Retirement insurance, also known as pension insurance or retirement benefits, is a financial product designed to provide individuals with a steady income stream after they stop working. It serves as a safety net, ensuring financial security and peace of mind during one's golden years. This type of insurance typically involves regular contributions made by individuals or their employers throughout their working lives, which are then invested to grow over time. Upon retirement, policyholders receive payouts in the form of annuities, lump sums, or regular income payments, depending on the plan's structure. Retirement insurance plans can be offered by governments, employers, or private insurance companies, each with varying features and benefits, catering to different needs and preferences. Understanding the intricacies of these plans is crucial for individuals to make informed decisions about their financial future and ensure a comfortable retirement.

| Characteristics | Values |

|---|---|

| Definition | A financial product designed to provide income and security during retirement. |

| Purpose | Ensures a steady stream of income after retirement, replacing or supplementing employment income. |

| Types |

|

| Funding Sources |

|

| Tax Benefits |

|

| Vesting Period | Time required for employees to gain full ownership of employer contributions (varies by plan). |

| Withdrawal Rules |

|

| Portability | Ability to transfer retirement savings between employers or plans (e.g., 401(k) rollovers). |

| Investment Options | Varies by plan (e.g., stocks, bonds, mutual funds, target-date funds). |

| Risk Factors |

|

| Government Role | Regulates retirement plans (e.g., IRS, DOL) and provides social security benefits. |

| Global Variations | Retirement systems differ by country (e.g., 401(k) in U.S., Superannuation in Australia, NPS in India). |

| Trends |

|

Explore related products

$15.45 $14.95

What You'll Learn

- Types of Retirement Insurance: Explore annuities, pensions, and other plans for steady post-retirement income

- Eligibility Criteria: Understand age, employment, and contribution requirements to qualify for retirement insurance

- Benefits and Coverage: Learn about income replacement, healthcare, and survivor benefits offered by retirement insurance

- Cost and Premiums: Factors like age, health, and coverage level that determine retirement insurance costs

- Tax Implications: Discover how retirement insurance payouts and contributions affect your tax liabilities

![]()

Types of Retirement Insurance: Explore annuities, pensions, and other plans for steady post-retirement income

Retirement insurance is a critical component of financial planning, designed to provide individuals with a steady stream of income after they stop working. It ensures financial security and peace of mind during retirement years. There are several types of retirement insurance plans, each with unique features and benefits tailored to different needs. Among the most common are annuities, pensions, and other specialized plans, all aimed at guaranteeing a reliable post-retirement income.

Annuities are one of the most popular forms of retirement insurance. An annuity is a financial product sold by insurance companies that provides a fixed or variable stream of income in exchange for a lump-sum payment or a series of payments. There are two primary types: immediate annuities, which begin payouts shortly after the initial investment, and deferred annuities, which accumulate value over time and start payouts at a later date. Annuities can be structured to provide income for a specific period or for life, making them a flexible option for retirees seeking predictable cash flow. Fixed annuities guarantee a set payout, while variable annuities offer the potential for higher returns based on investment performance, though they carry more risk.

