Medicare Supplement Insurance, also known as Medigap, is an additional insurance plan that covers costs that Original Medicare (Part A and Part B) does not. It is available to those aged 65 or older, or to those under 65 who are eligible for Medicare due to disability. It is important to note that Medicare Supplement Insurance is different from Medicare Advantage, and one cannot have both at the same time. There are up to 10 Medicare Supplement plans offered in each state, ranging from basic to extensive coverage.

| Characteristics | Values |

|---|---|

| Name | Medicare Supplement Insurance (Medigap) |

| Type | Private health insurance |

| Purpose | Helps pay for out-of-pocket costs not covered by Original Medicare (Part A and B) |

| Coverage | Up to 20% of Medicare expenses that Original Medicare doesn't cover |

| Eligibility | Available to individuals aged 65 or older, or younger than 65 with a disability |

| Enrollment | Can be applied for any time during the year, with a guaranteed 6-month open enrollment period for those aged 65 or older |

| Plans | Up to 10 plans offered in each state, ranging from basic to extensive coverage |

| Providers | Various insurance companies, including Cigna and UnitedHealthcare |

Explore related products

$19.95 $9.07

What You'll Learn

![]()

Medicare Supplement Insurance (Medigap)

Medicare Supplement Insurance, also known as Medigap, is extra insurance that adds on to Original Medicare (Part A and Part B). It helps cover out-of-pocket costs that Original Medicare does not, which can be substantial, as Medicare covers around 80% of healthcare costs. Medigap is provided by private health insurance companies and helps pay for about 20% of the expenses that Original Medicare doesn't cover.

Medigap policies are available to those aged 65 or older who are enrolled in Original Medicare Part A and Part B. Additionally, Medigap plans are also available to those under 65 who are eligible for Medicare due to disability or End-Stage Renal Disease. The best time to enroll is during the six-month Medigap Open Enrollment period, which begins on the first day of the month in which you turn 65 and are enrolled in Medicare Part B. Some states may have additional open enrollment periods, and you can apply for a Medigap plan at any time during the year. However, if you apply outside of your Open Enrollment period, you may be underwritten and not accepted into the plan.

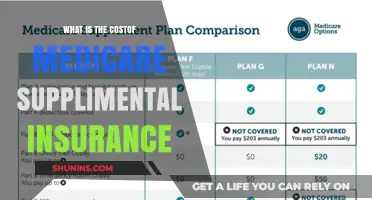

There are up to 10 Medigap plans offered in each state, ranging from basic to extensive coverage. The types of plans offered differ depending on the state, but each policy is standardized and offers the same basic benefits. The different types of plans are named alphabetically, from Plan A to Plan N. Medigap policies can be purchased separately, and they work with standalone Part D Prescription Drug plans as well.

Medigap is different from Medicare Advantage, and you can have either a Medicare Advantage Plan or a Medigap Plan, but not both simultaneously. It is important to understand your healthcare needs and financial situation when choosing a Medigap plan.

Understanding Adjusted Gross Income Brackets for Medical Insurance

You may want to see also

Explore related products

![]()

What does Medicare Supplement Insurance cover?

Medicare Supplement Insurance, also known as Medigap, is extra insurance that covers costs that Original Medicare (Part A and B) does not. Medigap helps pay for about 20% of the expenses that Original Medicare does not cover, which can be significant for large medical bills.

Medigap covers costs such as copayments, coinsurance, and deductibles. It can also cover other costs, depending on the specific plan chosen. There are up to 10 Medigap plans offered in each state, ranging from basic to extensive coverage. The types of plans offered differ by state, but each policy is standardized with the same basic benefits. Plans are typically named alphabetically, from Plan A to Plan N.

To be eligible for Medigap, individuals must be enrolled in both Original Medicare Part A and Part B. Generally, individuals must be 65 or older to be eligible for Medicare Supplement Insurance. However, in some states, plans may be available to persons under 65 who are eligible for Medicare due to disability or End-Stage Renal Disease.

The best time to enroll in a Medicare Supplement Insurance plan is during the six-month open enrollment period that begins when an individual turns 65 and is enrolled in Medicare Part B. Individuals can also apply for a plan at any time during the year.

Scarsdale Medical: Understanding Insurance Coverage and Your Options

You may want to see also

Explore related products

![]()

Who can apply for Medicare Supplement Insurance?

Medicare Supplement Insurance, also known as Medigap, is an additional insurance plan that can be purchased to cover healthcare costs not included in Original Medicare, such as copays, coinsurance, and deductibles. It is important to note that Medicare Supplement Insurance is not a substitute for Original Medicare but rather a supplement to it.

To be eligible to apply for Medicare Supplement Insurance, individuals must be enrolled in Original Medicare, specifically Part A (Hospital Insurance) and Part B (Medical Insurance). This is a crucial requirement, as Medigap is designed to fill the gaps in coverage provided by Original Medicare.

The best time to enrol in Medicare Supplement Insurance is during the open enrolment period, which is a six-month period that starts the first day of the month in which an individual turns 65 or older and is enrolled in Medicare Part B. This open enrolment period may vary depending on the state, and some states may offer additional open enrolment periods for individuals under 65 who are eligible for Medicare due to disability or End-Stage Renal Disease.

