Homeowners insurance is a type of insurance that provides coverage for your home and personal property in the case of a covered loss. It can also provide liability coverage if an accident or injury occurs in your home or on your property. There are eight types of homeowners insurance policies, with HO-3 being the most common. This type of policy, also known as special form coverage, offers suitable coverage for most homeowners. It covers your house and belongings and includes coverage for liability, medical payments to others, and additional living expenses.

| Characteristics | Values |

|---|---|

| Purpose | To provide financial protection against loss due to disasters, theft and accidents. |

| Coverage | Structure of the home, personal belongings, liability protection, additional living expenses, medical payments to others, etc. |

| Types | HO-1, HO-2, HO-3, HO-4, HO-5, HO-6, HO-7, HO-8. |

| Exclusions | Earthquakes, floods, damage or theft in unoccupied homes, etc. |

| Add-ons | Valuable items, such as jewelry or collectibles. |

Explore related products

$14.37 $24.99

What You'll Learn

- Homeowners insurance provides financial protection against loss due to disasters, theft and accidents

- There are eight types of homeowners insurance policies, including HO-1, HO-2, HO-3, and HO-5

- HO-3 is the most common type of homeowners insurance and covers your house, belongings, liability, medical payments and additional living expenses

- HO-5 offers the most protection and is suitable for those with high-value personal property

- Additional living expense (ALE) coverage helps with the costs of hotel bills, meals and other living expenses if your home is uninhabitable

![]()

Homeowners insurance provides financial protection against loss due to disasters, theft and accidents

Homeowners insurance is a form of property insurance that covers losses and damages to your residence, along with furnishings and other assets in the home. It provides financial protection against loss due to disasters, theft, and accidents. It is not a legal requirement in any of the 50 states or Washington, D.C., but it is usually a prerequisite for getting a mortgage.

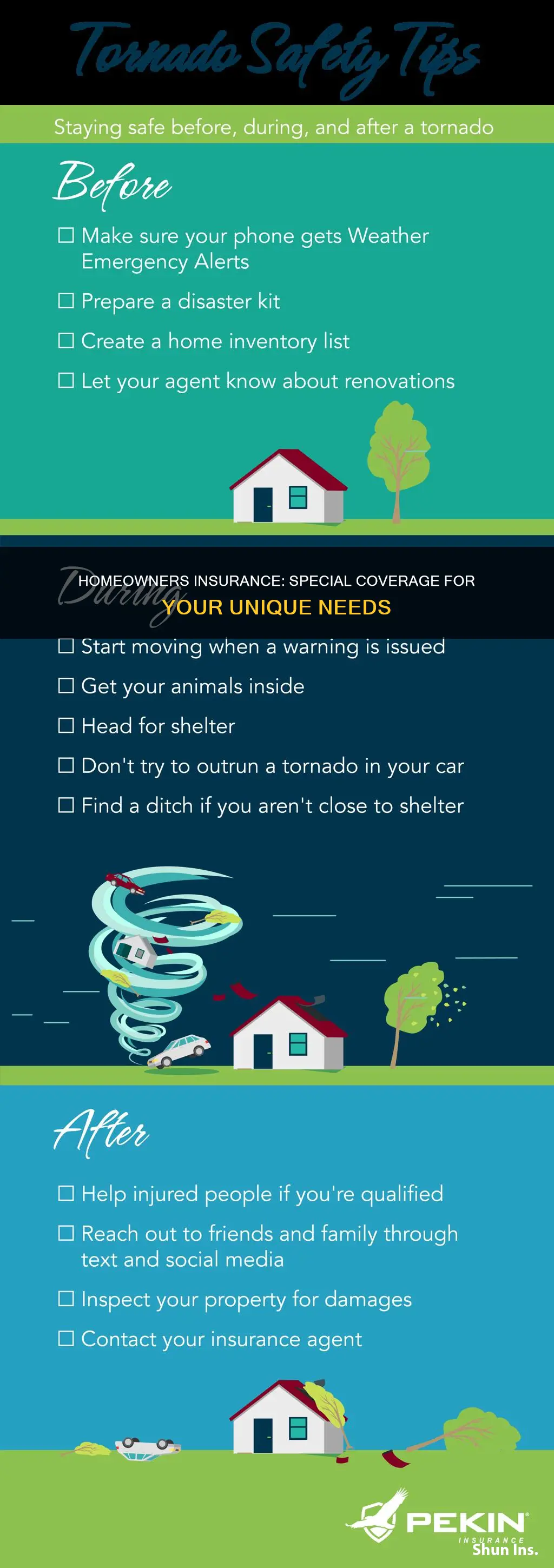

Homeowners insurance covers a variety of damages to your home and other assets at your residence. It pays to repair or replace damaged property, including your belongings and the structure of your house. Most basic homeowners insurance policies cover events such as hurricanes, tornadoes, and fires. They also cover your liability if you hurt someone else or damage their property.

