage balance reaches 80%.

One way to reach the PMI cancellation window sooner is by refinancing to a new loan with a lower balance. Refinancing can help lower interest rates and monthly payments. However, it is not free and typically only makes financial sense if the new interest rate is significantly lower. Closing costs for refinancing can range from 2% to 6% of the total loan amount and may include origination fees, appraisal fees, title services, and underwriting.

If your home reaches the 20% equity level ahead of the mortgage payment schedule, you can consider paying for a new appraisal to get a higher valuation. If your loan balance is no more than 80% of the new valuation, you can request PMI cancellation. This can be achieved through price appreciation or by making significant home improvements. An appraisal typically costs a few hundred dollars, depending on the location and characteristics of the property.

It is important to note that refinancing may result in higher total finance charges over the life of the loan. Additionally, refinancing with a conventional loan while having less than 20% equity in your home will require PMI. Therefore, it is crucial to carefully consider the costs and potential savings before deciding to refinance. Consulting with a financial advisor can provide valuable insights into whether refinancing is the right decision.

Insuring Your New Home: When to Start

You may want to see also

Frequently asked questions

Refinancing is when someone takes advantage of lower interest rates or changes the repayment term of their mortgage.

Mortgage insurance is an additional cost that you may face when buying a home. It protects the lender from the risk that a buyer might default on their loan.

Refinancing can make mortgage insurance free by removing Private Mortgage Insurance (PMI) when the new mortgage balance is less than 80% of the home value.

Yes, there are a few other ways to get rid of mortgage insurance. One way is to wait for automatic or final termination, which occurs when the mortgage balance reaches 78% of the home's purchase price. Another way is to request cancellation when the mortgage balance reaches 80%. Lastly, you can pay down your mortgage faster to reach the 20% equity level ahead of schedule.