Ridesharing, or ride-hailing, is a convenient and budget-friendly way to travel on short notice. The two biggest ridesharing companies are Uber and Lyft, which connect riders with private citizens who drive them to their destinations. Ridesharing drivers use their own vehicles and rely on smartphone apps to accept fares, which has been criticized for encouraging distracted driving. Ridesharing insurance is extra coverage for people who drive for app-based ride-hailing or delivery services, and it is important to understand the differences between personal insurance and ridesharing insurance.

| Characteristics | Values |

|---|---|

| What is ridesharing insurance? | Insurance for those who drive their car for a ride-hailing or delivery service app. |

| Who needs ridesharing insurance? | Those who drive their car to earn money. |

| What does ridesharing insurance cover? | Injuries or damage to others or their property while ridesharing. |

| What does ridesharing insurance not cover? | Damage to your car from an accident unless your personal policy includes comprehensive and collision insurance. |

| How do I get a quote for ridesharing insurance? | Contact an insurance company directly, or use an independent agent to find an insurer. |

| How much does ridesharing insurance cost? | Adding ridesharing coverage can cost a few extra dollars a month, but this varies by driver, state, and insurance company. |

Explore related products

What You'll Learn

![]()

Gaps in personal insurance policies

Ridesharing insurance, also known as a commercial policy, is a type of insurance that fills the gaps in coverage between your personal insurance policy and the insurance provided by the ride-hailing or delivery company you work for. This type of insurance is necessary if you use your car for a ride-hailing or delivery service app, such as Uber, Lyft, Uber Eats, or DoorDash.

While ridesharing companies do provide some insurance for their drivers, there may be limitations to their policies. For example, you may not be covered while waiting for a ride request or when you have a passenger in your vehicle. This is where ridesharing insurance comes into play, as it provides additional coverage to fill these gaps.

One gap in personal insurance policies is the lack of coverage while waiting for a ride request. During this time, you may not be covered by your personal policy or the ridesharing company's policy, leaving you vulnerable in the event of an accident. Ridesharing insurance can fill this gap by providing coverage from the moment you turn on the app to when you accept a ride request.

Another gap in personal insurance policies is the limited coverage for damage to your vehicle. While ridesharing companies may offer liability coverage for injuries or damage caused to others, they may not cover damage to your car. If your personal policy does not include comprehensive and collision insurance, also known as full coverage, you may have to pay for repairs out of pocket. Ridesharing insurance can provide additional coverage for damage to your vehicle, giving you peace of mind.

Additionally, personal insurance policies may not cover the deductible required by ridesharing companies. When you get into an accident while ridesharing, you may be responsible for paying the ridesharing company's deductible, which can be quite high. Ridesharing insurance can help reimburse the difference between the ridesharing company's deductible and your personal policy's deductible, reducing your out-of-pocket expenses.

Lastly, personal insurance policies may not cover you if you rent out your car through platforms like Turo. In this case, you would need to purchase a separate commercial policy or Turo car insurance. It's important to carefully review the policies of both your personal insurance and the ridesharing company to identify any gaps in coverage and ensure you have the necessary protection.

Participating Policies: Stock Insurers' Unique Offering

You may want to see also

Explore related products

![]()

Additional protection for ridesharing

If you drive your car for a ride-hailing or delivery service app, you will need rideshare insurance or a commercial policy. Rideshare insurance fills the gaps in coverage between your personal policy and any insurance the ride-hailing or on-demand delivery company offers.

Rideshare coverage protects you and your vehicle if you drive for a ridesharing service such as Uber and Lyft. While ridesharing companies may provide some insurance that applies to drivers operating on their platforms, their coverage may be limited while you're waiting to match with a rider or when you have a passenger in your vehicle.

Uber, for example, maintains commercial auto insurance on your behalf for ridesharing and delivery activities when you're driving on their platform. When you're not driving with Uber, you maintain your own personal auto insurance. Many personal auto insurers offer additional insurance for rideshare or delivery drivers, but this is not required for you to sign up to drive with Uber.

If you plan to operate on Uber, Lyft, or any ridesharing platform as a driver, you can add rideshare coverage to your personal auto insurance policy. This will protect you as soon as you start working. By adding rideshare coverage, you can gain protection beyond what's provided by your ridesharing company's insurance policy.