However, it is important to note that standard policies do not cover damage caused by floods, earthquakes, or routine wear and tear. If you live in an area prone to natural disasters, you may need special coverage to insure your property against floods or earthquakes. You can purchase supplemental flood insurance at an additional cost.

Homeowners insurance premiums are highly individualized and depend on various factors, including location, coverage limits, credit score, insurance company, and state regulations. When purchasing homeowners insurance, it is important to carefully review the policy and understand what is covered and what is excluded.

Nest Homeowners: Insurance Partners for Smart Homes

You may want to see also

Explore related products

![]()

There are eight types of homeowners insurance policies, including HO-1, HO-2, HO-3, and HO-5

Homeowners insurance is a type of insurance that provides coverage for your home and personal property in the case of a covered loss. It can also provide liability coverage if an accident or injury occurs in your home or on your property. There are eight types of homeowners insurance policies, including HO-1, HO-2, HO-3, and HO-5. These policies differ in the level of protection they offer and the types of properties they cater to.

HO-1 policies are the most basic type of homeowners insurance. They offer limited coverage and are not available in most states. HO-1 policies protect your home's structure against specified perils, such as fire, lightning, windstorms, and hail, but they do not include liability or personal property coverage. Many mortgage companies do not accept HO-1 policies as proof of home insurance.

HO-2 policies, also known as broad form homeowners insurance, offer coverage for a broader range of perils compared to HO-1. In addition to the perils covered by HO-1, HO-2 includes protection against falling objects, certain sudden or accidental damage, and the weight of ice, snow, or sleet. HO-2 policies cover your home at its replacement cost and your personal property at its actual cash value.

HO-3 is the most common type of homeowners insurance and is also known as special form coverage. HO-3 offers more expansive coverage than HO-2, safeguarding your home's structure against all perils except those specifically excluded, such as earthquakes and floods. HO-3 also provides protection against damage to your belongings from named perils and includes personal liability coverage.

HO-5 policies offer the highest level of protection among all types of homeowners insurance. They provide coverage for your home's structure and your personal belongings against any peril that is not explicitly excluded. HO-5 policies have higher coverage limits and fewer restrictions, making them ideal for those with high-value personal property or those seeking maximum coverage.

Other types of homeowners insurance policies include HO-4, which is designed for renters, and HO-6, which is for condo owners. HO-7 policies protect mobile or manufactured homes, while HO-8 insurance is for older properties, typically built more than 40 years ago.

RV Gap Insurance: Is It Worth the Extra Cost?

You may want to see also

Explore related products

![]()

HO-3 is the most common type of homeowners insurance and covers your house, belongings, liability, medical payments and additional living expenses

HO-3 is the most common type of homeowners insurance, offering a comprehensive package that covers your house, belongings, liability, medical payments, and additional living expenses. It is ideal for the average homeowner, providing a balance of reliable and affordable coverage against a broad range of risks.

HO-3 insurance policies typically include six types of coverage. Firstly, dwelling coverage pays for repairs to the structure of your home and any attached structures, like a porch or garage. Secondly, other structures coverage insures any detached buildings, such as garages, driveways, sheds, and fences. Thirdly, personal property coverage helps protect your possessions, including clothing and furniture, from damage or theft. Fourthly, personal liability coverage safeguards you financially if you or a family member are held responsible for someone else's injuries or property damage. Fifthly, guest medical payments coverage contributes to a guest's medical expenses if they are injured on your property, regardless of negligence. Lastly, additional living expenses cover temporary relocation costs, such as hotel stays and meals, if your home becomes uninhabitable due to a covered peril.

The specific details of HO-3 policies can vary, and additional coverage may be required depending on your location. For example, in areas prone to earthquakes or floods, separate insurance for these events may be necessary. HO-3 policies are typically written on an open-perils basis for the home and other structures, meaning any peril not explicitly excluded is covered. In contrast, personal property protection is often based on a named-perils list, specifying the covered risks.