It is important to note that Medicare Supplement Insurance plans are standardized and regulated by the federal government and, in the case of California, by the California Department of Insurance (CDI). These plans are sold by private insurance companies, and individuals can choose the company and plan that best suits their needs.

Utah Hospital: What Medical Insurance is Offered?

You may want to see also

Explore related products

![]()

When to apply for Medicare Supplement Insurance

Medicare Supplement Insurance, also known as Medigap, is an additional insurance policy that can be purchased from a private health insurance company. It helps cover some of the out-of-pocket costs that Original Medicare (Parts A and B) does not cover. While it is not a requirement, many people choose to enrol in a Medicare Supplement plan to enhance their healthcare coverage.

So, when is the best time to apply for Medicare Supplement Insurance? Here is a detailed guide to help you navigate the process:

Initial Eligibility and Open Enrollment Period

The ideal time to enrol in a Medicare Supplement Insurance plan is during your initial eligibility period, which coincides with your Medicare Supplement Open Enrollment period. This period begins on the first day of the month in which you turn 65 and are enrolled in Medicare Part B. It lasts for six months. During this time, you have guaranteed issue rights, meaning insurance companies cannot use medical underwriting to deny your application based on pre-existing health conditions.

Special Circumstances and Guaranteed Issue Rights

If you missed your initial Open Enrollment period, there are still opportunities to apply for Medicare Supplement Insurance. Certain life events or changes in your circumstances may trigger a Guaranteed Issue period, during which you can enrol in a Medigap policy with guaranteed issue rights. These events include situations such as losing your current health coverage or your Medicare Advantage Plan no longer covering your area. Contact your State Insurance Department or consult the Medicare website to learn more about these special circumstances.

Annual Medicare Open Enrollment Period

It is important to distinguish between the Medicare Supplement Open Enrollment Period and the annual Medicare Open Enrollment Period. The latter occurs every year, during which you can change your Medicare Advantage Plan or prescription drug coverage. However, this period is not the ideal time to purchase a Medigap policy, as your options may be limited, and you may be subject to medical underwriting.

State-Specific Rules and Eligibility

It is worth noting that Medicare Supplement Insurance rules and eligibility criteria can vary by state. Some states allow individuals under 65 to purchase Medigap policies, especially if they are eligible for Medicare due to a disability or End-Stage Renal Disease (ESRD). Check with your State Insurance Department to understand your specific state's rules and your rights under state law.

Comparing Plans and Seeking Assistance

When considering Medicare Supplement Insurance, it is essential to compare plans available in your area. Evaluate the costs, coverage, and benefits offered by each plan. You can consult the "Medicare & You" handbook, speak to a trusted agent or broker, or contact your local State Health Insurance Assistance Program (SHIP) for free, personalised counselling. They can help you navigate the process and ensure you make an informed decision.

Accident Insurance: Pregnancy Coverage Explained

You may want to see also

Explore related products

![]()

Medicare Supplement Insurance providers

Medicare Supplement Insurance, also known as Medigap, is extra insurance you can buy from a private health insurance company to help cover the out-of-pocket costs that Original Medicare doesn't. Original Medicare includes Part A (Hospital Insurance) and Part B (Medical Insurance). While Medicare Part B generally covers about 80% of Part B expenses, you are responsible for paying the remaining 20%. A Medicare Supplement Insurance plan could help pay your share.

Medigap plans are offered by private insurance companies, with each plan having a different monthly premium. Some plans have higher monthly premiums but cover most of your out-of-pocket costs, while others have lower monthly premiums but cover fewer out-of-pocket costs.

When considering Medicare Supplement Insurance providers, it is important to compare multiple insurance companies and their quotes to find the best coverage and rate for your needs and budget. Here is a list of some Medicare Supplement Insurance providers:

- AARP Medicare Supplement Insurance from UnitedHealthcare: AARP offers a range of plans with different prices, wellness extras, and network restrictions. They have low complaint rates compared to their competitors and their plans are available in every state.

- Other providers: While a comprehensive list of all Medicare Supplement Insurance providers is beyond the scope of this response, other notable providers may include Mutual of Omaha, Cigna, and Blue Cross Blue Shield, among others. It is recommended to research these companies and compare their plans, prices, member satisfaction, and availability in your state.

Remember, the information provided here is for informational purposes only. It is always advisable to consult official government resources and speak with a licensed insurance agent or producer to understand your specific options and make an informed decision.

Medical and Dental Insurance: Government-Funded or Private?

You may want to see also

Frequently asked questions

Medicare Supplement Insurance, also known as Medigap, is private health insurance that adds on to Original Medicare (Part A and B). It helps pay for some costs that Original Medicare does not cover.

Medicare Supplement Insurance covers some costs not paid by Original Medicare Part A and B. Original Medicare will pay its share of the Medicare-approved amount for covered health costs, and then your Medicare Supplement Insurance plan will pay its share of the costs it covers.

You can apply for a Medicare Supplement insurance plan at any time during the year. The best time to enroll is during your Open Enrollment period, which is a six-month period that starts the first day of the month in which you are 65 or older and enrolled in Medicare Part B.