In most states, rideshare insurance covers drivers who operate on delivery service platforms like Uber Eats or DoorDash. The exact coverages that apply between your personal auto policy with rideshare insurance and any insurance provided through the delivery company may vary by state.

CMS vs Private Insurers: ACO Public Option Explored

You may want to see also

Explore related products

![]()

Uber and Lyft insurance coverage

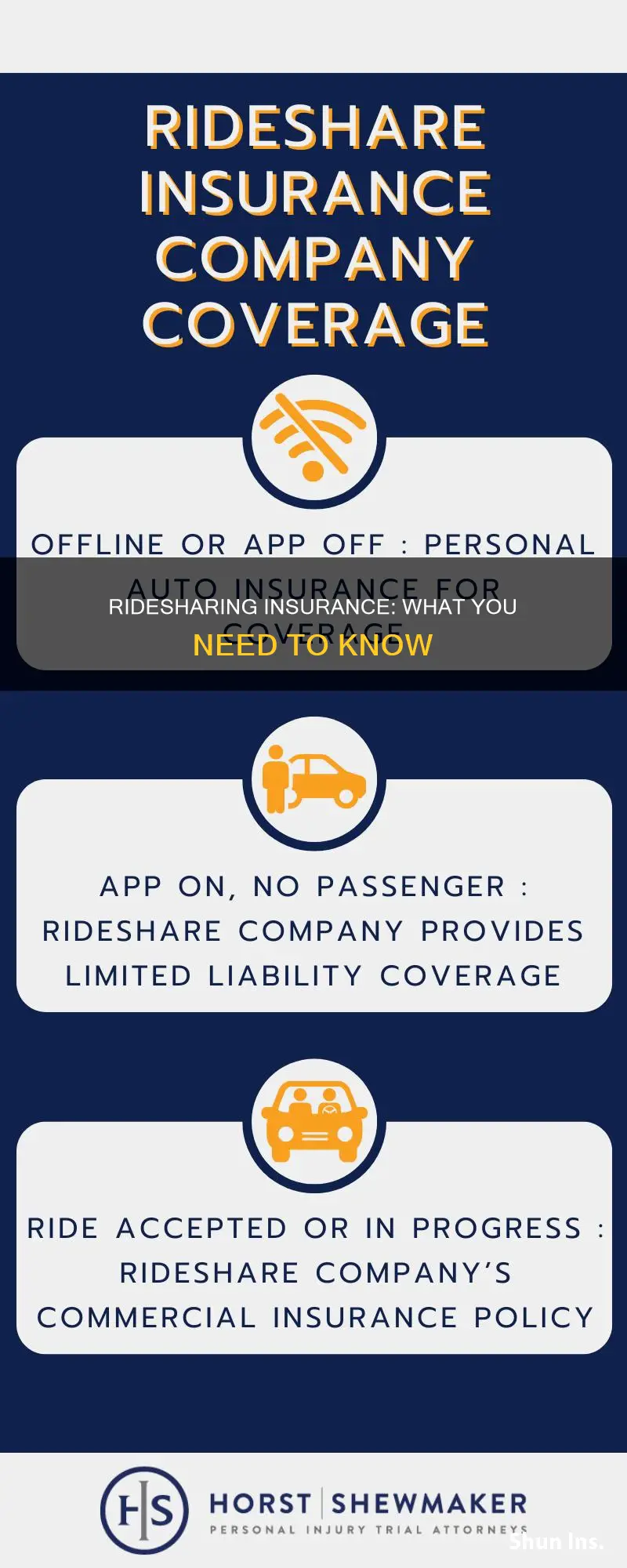

Ridesharing insurance is a type of commercial insurance that covers drivers who work for ride-hailing or delivery service apps. Uber and Lyft, two popular ridesharing companies, offer their drivers rideshare insurance under a commercial insurance policy. This insurance covers any accidents that occur while the driver is "on duty", which is divided into several periods.

Period 1 involves the driver having the rideshare app open and looking for passengers. During this time, Uber and Lyft provide liability coverage for any accident that is the fault of the driver, covering up to $50,000 per person injured, $100,000 total injury liability per accident, and $25,000 property damage liability. This liability coverage only covers damages sustained by others and does not include injuries to the driver or damage to their property.

Period 2 begins when the driver has been matched with a rider and is en route to pick them up. Period 3 starts when the rider enters the car and ends when they exit. If an accident occurs during these two periods, Uber and Lyft provide liability coverage of up to $1 million for injuries and property damage sustained by a rideshare customer or anyone hit by an Uber or Lyft vehicle at the fault of the rideshare driver. This coverage also applies if an uninsured or underinsured driver is involved in the accident.