HO-3 insurance is widely applicable to owner-occupied single-family homes and townhouses. It is designed to provide financial assistance in various scenarios, including repairing or rebuilding your home and other structures, replacing stolen or damaged belongings, covering living expenses during displacement, and paying legal fees if you are sued for injuries or property damage. While HO-3 is the most prevalent type of homeowners insurance, other options, such as HO-1, HO-2, and HO-5, offer varying levels of coverage depending on individual needs and home characteristics.

Pet Insurance: Worth the Cost?

You may want to see also

Explore related products

![]()

HO-5 offers the most protection and is suitable for those with high-value personal property

HO-5 insurance is a type of homeowners insurance that provides the most comprehensive coverage for your home and personal belongings. It is an open-peril policy, meaning it covers any scenario that is not specifically excluded in the policy. This includes damage to your home's structure, foundation, and roof, as well as any other structures on your property that are not connected to your dwelling. It also covers your personal property at full replacement cost, meaning you will receive enough money to purchase a brand-new item.

The HO-5 policy is suitable for those with high-value personal property as it offers higher coverage limits and fewer restrictions on perils. For example, if you need to make a claim for a five-year-old laptop that you bought for $1,000, an HO-3 policy would consider the depreciated cost after five years, which could be around $500 or less. In contrast, an HO-5 policy would reimburse you for the full cost of replacing your laptop at today's value, so you could receive $1,000 to buy a brand new laptop.

HO-5 insurance also provides coverage for liability, including any medical expenses for guests who are injured on your property or by you off of your property. It also includes loss of use coverage, which reimburses you for any expenses incurred while you cannot reside in your home due to a covered reason.

It is important to note that eligibility for HO-5 insurance depends on factors such as the condition and location of the property, as well as the homeowner's claims history. Generally, HO-5 insurance is available to homeowners who own newer or well-maintained homes in areas considered low risk for natural disasters and other potential threats.

To further personalize your HO-5 insurance, you can purchase additional policies or endorsements, such as sewer and water backup coverage, identity theft coverage, earthquake insurance, and personal property replacement coverage.

Chubb Home Insurance: Is It Worth the Cost?

You may want to see also

Explore related products

![]()

Additional living expense (ALE) coverage helps with the costs of hotel bills, meals and other living expenses if your home is uninhabitable

Homeowners insurance is a form of property insurance that covers losses and damages to your residence, as well as furnishings and other assets in the home. It is not a legal requirement, but if you have a mortgage, your lender will likely require you to insure the home to protect its investment.

Special homeowners insurance is necessary if you live in an area prone to natural disasters, such as earthquakes or floods, which are typically excluded from standard policies.

Additional living expense (ALE) coverage is a standard part of a home insurance policy that helps with the costs of hotel bills, meals, and other living expenses if your home is uninhabitable. This includes the costs of doing laundry, transportation, and lost rental income. ALE covers the difference between your everyday living expenses and these additional costs. For example, if your everyday living expenses for three months are $8,500, and your living expenses while your home is uninhabitable for the same period are $12,000, your ALE claim would be $3,500.

ALE coverage is intended to cover the extra expenses incurred as a result of being temporarily displaced from your home. It is important to note that ALE only applies to a covered loss, meaning the damage must be due to a peril outlined in your policy, such as fire, windstorm, or water damage from a burst pipe. It does not cover all expenses, only those deemed necessary to maintain your standard of living.

To make a claim, it is crucial to keep receipts and documentation for all ALE expenses. These documents are necessary for filing a claim and ensuring you receive the appropriate reimbursement.

ATV Insurance: Is It Worth the Cost?

You may want to see also

Frequently asked questions

Homeowners insurance is a type of insurance that provides financial protection against loss due to disasters, theft and accidents. It covers your home and personal property in the case of a covered loss.

There are eight types of homeowners insurance policies: HO-1, HO-2, HO-3, HO-4, HO-5, HO-6, HO-7, and HO-8. The most common type is HO-3, which covers your house and belongings and includes liability, medical payments to others, and additional living expenses.

HO-3 policies cover your home and belongings against all perils unless they are specifically listed as exclusions. This includes damage to the structure of your home and your personal property.

Homeowners insurance typically does not cover damage caused by floods, earthquakes, or routine wear and tear. Some policies may also exclude government actions, legal action due to lack of permits, and damage to unoccupied homes.