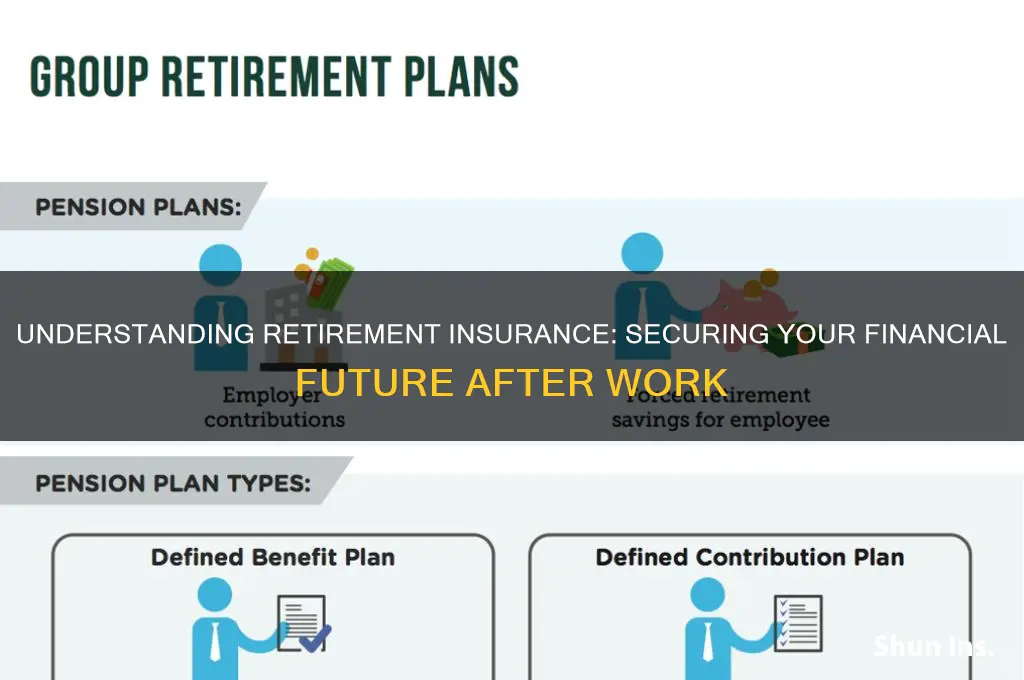

Pensions are another traditional form of retirement insurance, often provided by employers as part of a benefits package. A pension plan is a defined benefit plan where the employer promises to pay the employee a specific amount upon retirement, typically based on factors like salary history and years of service. Pensions provide a stable, guaranteed income for life, which can be particularly valuable in retirement planning. However, pensions are becoming less common in the private sector, with many employers shifting to defined contribution plans like 401(k)s. For those with access to a pension, it remains a cornerstone of retirement security.

Beyond annuities and pensions, there are other retirement insurance plans worth exploring. Defined contribution plans, such as 401(k)s and IRAs, allow individuals to save and invest for retirement, with the eventual income depending on contributions and investment performance. These plans offer flexibility and tax advantages but require active management. Social Security is another form of retirement insurance, providing a government-backed income based on lifetime earnings. While not a complete solution on its own, Social Security supplements other retirement income sources. Additionally, longevity insurance is a specialized product that begins payouts at an advanced age, typically 80 or 85, to protect against outliving savings.

When choosing a retirement insurance plan, it’s essential to consider factors like financial goals, risk tolerance, and expected retirement lifestyle. Annuities and pensions offer guaranteed income, making them ideal for risk-averse individuals, while defined contribution plans and longevity insurance provide more flexibility and potential for growth. Combining multiple types of retirement insurance can create a diversified strategy, ensuring a steady and reliable income stream throughout retirement.

In conclusion, retirement insurance is a multifaceted tool for securing financial stability in later years. By exploring options like annuities, pensions, and other plans, individuals can tailor their retirement strategy to meet their unique needs. Understanding the features and benefits of each type of retirement insurance is the first step toward building a robust and reliable post-retirement income plan.

Insurance Simplified: A-Win's Comprehensive Coverage

You may want to see also

Explore related products

![]()

Eligibility Criteria: Understand age, employment, and contribution requirements to qualify for retirement insurance

Retirement insurance, often referred to as pension or retirement benefits, is a financial safety net designed to provide individuals with a steady income after they stop working. To qualify for these benefits, it’s crucial to understand the eligibility criteria, which typically revolve around age, employment history, and contribution requirements. These criteria ensure that the system remains sustainable and fair, providing support to those who have contributed adequately during their working years.

Age Requirements are a fundamental aspect of retirement insurance eligibility. Most countries and retirement programs specify a minimum retirement age, often ranging between 60 to 67 years, depending on the region and type of plan. Early retirement options may be available, but they usually come with reduced benefits. Conversely, delaying retirement beyond the standard age can sometimes increase the benefit amount. It’s essential to check the specific age requirements of your retirement insurance program, as these can vary based on factors like gender, occupation, and policy updates.

Employment History plays a critical role in determining eligibility for retirement insurance. Many programs require a minimum number of years of employment or participation in the workforce. For instance, Social Security in the United States mandates 40 credits, roughly equivalent to 10 years of work, to qualify for retirement benefits. Some systems also consider the nature of employment, with certain occupations or self-employed individuals having unique requirements. Continuous employment is not always necessary, but gaps in work history may affect the benefit amount or eligibility.

Contribution Requirements are another key factor in qualifying for retirement insurance. Most retirement programs are funded through payroll taxes, personal contributions, or a combination of both. For example, employees and employers in many countries contribute a percentage of earnings to a national pension fund. Self-employed individuals are typically responsible for making full contributions themselves. The total amount contributed and the consistency of these contributions often determine the benefit level. Some programs also require a minimum number of years of contributions to qualify for full benefits.

In addition to these core criteria, certain retirement insurance programs may have special provisions or exceptions. For example, individuals with disabilities or those who have worked in hazardous conditions might qualify for benefits at an earlier age or with fewer contributions. Similarly, survivors’ benefits may be available to spouses or dependents of deceased workers, regardless of their own contribution history. Understanding these nuances is essential to maximize your retirement insurance benefits.