It is important to note that Uber and Lyft do not classify their drivers as employees but rather as independent contractors. As such, drivers may need to purchase additional rideshare insurance to fill any gaps in coverage provided by the companies. This insurance can be added to a personal auto policy or obtained as a separate commercial policy. It is recommended that drivers understand the insurance coverage provided by the rideshare companies and how it interacts with their personal auto insurance policy to ensure adequate protection.

In summary, Uber and Lyft provide liability coverage for their drivers while they are on duty, with varying limits depending on the period of the trip. However, additional rideshare insurance may be necessary to ensure comprehensive protection for both the driver and their vehicle.

AOK Private Insurance: What You Need to Know

You may want to see also

Explore related products

![]()

Commercial auto policies

If you are a driver for a ridesharing company, such as Uber or Lyft, you may need to consider a commercial auto policy. While ridesharing companies do provide some insurance for their drivers, this coverage may be limited to certain periods, such as when a passenger is in the car. This means that you could be at risk of liability if you get into an accident while waiting for a ride request.

Rideshare insurance is designed to fill in these coverage gaps and protect you and your vehicle when driving for a ridesharing service. This insurance can be added as an endorsement to your personal auto policy, but it is not available in all states. If you are unable to add rideshare insurance to your personal policy, you may need to purchase a commercial auto policy.

It is important to note that the specific coverages and exclusions of a commercial auto policy may vary depending on the insurance company and the state in which you are located. Additionally, some states and ridesharing services may require you to purchase a commercial policy to ensure adequate coverage. Therefore, it is recommended to contact your insurance provider and inquire about the specific details of their commercial auto policies and how they apply to ridesharing activities.

Overall, if you are a ridesharing driver, it is crucial to understand the insurance implications and ensure that you have the necessary coverage to protect yourself, your vehicle, and your passengers in the event of an accident.

ACA's Impact on Texas Private Insurance: What's Changed?

You may want to see also

Explore related products

![]()

Ridesharing insurance availability

Ridesharing insurance is an additional coverage option that can be added to your personal auto insurance policy. It is designed to fill in the gaps in coverage that may exist when driving for a ride-hailing or delivery service. While some insurance companies may refer to this type of insurance as a "ridesharing endorsement", others may simply include it as part of their standard personal auto insurance policy.

The availability of ridesharing insurance can vary depending on your location and the insurance company you choose. Some companies, such as Progressive, offer ridesharing insurance as an add-on to your personal auto policy in most states. They also provide the option of obtaining a commercial auto policy if a ridesharing endorsement is not available in your state. It is important to note that adding ridesharing coverage will increase the price of your personal auto policy.

If your current insurance company does not offer ridesharing insurance, you may need to switch to a different provider. It is recommended to compare quotes and coverage options from multiple companies, including large and small insurers, to find the best option for your needs. Working with an independent agent can also be helpful in finding insurers that offer ridesharing insurance in your area.

Additionally, it is crucial to understand the limitations of ridesharing insurance. While it provides coverage during periods when you are waiting to be matched with a rider or when you have a passenger in your vehicle, there may still be gaps in coverage. For example, damage to your car from an accident while ridesharing may only be covered if your personal policy includes comprehensive and collision insurance, and you may need to pay a deductible before the ridesharing company's insurance pays out.

Before engaging in ridesharing activities, it is essential to contact your insurer and understand the terms of your policy. Some insurance companies may cancel or non-renew your policy if they find out you are driving for a ridesharing service without their knowledge. It is also important to review the insurance provided by the ridesharing company, as their coverage may vary depending on the situation and may not cover all liabilities.

Understanding HMO and PPO: Private Insurance Options

You may want to see also

Frequently asked questions

Ridesharing insurance is an add-on to your personal auto policy that fills in the gaps in coverage between your personal policy and the limited protection from ridesharing companies.

Driving for a ridesharing company without a proper insurance policy could leave you at risk for any potential damages and could lead to your coverage being dropped altogether.

Ridesharing insurance covers damage to your car from an accident while ridesharing. It also covers injuries or damage you may cause to others or their property while ridesharing.

You can get a quote for ridesharing insurance by contacting an insurance company that offers this type of coverage, such as Progressive, State Farm, or The Zebra.