Straight life insurance, also known as whole life insurance, is a type of life insurance that lasts your entire lifetime as long as premiums are paid. It differs from term life insurance, which has level premiums and a level death benefit but only lasts for a certain length of time, usually between 10 and 30 years. Straight life insurance offers the opportunity to build cash value over time, similar to a savings account.

| Characteristics | Values |

|---|---|

| Type | Whole life insurance |

| Duration | Lasts your entire lifetime as long as premiums are paid |

| Benefits | Can be used throughout your life |

| Cost | More expensive than term life insurance |

| Cash value | Opportunity to build cash value, similar to a savings account |

| Premiums | Level premiums paid until death or until the policy is considered paid in full |

| Death benefit | Paid to chosen beneficiary or beneficiaries after death |

Explore related products

![]()

Whole life insurance

Straight life insurance is more commonly known as whole life insurance. It is a type of life insurance that lasts your entire lifetime, as long as the premiums are paid. Whole life insurance is typically more expensive than term life insurance, but it offers the opportunity to build cash value, similar to a savings account.

Life Insurance Loan Proceeds: Taxable or Not?

You may want to see also

Explore related products

![]()

Level premiums

Straight life insurance, also known as whole life insurance, is a type of insurance that lasts your entire lifetime as long as premiums are paid. It offers a level death benefit and level premiums for as long as the insured person lives and premiums are paid on time. This differs from term life insurance, which has level premiums and a level death benefit but only lasts for a certain length of time, usually between 10 and 30 years.

The level premiums are calculated based on various factors, including the insured person's age, health status, and life expectancy at the time of purchasing the policy. The insurance company will assess these factors and determine a premium amount that remains constant over the years. This means that the insured person knows exactly how much they need to budget for their life insurance each month or year.

It is important to note that the level premiums must be paid consistently and on time to keep the policy active. If payments are missed or delayed, the policy may lapse, and the insurance coverage may be terminated. Therefore, it is crucial for policyholders to prioritise timely payment of the level premiums to maintain their straight life insurance coverage.

Straight life insurance policies with level premiums offer several advantages. Firstly, they provide lifelong coverage, ensuring peace of mind that beneficiaries will receive a death benefit regardless of when the insured person passes away. Secondly, these policies can build cash value over time. A portion of each premium payment goes towards maintaining the policy, while the rest accumulates in a cash value account, similar to a savings account. This cash value can be accessed or borrowed against during the insured person's lifetime, providing additional financial flexibility.

Heart Disease and Afib: Impact on Life Insurance

You may want to see also

Explore related products

![]()

Death benefits

Straight life insurance, also known as whole life insurance, provides a level death benefit and premiums for as long as the insured person lives and premiums are paid on time. This means that the policyholder's beneficiaries will receive a death benefit amount when the policyholder passes away, as long as the premiums have been paid up to that point. This differs from term life insurance, which only lasts for a certain length of time, usually between 10 and 30 years, and provides a level death benefit and premiums for that fixed term.

Straight life insurance policies can also build cash value over time, similar to a savings account. Every time a premium is paid, a portion goes towards maintaining the life insurance policy, and the rest goes to the cash value account. This cash value can be accessed during the policyholder's lifetime and can be used for various purposes, such as supplementing retirement income or covering unexpected expenses.

The death benefit provided by straight life insurance can be a significant source of financial support for the policyholder's loved ones after their death. It can help cover funeral and burial expenses, pay off any outstanding debts, or provide ongoing financial support for dependents, such as a spouse or children. The death benefit amount can be customized according to the policyholder's needs and financial goals, ensuring that their beneficiaries receive the desired level of financial protection.

Additionally, straight life insurance policies typically offer the option to choose between a lump-sum payout or an annuity payout for the death benefit. A lump-sum payout provides the entire death benefit amount in a single payment, while an annuity payout distributes the benefit over a specified period, often with interest. The choice between these payout options depends on the policyholder's preferences and the financial needs of their beneficiaries.

Gerber Life Insurance: Cash Availability and Accessibility

You may want to see also

Explore related products

![Life and Health Insurance Study Cards: Life Health Insurance License Exam Prep with Practice Test Questions [Full Color]](https://m.media-amazon.com/images/I/51Pox87Z5lL._AC_UL320_.jpg)

![]()

Cash value

Straight life insurance, also known as whole life insurance, offers lifelong coverage and the opportunity to build cash value. This is similar to a savings account, with a portion of each premium going towards maintaining the life insurance policy and the rest going to the cash value account.

Straight life insurance policies have level premiums that are paid until death or until the policy is considered paid in full. Once the insured person passes away, the death benefit amount is paid to their chosen beneficiary or beneficiaries.

The cash value of a straight life insurance policy can be a useful feature for those looking to build savings over time. It is important to note that the cash value account is separate from the death benefit, and the funds in the account can be accessed by the policyholder during their lifetime.

While straight life insurance typically offers more benefits than term life insurance, it is usually more expensive. Term life insurance provides temporary coverage with level premiums and a level death benefit for a fixed term, usually between 10 and 30 years.

Overall, straight life insurance can be a valuable option for those seeking lifelong coverage and the opportunity to build cash value over time. The cash value feature provides flexibility and can be a useful addition to the death benefit provided by the policy.

Life Insurance Licenses: California's Comprehensive Credentials

You may want to see also

Explore related products

![]()

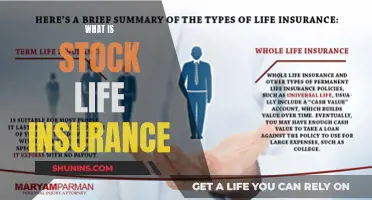

Term life insurance

Straight life insurance is more commonly known as whole life insurance. It offers lifelong coverage and is typically more expensive than term life insurance. Term life insurance provides temporary coverage, usually for a fixed period of 10 to 30 years, although some companies offer coverage for as little as five years or as much as 40 years.

One advantage of term life insurance is that it is generally more affordable than straight life insurance. This is because the coverage is only for a limited period, and the premiums are fixed for that term. On the other hand, straight life insurance premiums are typically higher because they are guaranteed to remain in force for the insured's entire lifetime, provided the required premiums are paid.

Another difference between the two types of insurance is that straight life insurance offers the opportunity to build cash value over time. This means that a portion of the premium paid goes towards maintaining the life insurance policy, while the rest goes into a cash value account. Term life insurance, on the other hand, does not offer this feature.

Group Life Insurance Calculation: Understanding the Premium Formula

You may want to see also

Frequently asked questions

Straight life insurance is a type of whole life insurance. It lasts your entire lifetime as long as premiums are paid.

Straight life insurance offers lifelong coverage, whereas term life insurance provides temporary coverage, usually for 10 to 30 years. Straight life insurance also offers the opportunity to build cash value over time, similar to a savings account.

The death benefit amount is paid to the chosen beneficiary or beneficiaries.