Finally, it’s important to review and plan ahead to ensure eligibility for retirement insurance. Regularly check your contribution records, understand the rules of your specific program, and consider consulting a financial advisor or retirement specialist. Planning for retirement early allows you to address any gaps in contributions or employment history and make informed decisions about when and how to retire. By meeting the age, employment, and contribution requirements, you can secure a stable financial future during your retirement years.

Insurance Jobs: Recession-Proof or Not?

You may want to see also

Explore related products

![Pension coverage and vesting among private wage and salary workers, 1979 : preliminary estimates from the 1979 survey of pension plan coverage / Gayle Thompson Rogers. 1980 [Leather Bound]](https://m.media-amazon.com/images/I/61IX47b4r9L._AC_UY218_.jpg)

![]()

Benefits and Coverage: Learn about income replacement, healthcare, and survivor benefits offered by retirement insurance

Retirement insurance, often referred to as pension insurance or retirement income security, is a financial product designed to provide individuals with financial stability and peace of mind during their post-work years. One of its primary benefits is income replacement, which ensures that retirees continue to receive a steady stream of income after they stop working. This income is typically a percentage of their pre-retirement earnings, calculated based on factors such as years of service, salary history, and contributions to the plan. Income replacement helps retirees maintain their standard of living, cover daily expenses, and plan for long-term financial needs without relying solely on personal savings or government benefits.

Another critical aspect of retirement insurance is healthcare coverage. As individuals age, healthcare expenses often increase due to higher medical needs, chronic conditions, or long-term care requirements. Retirement insurance plans frequently include provisions for healthcare, either through direct coverage or by supplementing existing Medicare or private health insurance plans. This ensures that retirees have access to necessary medical services without facing overwhelming out-of-pocket costs. Some plans may also cover prescription medications, preventive care, and specialized treatments, providing comprehensive health security during retirement.

Survivor benefits are another essential component of retirement insurance, offering financial protection to the retiree's dependents or beneficiaries after their death. These benefits typically include a lump-sum payment or a continued stream of income to the surviving spouse, children, or other designated individuals. Survivor benefits help ensure that the retiree's family can maintain financial stability, cover immediate expenses, and plan for the future. This feature is particularly valuable for retirees who want to leave a financial legacy or provide for loved ones who may depend on their income.

In addition to these core benefits, retirement insurance often includes flexibility and customization to meet individual needs. Retirees can choose from various payout options, such as lifetime annuities, joint-and-survivor benefits, or lump-sum distributions, depending on their financial goals and circumstances. Some plans also offer cost-of-living adjustments (COLAs) to protect against inflation, ensuring that the retiree's income retains its purchasing power over time. This flexibility allows individuals to tailor their retirement insurance to align with their unique retirement plans and priorities.

Lastly, retirement insurance provides peace of mind by reducing financial uncertainty in later years. Knowing that income, healthcare, and survivor needs are covered allows retirees to focus on enjoying their retirement years without the stress of financial instability. It also complements other retirement savings vehicles, such as 401(k)s or IRAs, by providing a guaranteed income stream and additional protections. By understanding the benefits and coverage of retirement insurance, individuals can make informed decisions to secure a comfortable and worry-free retirement.

MetLife Annuity Contracts: Insurance for Life?

You may want to see also

Explore related products

$15.75

![]()

Cost and Premiums: Factors like age, health, and coverage level that determine retirement insurance costs

Retirement insurance, often referred to as pension insurance or annuities, is a financial product designed to provide individuals with a steady income stream during their retirement years. When considering retirement insurance, understanding the factors that influence its cost and premiums is crucial for making informed decisions. The primary determinants of these costs include age, health, and the level of coverage desired.

Age is one of the most significant factors affecting retirement insurance premiums. Generally, the younger you are when you purchase a retirement insurance policy, the lower your premiums will be. This is because insurers assume a longer period to accumulate funds and a lower immediate risk of payout. Conversely, purchasing retirement insurance at an older age typically results in higher premiums, as the insurer has less time to grow the investment and a higher likelihood of beginning payouts sooner. For example, a 30-year-old might pay significantly less for the same coverage compared to a 50-year-old due to the extended time horizon for investment growth.

Health also plays a critical role in determining retirement insurance costs. Insurers often assess an individual’s health status through medical underwriting to evaluate the risk of early or frequent claims. Individuals with pre-existing conditions or poor health may face higher premiums, as they are considered higher-risk clients. Conversely, those in good health may qualify for lower premiums due to the reduced likelihood of needing immediate or extensive benefits. Some policies may even offer discounted rates for individuals who meet certain health criteria, such as non-smokers or those with a healthy body mass index (BMI).

The coverage level selected directly impacts the cost of retirement insurance. Policies with higher monthly payouts or additional benefits, such as cost-of-living adjustments or survivor benefits, will naturally come with higher premiums. For instance, an annuity that guarantees a fixed income for life will typically cost more than one that provides income for a specified period. Similarly, adding features like inflation protection or spousal coverage increases the overall cost. It’s essential to balance the desired level of financial security with the affordability of premiums when choosing a coverage level.

Other factors, such as the type of retirement insurance product (e.g., fixed, variable, or indexed annuities) and the financial strength of the insurer, also influence costs. Fixed annuities, which offer guaranteed payouts, often have higher premiums due to the insurer’s obligation to provide consistent returns. Variable annuities, which allow for investment growth but carry market risks, may have lower base premiums but include additional fees for investment management. Additionally, insurers with higher credit ratings may charge more for their policies due to the perceived reliability and stability of their products.

In summary, the cost and premiums of retirement insurance are shaped by a combination of personal factors and policy choices. Age and health are key determinants, with younger, healthier individuals typically benefiting from lower costs. The desired coverage level, including payout amounts and additional benefits, directly affects premiums. Understanding these factors enables individuals to tailor their retirement insurance plans to their financial needs and circumstances, ensuring a secure and stable retirement income.

Are DJs Insured? Protecting Your Passion and Career

You may want to see also

Explore related products

![]()

Tax Implications: Discover how retirement insurance payouts and contributions affect your tax liabilities

Retirement insurance, often referred to as pension plans or annuities, is a financial product designed to provide individuals with a steady income stream during their retirement years. When considering retirement insurance, it’s crucial to understand its tax implications, as both contributions and payouts can significantly affect your tax liabilities. Contributions to certain types of retirement insurance plans, such as traditional Individual Retirement Accounts (IRAs) or employer-sponsored 401(k)s, are often tax-deductible. This means that the amount you contribute reduces your taxable income for the year, potentially lowering your overall tax burden. However, not all retirement insurance plans offer this benefit; for instance, contributions to Roth IRAs are made with after-tax dollars and do not provide an immediate tax deduction.

The tax treatment of retirement insurance payouts varies depending on the type of plan and how contributions were made. For traditional retirement plans, where contributions were tax-deductible, the payouts during retirement are taxed as ordinary income. This is because the government deferred taxes on the contributions and investment growth, so withdrawals are subject to taxation. On the other hand, Roth retirement plans, funded with after-tax dollars, offer tax-free payouts in retirement, provided certain conditions, such as age and account holding period, are met. Understanding these differences is essential for planning your retirement income and managing your tax liabilities effectively.

Another important tax consideration is the timing of withdrawals. Early withdrawals from retirement insurance plans, typically before age 59½, often incur penalties in addition to income taxes. For example, traditional IRA withdrawals before this age may be subject to a 10% early withdrawal penalty, plus ordinary income tax. Roth IRAs, however, allow penalty-free withdrawals of contributions (not earnings) at any time, offering more flexibility in certain situations. Planning withdrawals strategically can help minimize taxes and penalties, ensuring that your retirement savings last longer.

Required Minimum Distributions (RMDs) are another tax-related aspect of retirement insurance that retirees must be aware of. For traditional retirement accounts, the IRS mandates that account holders begin taking minimum distributions by April 1 of the year following the year they turn 73 (as of recent regulations). Failure to take RMDs results in a 50% penalty on the amount not distributed, in addition to regular income tax. Roth IRAs, however, do not require RMDs during the account owner’s lifetime, providing more control over tax planning in retirement.

Lastly, the impact of retirement insurance on your overall tax strategy extends beyond individual contributions and withdrawals. For example, large payouts from retirement plans can push you into a higher tax bracket, increasing your tax liability. Additionally, retirement income, including Social Security benefits and pension payouts, may be subject to taxation depending on your total income. Coordinating withdrawals from taxable, tax-deferred, and tax-free accounts can help optimize your tax situation in retirement. Consulting a financial advisor or tax professional can provide personalized guidance to navigate these complexities and maximize the after-tax value of your retirement insurance.

Life Insurance Simplified: Direct Term Coverage Explained

You may want to see also

Frequently asked questions

Retirement insurance, also known as pension insurance or retirement income protection, is a financial product designed to provide individuals with a steady income stream after they retire. It ensures financial security by replacing a portion of pre-retirement income, often through annuities, pensions, or other structured plans.

Retirement insurance differs from traditional savings plans like 401(k)s or IRAs because it guarantees a fixed income for life, regardless of market fluctuations. While savings plans rely on investments and contributions, retirement insurance focuses on providing predictable, stable payouts during retirement.

Eligibility for retirement insurance varies by provider and plan, but it is generally available to individuals nearing retirement age. It’s advisable to consider retirement insurance if you want guaranteed income, are concerned about outliving your savings, or prefer a predictable financial plan for your later years.